Global Heat Meter Market Size, Share and Forecast 2026 to 2035

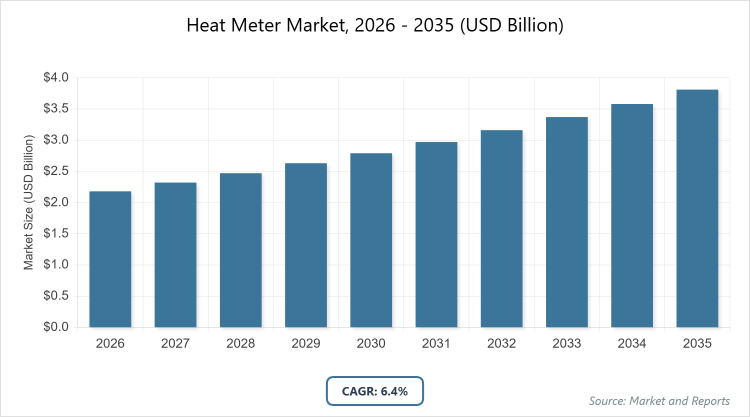

According to our latest research, the global heat meter market is projected to grow from USD 2.18 billion in 2026 to USD 3.8 billion by 2035, growing at a CAGR is estimated at 6.4% during 2026-2035. The Heat Meter Market is primarily driven by rising energy efficiency mandates and the expansion of district heating networks, which necessitate precise, consumption-based billing and real-time thermal monitoring to meet global decarbonization targets.

What are the Key Insights into the Heat Meter Market?

- Global market value projected to reach USD 3.8 billion by 2035 from USD 2.18 billion in 2026.

- Compound Annual Growth Rate (CAGR) estimated at 6.4% during 2026-2035.

- Static dominates the type segment.

- Wired Connection dominates the connectivity segment.

- Industrial dominates the end-user segment.

- North America dominates the regional market.

What is the Heat Meter Market?

Industry Overview

The heat meter market involves devices that measure thermal energy consumption in heating and cooling systems by calculating the flow rate of heat transfer fluid and temperature differences, ensuring accurate billing, energy efficiency, and compliance with regulations in residential, commercial, and industrial applications. These meters, including ultrasonic, electromagnetic, and mechanical types, are essential for district heating networks, individual buildings, and HVAC systems, providing data for optimizing energy use and reducing waste.

The market encompasses manufacturers, service providers, and end-users focused on smart metering integrations with IoT for real-time monitoring and predictive maintenance, driven by the global push for sustainable energy management amid climate change concerns. It bridges utility services with building management, emphasizing reliability, non-invasiveness, and cost-effectiveness while addressing challenges in installation and data accuracy in a landscape shaped by urbanization and renewable energy transitions.

What are the Market Dynamics in the Heat Meter Market?

Growth Drivers

The heat meter market is driven by mandatory regulatory requirements for energy monitoring in district heating systems, increasing adoption of smart metering technologies for accurate billing and efficiency, and growing infrastructure for renewable energy integration that necessitates precise heat measurement to optimize consumption and reduce carbon footprints in urban areas.

Restraints

Restraints include high initial costs for advanced ultrasonic meters and installation, limited awareness in developing regions, and competition from alternative heat sources like solar panels that reduce demand for traditional metering in some applications.

Opportunities

Opportunities lie in the expansion of district heating infrastructure in emerging economies, innovations in IoT-enabled wireless meters for remote monitoring, and partnerships for smart city projects that integrate heat meters with energy management systems to enhance sustainability.

Challenges

Challenges encompass regulatory inconsistencies across regions, complicating standardization, technical issues in wireless connectivity for accurate data transmission, and supply chain disruptions affecting component availability for meter production.

Heat Meter Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Heat Meter Market |

| Market Size 2025 | USD 2.18 Billion |

| Market Forecast 2035 | USD 3.8 Billion |

| Growth Rate | CAGR of 6.4% |

| Report Pages | 220 |

| Key Companies Covered | Danfoss, Kamstrup, Diehl Metering, Itron, Zenner International |

| Segments Covered | By Type, By Connectivity, By End-User, By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation Analysis for the Heat Meter Market?

The heat meter market is segmented by type, connectivity, end-user, and region.

By type segment, static emerges as the most dominant subsegment, followed by mechanical as the second most dominant. Static leads due to its non-invasive ultrasonic or electromagnetic technology that offers high accuracy and low maintenance for district heating applications, driven by regulatory demands for precise energy measurement; this dominance drives the market by enabling efficient data collection in large-scale systems, attracting investments in smart infrastructure, and facilitating integration with IoT for real-time analytics, thereby expanding adoption in industrial and residential sectors and boosting overall revenue through premium pricing and compliance advantages.

By connectivity segment, Wired Connection stands out as the most dominant subsegment in the connectivity segment, with Wireless Connection as the second most dominant. Wired Connection dominates owing to its reliability for accurate data transmission in clustered apartment heating systems, ensuring minimal interference and long battery life; this leadership propels the market by supporting high-density urban deployments, enabling stable integrations with building management systems, and driving demand for durable infrastructure that reduces operational costs, thus accelerating growth through widespread use in commercial and residential applications. Wireless Connection, gaining traction with IoT advancements, contributes through flexible remote monitoring in modern setups.

By end-user segment, Industrial is the most dominant subsegment in the end-user segment, followed by Residential as the second most dominant. Industrial dominates with the fastest CAGR, due to its need for precise heat measurement in equipment like boilers and chillers to regulate energy expenses and ensure operational efficiency; this position drives the market by generating high-value demand for advanced meters, fostering innovations in industrial IoT integrations, and enabling cost savings that attract large-scale investments, thereby expanding the overall market through efficiency gains and regulatory compliance. Residential, as the second dominant, supports growth via smart home energy monitoring trends.

What are the Recent Developments in the Heat Meter Market?

- In September 2025, Danfoss launched an AI-integrated ultrasonic heat meter for district heating, enhancing accuracy and enabling predictive maintenance to reduce energy waste in European markets.

- In November 2025, Kamstrup partnered with a major utility provider in North America to deploy wireless smart heat meters, focusing on real-time data analytics for residential billing efficiency.

What is the Regional Analysis of the Heat Meter Market?

- North America to dominate the market

North America holds a dominant position in the heat meter market, accounting for the sequential most significant stake, driven by new product availability, high energy monitoring demand, and a mature building industry; the United States leads as the dominating country through federal incentives for energy efficiency, widespread adoption in district heating, and innovations from players like Itron, addressing urban energy conservation amid climate goals.

Asia Pacific is projected to grow at the highest CAGR, led by rapid urbanization and building activities; China dominates here with cutting-edge metering devices and government support for district heating, enabling large-scale implementations in cities to combat energy waste.

Europe forecasts the fastest CAGR, owing to strong demand from emerging markets like Germany, Russia, and Turkey; Germany leads through its focus on renewable integration and environmental regulations, fostering advanced meter deployments in industrial heating systems.

Who are the Key Market Players and Their Strategies in the Heat Meter Market?

- Danfoss employs strategies focused on AI integrations and partnerships for smart metering, expanding in Europe through sustainable solutions for district heating.

- Kamstrup prioritizes wireless innovations, investing in IoT for remote monitoring to target residential and industrial segments.

- Diehl Metering leverages acquisitions for tech enhancements, focusing on ultrasonic accuracy for global compliance.

- Itron adopts data analytics strategies, forming alliances with utilities for energy management systems in North America.

- Zenner International concentrates on cost-effective mechanical meters, expanding in emerging markets through localized production.

What are the Market Trends in the Heat Meter Market?

- Adoption of IoT-based wireless connections for remote monitoring and control.

- Smart metering utilizing Automatic Meter Reading (AMR) radio-frequency modules.

- Increasing use in district heating and cooling systems.

- Growth in home automation systems integrating heat meters.

- Emphasis on energy conservation and accurate billing.

What Market Segments are Covered in the Heat Meter Market Report?

By Type

- Mechanical

- Static

By Connectivity

- Wired Connection

- Wireless Connection

By End-User

- Residential

- Commercial & Public

- Industrial

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Heat Meter Market - Industry Analysis

Chapter 4. Global Heat Meter Market- Competitive Landscape

Chapter 5. Global Heat Meter Market - Type Analysis

Chapter 6. Global Heat Meter Market - Connectivity Analysis

Chapter 7. Global Heat Meter Market - End-User Analysis

Chapter 8. Heat Meter Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Heat meters are devices that measure thermal energy by monitoring fluid flow rate and temperature differences in heating/cooling systems for accurate billing and efficiency.

Key factors include regulatory mandates for installation, energy conservation savings, district heating infrastructure growth, and technological advancements in smart metering.

The market is projected to grow from USD 2.18 billion in 2026 to USD 3.8 billion by 2035.

The CAGR is estimated at 6.4% during 2026-2035.

North America will contribute notably, holding the largest share due to energy monitoring demand and building industry maturity.

Major players include Danfoss, Kamstrup, Diehl Metering, Itron, Zenner International.

The report provides insights into market size, forecasts, segmentation, regional analysis, key players, trends, dynamics, and developments.

The value chain includes component manufacturing, assembly of flow sensors and calculators, integration with connectivity tech, distribution to end-users, and maintenance services.

Trends are evolving toward IoT and smart metering for remote control, with consumers preferring energy-efficient, accurate systems for cost savings.

Regulatory factors include mandates for installation and energy monitoring, while environmental factors involve climate concerns driving heat conservation and alternative sources.