Healthcare Fraud Analytics Market Size, Share and Trends 2026 to 2035

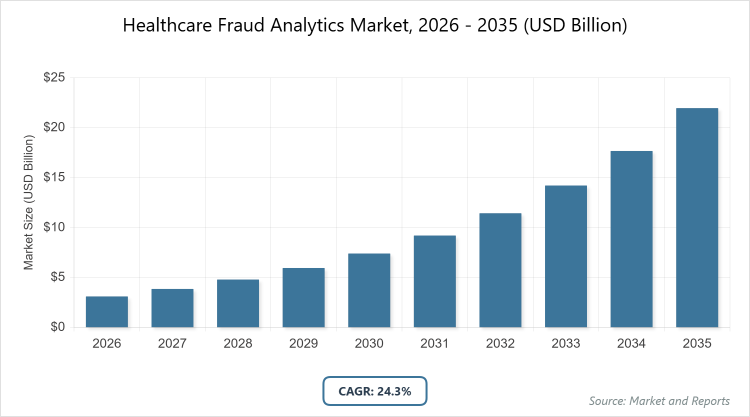

According to MarketnReports, the global Healthcare Fraud Analytics market size was estimated at USD 3.1 billion in 2025 and is expected to reach USD 22 billion by 2035, growing at a CAGR of 24.3% from 2026 to 2035. Healthcare Fraud Analytics Market is driven by rising healthcare expenditures, increasing fraud incidents, and advancements in AI and machine learning technologies.

What are the Key Insights into Healthcare Fraud Analytics?

- The global Healthcare Fraud Analytics market was valued at USD 3.1 billion in 2025 and is projected to reach USD 22 billion by 2035.

- The market is expected to grow at a CAGR of 24.3% during the forecast period from 2026 to 2035.

- The market is driven by escalating healthcare fraud cases, adoption of AI/ML for real-time detection, stringent regulatory requirements, and increasing digitalization of health records.

- In the type segment, predictive analytics dominates with a 40% share due to its proactive identification of potential fraud patterns using historical data and algorithms, enabling early intervention.

- In the application segment, insurance claims review dominates with a 45% share as it scrutinizes high-volume claims for discrepancies, crucial for payers to minimize losses.

- In the end-user segment, private insurance payers dominate with a 35% share owing to their exposure to large-scale fraud and need for cost recovery tools.

- North America dominates the regional market with a 40% share, driven by advanced healthcare infrastructure, high fraud incidence, and supportive regulations like HIPAA.

What is the Industry Overview of Healthcare Fraud Analytics?

The Healthcare Fraud Analytics market involves advanced data analysis tools and software designed to detect, prevent, and investigate fraudulent activities within healthcare systems, utilizing algorithms, machine learning, and big data to identify anomalies in claims, billing, and patient records. Market definition includes solutions that process vast amounts of healthcare data from insurers, providers, and regulators to flag suspicious patterns such as upcoding, duplicate billing, or phantom services, ensuring compliance, reducing financial losses, and improving operational integrity in an industry prone to complex fraud schemes due to its high-value transactions and regulatory complexities.

What are the Market Dynamics of Healthcare Fraud Analytics?

Growth Drivers

The Healthcare Fraud Analytics market is experiencing significant expansion due to the surging volume of healthcare data from electronic health records and claims processing, which necessitates sophisticated analytics to uncover hidden fraud patterns through machine learning and predictive modeling. Rising global healthcare expenditures, coupled with increasing incidents of billing fraud, phantom services, and identity theft, compel insurers and providers to adopt these solutions for financial safeguarding and operational efficiency. Advancements in AI and big data technologies enable real-time detection and automation, reducing manual reviews and false positives, while collaborations between tech firms and healthcare entities accelerate innovation. Stringent government regulations mandating fraud prevention further drive investments, particularly in integrated platforms that ensure compliance and enhance trust in healthcare systems.

Restraints

Implementation challenges, including high initial costs for AI-driven systems and integration with legacy healthcare IT infrastructure, restrict adoption among smaller providers and in resource-limited regions. Data privacy concerns under regulations like GDPR and HIPAA complicate analytics deployment, requiring robust security measures that increase complexity and expenses. Limited skilled personnel in data science and fraud analysis hinder effective utilization, while interoperability issues between disparate data sources lead to incomplete insights and higher error rates. Economic pressures on healthcare budgets, especially in developing economies, prioritize essential services over advanced analytics, slowing market penetration.

Opportunities

Opportunities abound in the expansion of AI and blockchain integrations for tamper-proof data tracking and enhanced predictive accuracy, appealing to emerging markets with growing digital health initiatives. Partnerships with telemedicine providers can address fraud in virtual care, while cloud-based solutions offer scalable, cost-effective options for SMEs. The rise of value-based care models emphasizes fraud prevention for accurate reimbursements, creating demand for specialized analytics. Government incentives for digital health in Asia and Latin America open untapped regions, and advancements in natural language processing for unstructured data analysis present innovative detection capabilities.

Challenges

Challenges include the evolving nature of fraud tactics, requiring continuous algorithm updates to combat sophisticated schemes like AI-generated false claims, straining R&D efforts. Data silos across healthcare stakeholders impede comprehensive analysis, while false positives from over-sensitive models lead to operational disruptions and trust issues. Regulatory variations across countries complicate global standardization, and cybersecurity threats to analytics platforms risk data breaches, eroding confidence. Talent shortages in specialized analytics exacerbate implementation delays, and ethical concerns over biased algorithms in fraud detection pose reputational risks.

Healthcare Fraud Analytics Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Healthcare Fraud Analytics Market |

| Market Size 2025 | USD 3.1 Billion |

| Market Forecast 2035 | USD 22 Billion |

| Growth Rate | CAGR of 24.3% |

| Report Pages | 220 |

| Key Companies Covered |

IBM, Optum, Inc., Cotiviti, Inc., SAS Institute, EXL Service Holdings, Inc., Wipro Limited, Conduent, Inc., DXC Technology, HCL Technologies Limited, OSP Labs, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Healthcare Fraud Analytics?

The Healthcare Fraud Analytics market is segmented by type, application, end-user, and region.

By Type. Predictive analytics is the most dominant subsegment, holding approximately 40% market share, due to its forward-looking approach in forecasting fraud risks based on patterns and trends, allowing preemptive actions. This dominance drives the market by minimizing losses through early detection and optimizing resource allocation for investigations. Descriptive analytics ranks as the second most dominant, with around 30% share, providing historical insights into fraud occurrences, propelling growth by enabling root cause analysis and informed strategy development.

By Application. Insurance claims review emerges as the most dominant subsegment, capturing about 45% share, primarily because it processes vast claim data to identify irregularities like upcoding or unbundling. This leads to market growth by safeguarding payer revenues and ensuring fair reimbursements. Payment integrity follows as the second most dominant, with a roughly 25% share, focusing on verifying transaction accuracy, driving the market via reduced overpayments and enhanced financial controls.

By End-User. Private insurance payers represent the most dominant subsegment at about 35% share, driven by their vulnerability to large-scale fraud and need for cost containment. This dominance accelerates market expansion through high-volume deployments and ROI-focused innovations. Public & government agencies rank second most dominant, holding around 25% share, due to regulatory mandates, contributing to growth by promoting transparency and public fund protection.

What are the Recent Developments in Healthcare Fraud Analytics?

- In December 2025, IBM Watson Health enhanced its fraud detection platform with new AI algorithms for real-time claims analysis, targeting upcoding in Medicare.

- In October 2025, Optum launched a blockchain-integrated module for its analytics suite, improving data integrity in multi-payer environments.

- In August 2025, SAS Institute partnered with a major insurer to deploy ML-based anomaly detection, reducing false positives by 30%.

- In June 2025, Cotiviti acquired a startup specializing in NLP for unstructured medical notes, bolstering fraud identification in clinical data.

- In April 2025, EXL Service introduced a cloud-based tool for predictive fraud scoring, aimed at small payers for affordable access.

What is the Regional Analysis of Healthcare Fraud Analytics?

- North America is expected to dominate the global market.

North America holds the largest share at approximately 40%, with the United States as the dominating country, attributed to its vast healthcare spending, high fraud prevalence, and advanced tech ecosystem supporting AI adoption. This leadership is underpinned by regulations like the False Claims Act, encouraging proactive analytics, and the presence of innovators like IBM and Optum driving R&D. Robust data infrastructure and collaborations between payers and tech firms enhance detection accuracy, while government initiatives like CMS fraud prevention programs amplify demand. The region’s mature insurance market, with complex Medicare and Medicaid systems, necessitates sophisticated tools for claims scrutiny. High-profile fraud cases prompt continuous investments in ML upgrades. Canada’s universal health system contributes through national anti-fraud strategies, fostering cross-border tech sharing.

Europe represents a strong market with steady growth, largely due to unified regulations like GDPR ensuring secure data handling, where Germany dominates through its efficient healthcare system and focus on digital health. The region’s expansion is fueled by EU funding for anti-fraud tech and increasing cross-border data sharing, supported by aging populations raising claim volumes and fraud risks. Collaborative efforts under the European Health Data Space promote standardized analytics across member states. The UK’s NHS invests in AI for payment integrity post-Brexit. Multilingual platforms cater to diverse markets like France and Italy. Emphasis on ethical AI addresses bias concerns in detection algorithms.

Asia Pacific is the fastest-growing region, exhibiting the highest CAGR, driven by expanding health insurance penetration and digitalization, with India leading due to government schemes like Ayushman Bharat necessitating fraud controls. This area’s potential lies in rising middle-class healthcare access, mobile tech adoption, and investments from global players addressing local fraud patterns. China’s social insurance reforms boost demand for real-time analytics in urban centers. Japan’s advanced tech infrastructure integrates AI for elderly care claims. Southeast Asian nations like Singapore adopt measures for telemedicine fraud prevention. Cultural shifts toward digital trust build user acceptance for analytics tools.

Latin America shows moderate but consistent growth, dominated by Brazil’s universal health system and rising private insurance, though limited by infrastructure challenges; expansion is supported by foreign investments in digital tools for public health fraud mitigation. Mexico benefits from NAFTA ties, enhancing cross-border data analytics with U.S. partners. Government programs in Argentina promote AI training for fraud investigators. The rise of telehealth in Colombia creates needs for virtual claim verification. However, economic volatility affects consistent funding. Emerging private payers drive demand for cost-effective cloud solutions.

The Middle East and Africa represent emerging markets with lower penetration but growing potential, particularly in the UAE through smart health initiatives and oil-funded systems, constrained by uneven tech access but advancing via partnerships for regulatory compliance. Saudi Arabia’s Vision 2030 invests in digital health platforms for fraud detection in expanding insurance. South Africa’s National Health Insurance pilots analytics for public fund protection. Technology transfers from European firms build local capabilities in Egypt. However, data scarcity in rural areas hinders comprehensive analysis. Investments in mobile-based tools address accessibility issues in the region.

What are the Key Market Players in Healthcare Fraud Analytics?

- IBM. IBM employs AI-driven Watson Health for predictive fraud detection, focusing on scalable cloud solutions and partnerships with insurers to enhance real-time analytics.

- Optum, Inc. Optum integrates ML with claims data for comprehensive fraud prevention, strategizing on acquisitions to expand its payment integrity offerings.

- Cotiviti, Inc. specializes in post-payment audits using advanced algorithms, pursuing data-driven insights to recover overpayments for payers.

- SAS Institute. SAS leverages statistical modeling for anomaly detection, investing in R&D for AI enhancements to address evolving fraud tactics.

- EXL Service Holdings, Inc. EXL focuses on end-to-end analytics services, employing domain expertise for customized solutions in claims review.

- Wipro Limited. Wipro offers holistic fraud management platforms, strategizing on global delivery models for cost-effective implementations.

- Conduent, Inc. targets government programs with compliance-focused tools, emphasizing automation for efficient investigations.

- DXC Technology. DXC integrates blockchain for secure data sharing, focusing on hybrid models for diverse healthcare environments.

What are the Market Trends in Healthcare Fraud Analytics?

- Increasing integration of AI and ML for predictive fraud detection.

- Adoption of blockchain for secure, tamper-proof data transactions.

- Rise of real-time analytics to prevent fraud at the point of claim.

- Growing use of NLP for analyzing unstructured clinical notes.

- Expansion of cloud-based solutions for scalability and accessibility.

- Focus on behavioral analytics to detect insider threats.

- Incorporation of big data from wearables for comprehensive monitoring.

What Market Segments and Subsegments are Covered in the Healthcare Fraud Analytics Report?

By Type

- Descriptive Analytics

- Predictive Analytics

- Prescriptive Analytics

- Real-Time Analytics

- Post-Payment Analytics

- Pre-Payment Analytics

- Rule-Based Analytics

- AI/ML-Based Analytics

- Anomaly Detection Analytics

- Behavioral Analytics

- Others

By Application

- Insurance Claims Review

- Pharmacy Billing Issue

- Payment Integrity

- Identity & Case Management

- Medical Coding Errors

- Duplicate Billing Detection

- Upcoding Detection

- Unbundling Detection

- Provider Fraud Detection

- Patient Fraud Detection

- Others

By End-User

- Public & Government Agencies

- Private Insurance Payers

- Third-Party Service Providers

- Employers

- Hospitals & Clinics

- Pharmaceutical Companies

- Healthcare Consultants

- Research Organizations

- Regulatory Bodies

- Managed Care Organizations

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Healthcare Fraud Analytics are data-driven tools using AI and algorithms to detect and prevent fraudulent activities in healthcare claims and operations.

Key factors include AI advancements, rising fraud cases, regulatory pressures, and digital health data growth.

The market is projected to grow from USD 3.1 billion in 2025 to USD 22 billion by 2035.

The CAGR is expected to be 24.3%.

North America will contribute notably, holding around 40% share due to high healthcare spending and regulations.

Major players include IBM, Optum, Cotiviti, SAS Institute, and EXL Service Holdings.

The report offers detailed insights on size, trends, segments, regions, players, and forecasts.

Stages include data collection, algorithm development, software integration, deployment, analysis, and reporting.

Trends evolve toward AI and real-time detection, with preferences for user-friendly, integrated platforms.

Regulations like HIPAA and GDPR mandate secure analytics, while environmental factors involve energy-efficient cloud computing.