Healthcare Augmented and Virtual Reality Market Size, Share and Trends 2026 to 2035

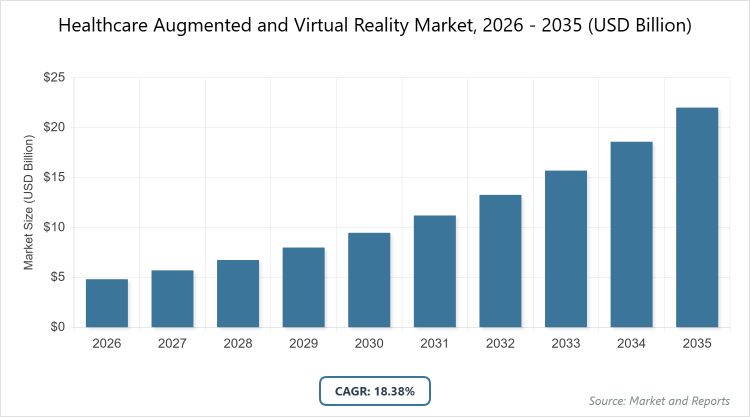

The global Healthcare Augmented and Virtual Reality Market size was estimated at USD 4.82 Billion in 2025 and is expected to reach USD 18.38 Billion by 2035, growing at a CAGR of 18.38% from 2026 to 2035. The Healthcare Augmented and Virtual Reality (AR/VR) market is primarily driven by the increasing demand for advanced medical training and simulation tools, alongside the rapid integration of immersive technologies to enhance surgical precision and patient rehabilitation.

What are the Key Insights?

- The global Healthcare Augmented and Virtual Reality Market was valued at approximately USD 4.82 billion in 2026, projected to reach USD 18.38 billion by 2035.

- The market is expected to grow at a CAGR of 18.38% during the forecast period from 2026 to 2035.

- In the component segment, hardware dominates with a share of around 67.8%.

- In the technology segment, augmented reality leads with a share of approximately 61%.

- In the application segment, medical training and education holds the largest share at about 30%.

- In the end-user segment, hospitals and surgical centers dominate with a share of over 40%.

- North America is the dominant region, accounting for 41% of the market share.

What is the Industry Overview?

Industry Definition

The Healthcare Augmented and Virtual Reality Market encompasses technologies that integrate digital information with the real world (augmented reality) or create fully immersive simulated environments (virtual reality) to enhance medical practices. Augmented reality overlays computer-generated images onto real-world views, aiding in tasks like surgical navigation and patient education, while virtual reality immerses users in artificial settings for applications such as training simulations and therapy. This market supports healthcare delivery by improving precision, reducing risks, and enabling remote interactions, transforming areas like diagnostics, rehabilitation, and professional development without relying on traditional physical constraints.

What are the Market Dynamics?

Growth Drivers

Advancements in hardware like head-mounted displays and sensors, coupled with increasing adoption for medical training and minimally invasive surgeries, are propelling the market forward. Rising healthcare expenditures, the need for efficient remote care amid aging populations, and supportive government initiatives for digital health integration further accelerate growth, as these technologies reduce costs, enhance patient outcomes, and address skill shortages in medical personnel.

Restraints

High initial costs for hardware and software implementation, along with limited reimbursement policies in many regions, hinder widespread adoption, particularly in resource-constrained settings. Concerns over data privacy, cybersecurity risks, and the lack of standardized regulations also slow progress, as healthcare providers grapple with integrating these technologies into existing workflows without compromising patient safety.

Opportunities

The integration of AI and 5G for real-time diagnostics and personalized treatments opens new avenues, especially in emerging markets with expanding digital infrastructure. Expanding applications in mental health therapy, chronic disease management, and telemedicine present untapped potential, as collaborations between tech firms and healthcare institutions drive innovation and scalability.

Challenges

Technical limitations such as device discomfort during prolonged use, latency issues in real-time applications, and the need for specialized training pose significant hurdles. Ethical concerns around patient consent in virtual environments, coupled with disparities in access across regions, challenge equitable deployment and long-term sustainability.

Healthcare Augmented and Virtual Reality Market : Report Scope

| Report Attributes | Report Details |

| Report Name | Healthcare Augmented and Virtual Reality Market |

| Market Size 2025 | USD 4.82 Billion |

| Market Forecast 2035 | USD 18.38 Billion |

| Growth Rate | CAGR of 18.38% |

| Report Pages | 215 |

| Key Companies Covered |

Microsoft, Google, Philips Healthcare, GE Healthcare, Siemens Healthineers, CAE Inc., Osso VR, Inc.,ImmersiveTouch, Inc.,VirtaMed AG,AccuVein, Inc. |

| Segments Covered | By Component, By Technology, By Application, By End User, By Region. |

| Regions Covered | Asia Pacific, North America, Europe, Latin America, The Middle East and Africa |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation?

Component Segmentation

The hardware segment is the most dominant in the component category, holding around 67.8% market share due to the essential role of devices like head-mounted displays, sensors, and smart glasses in enabling immersive experiences. It drives the market by providing the foundational infrastructure for AR and VR applications, reducing surgical errors and enhancing training efficiency through tangible, high-fidelity tools that integrate seamlessly with healthcare systems. The software segment is the second most dominant, capturing about 25% share, as it powers customizable simulations and data analytics, fostering innovation in patient-specific treatments and remote monitoring, which accelerates adoption by offering scalable, cost-effective solutions without heavy hardware reliance.

Technology Segmentation

Augmented reality dominates the technology segment with approximately 61% market share, excelling in real-time overlays for surgical guidance and diagnostics, which boosts precision and minimizes invasiveness, driving market growth through widespread integration in clinical settings. Virtual reality is the second most dominant, with around 39% share, thriving in immersive training and therapy environments that improve skill retention and patient rehabilitation, contributing to overall expansion by addressing gaps in hands-on education and mental health support.

Application Segmentation

Medical training and education is the most dominant application segment, comprising about 30% of the market, as it revolutionizes skill-building for healthcare professionals through risk-free simulations, enhancing competency and reducing real-world errors to propel industry-wide efficiency. Surgery is the second most dominant, holding around 25% share, by providing 3D visualizations and navigation aids that improve outcomes and shorten procedure times, fueling market advancement through better surgical precision and patient safety.

End-User Segmentation

Hospitals and surgical centers dominate the end-user segment with over 40% market share, leveraging AR and VR for complex procedures and patient management, which optimizes resource use and elevates care quality to drive broader market penetration. Academic institutes and research organizations are the second most dominant, with about 20% share, utilizing these technologies for innovative studies and training programs that accelerate knowledge transfer and foster long-term healthcare innovations.

What are the Recent Developments?

- In January 2024, Ocutrx Technologies launched the ORLenz headset, designed to replace traditional surgical loupes with higher resolution and magnification, improving ergonomics and efficiency in operating rooms.

- In June 2024, GE HealthCare and MediView XR completed the first clinical use of the OmnifyXR Interventional Suite in Minneapolis, combining AR with live imaging and 3D views to enhance radiology procedures and real-time collaboration.

- In March 2023, SimX partnered with the U.S. Air Force to develop VR training for Aeromedical Evacuation personnel, funded by USD 750,000 from the Small Business Innovation Research program, aiming to improve critical care transport skills.

- In November 2023, Smileyscope Therapy became the first VR device to receive FDA Class II clearance for acute pain management, focusing on pediatric procedures to reduce anxiety and improve patient experiences.

- In July 2025, DataArt partnered with German Lab E GmbH to launch a VR platform for psychotherapists, enabling immersive mental health treatments under expert supervision.

What is the Regional Analysis?

North America dominates the global market with a 41% share, driven by advanced healthcare infrastructure, high R&D investments, and supportive policies like NIH funding for AR/VR research. The United States leads as the dominating country, accounting for over 80% of the region’s market, due to widespread adoption in hospitals, collaborations between tech giants like Microsoft and medical institutions, and innovations in surgical training and telemedicine, which enhance efficiency and reduce costs amid rising chronic disease burdens.

Europe holds the second-largest share at around 30%, fueled by favorable regulations, increasing digital health initiatives, and partnerships for AR/VR integration in medical education and therapy. Germany is the dominating country, contributing about 25% to the region’s market, with strong emphasis on precision medicine, collaborations like Vuzix and VSee for telemedicine, and government-backed R&D in immersive technologies that improve surgical outcomes and address workforce shortages in aging populations.

Asia Pacific is the fastest-growing region with a projected CAGR of over 25%, supported by expanding healthcare access, rising investments in digital infrastructure, and government programs promoting tech adoption. China dominates the region with around 35% share, driven by rapid urbanization, increasing AR/VR use in training and rehabilitation, and initiatives like national health tech funds that tackle physician shortages and enhance remote care in vast rural areas.

Latin America accounts for about 10% of the market, growing through improving digital connectivity and targeted investments in affordable AR/VR solutions for training and patient care. Brazil is the dominating country, holding over 50% of the region’s share, with efforts to integrate these technologies in public health systems, partnerships for surgical simulations, and focus on reducing healthcare disparities in underserved communities.

The Middle East and Africa represent around 8% of the market, with growth spurred by oil-funded healthcare modernization and international collaborations for tech transfer. Saudi Arabia dominates with about 40% regional share, leveraging Vision 2030 initiatives to adopt AR/VR in medical education and therapy, addressing skill gaps and enhancing specialized care in high-investment hubs like Riyadh.

Who are the Key Market Players and Their Strategies?

Microsoft focuses on expanding its HoloLens ecosystem through partnerships with hospitals for mixed-reality surgical planning and training, emphasizing AI integration to enhance real-time data visualization and remote collaboration.

Google invests in AR/VR for healthcare via cloud-based platforms and acquisitions, prioritizing scalable solutions for diagnostics and education to drive accessibility and innovation in emerging markets.

Philips Healthcare pursues strategies centered on hardware-software integration, collaborating with startups for immersive therapy tools and leveraging its imaging expertise to improve surgical navigation and patient outcomes.

GE Healthcare emphasizes R&D in AR overlays for radiology, forming alliances like with MediView for interventional suites to boost procedural efficiency and expand its presence in North American hospitals.

Siemens Healthineers adopts a strategy of embedding AR/VR in its diagnostic equipment, focusing on global expansions and regulatory approvals to enhance training simulations and precision medicine applications.

CAE Inc. concentrates on simulation-based training solutions, partnering with academic institutions to develop customizable VR modules that address skill shortages and improve healthcare workforce readiness.

Osso VR, Inc. specializes in orthopedic training platforms, securing investments for platform expansions and clinical validations to dominate surgical education and reduce procedural risks.

ImmersiveTouch, Inc. targets neurosurgery with haptic-enabled VR, pursuing FDA clearances and hospital integrations to pioneer personalized surgical rehearsals and drive market adoption.

VirtaMed AG focuses on laparoscopic and endoscopic simulations, collaborating with medical societies for standardized training programs that enhance global surgical proficiency.

AccuVein, Inc. innovates in vein visualization AR, expanding through direct sales and partnerships to improve procedural success rates in hospitals and clinics worldwide.

What are the Market Trends?

- Integration of AI with AR/VR for personalized diagnostics and predictive analytics in treatments.

- Rising adoption in mental health therapy, using immersive environments for anxiety and PTSD management.

- Expansion of telemedicine applications, enabling remote consultations and virtual patient monitoring.

- Growth in wearable AR devices for real-time surgical guidance and rehabilitation tracking.

- Increased focus on data security and ethical standards to address privacy concerns in virtual healthcare.

- Surge in collaborative platforms for multi-user training sessions across global healthcare teams.

- Emphasis on cost-effective, mobile-based VR solutions for resource-limited settings.

What Market Segments are Covered in the Report?

- By Component

- Hardware

- Software

- Services

- By Technology

- Augmented Reality

- Virtual Reality

- By Application

- Surgery

- Therapy

- Education and Training

- Rehabilitation

- Medical Training and Education

- Diagnostic Imaging

- Patient Care and Management

- By End User

- Hospitals, Clinics, and Surgical Centers

- Academic Institutes and Research Organizations

- Diagnostics Centers

- Rehabilitation Centers

- Pharmaceutical and Biotech Companies

- Medical Device Manufacturers

- Patients/Home Users

- Government and Defense

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

The Healthcare Augmented and Virtual Reality Market refers to technologies that overlay digital elements onto real-world views (AR) or create simulated environments (VR) to improve medical training, surgery, therapy, and patient care, enhancing precision and efficiency in healthcare delivery.

Key factors include technological advancements in hardware and AI integration, rising demand for remote training and telemedicine, increasing healthcare expenditures, supportive government policies, and the need to address skill shortages and reduce procedural risks.

The market is projected to grow from approximately USD 4.82 billion in 2026 to USD 18.38 billion by 2035.

The market is expected to grow at a CAGR of 18.38% from 2026 to 2035.

North America will contribute notably, holding around 41% of the market value, driven by advanced infrastructure and high adoption rates.

Major players include Microsoft, Google, Philips Healthcare, GE Healthcare, Siemens Healthineers, CAE Inc., Osso VR, Inc., ImmersiveTouch, Inc., VirtaMed AG, and AccuVein, Inc.

The report provides comprehensive insights into market size, growth forecasts, segmentation, dynamics, regional analysis, key players, trends, and recent developments, offering a detailed overview for strategic decision-making.

The value chain includes research and development of hardware/software, manufacturing and integration, distribution through partnerships, deployment in healthcare settings, and ongoing services like training and maintenance.

Trends are shifting toward AI-enhanced personalization and mobile accessibility, while consumers prefer immersive, user-friendly tools for therapy and education that prioritize privacy and seamless integration with existing healthcare systems.

Regulatory factors include FDA clearances for devices and data privacy laws like HIPAA, while environmental considerations involve sustainable hardware production and energy-efficient designs to minimize electronic waste in healthcare tech.