Headless Compression Screws Market Size, Share and Trends 2026 to 2035

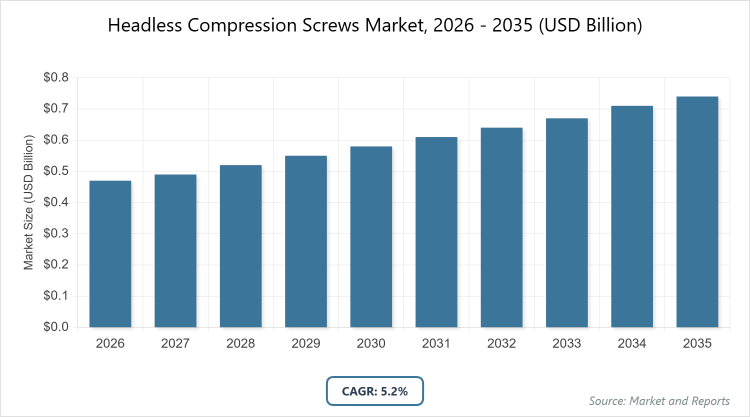

According to MarketnReports, the global Headless Compression Screws market size was estimated at USD 0.47 billion in 2025 and is expected to reach USD 0.78 billion by 2035, growing at a CAGR of 5.2% from 2026 to 2035. Headless Compression Screws Market is driven by the increasing prevalence of orthopedic injuries and rising demand for minimally invasive surgeries.

What are the Key Insights of Headless Compression Screws Market?

- The global Headless Compression Screws market size was valued at USD 0.47 billion in 2025 and is projected to reach USD 0.78 billion by 2035.

- The market is expected to grow at a CAGR of 5.2% during the forecast period 2026-2035.

- The market is driven by rising orthopedic injuries, aging population, and advancements in minimally invasive surgical techniques.

- In the product type segment, Fully Threaded Screw dominated with 61% share due to its effectiveness in stabilizing bone fragments without requiring additional compression, making it ideal for non-compressive fixation procedures.

- In the application segment, Hand dominated with 35% share due to the high incidence of hand fractures from trauma and sports, where these screws provide discreet fixation and reduce soft tissue irritation.

- In the end-user segment, Hospitals dominated with 50% share due to their capacity for handling complex orthopedic surgeries and access to advanced surgical infrastructure.

- North America dominated with 38% share due to its advanced healthcare systems, high surgical volumes, and strong presence of key manufacturers.

What is the Headless Compression Screws Market Industry Overview?

The Headless Compression Screws market encompasses specialized orthopedic implants designed for internal fixation of bone fractures, particularly in small bones and joints, where minimal tissue irritation and optimal compression are essential. These screws feature a design without a protruding head, allowing them to be fully embedded within the bone, which promotes stable fixation and accelerates healing by applying interfragmentary compression. The market includes devices used in trauma, sports medicine, and reconstructive surgeries, serving healthcare providers focused on enhancing patient outcomes through advanced biomaterials and precise surgical tools. This sector is integral to the broader orthopedic devices industry, addressing needs in fracture management and joint fusion procedures.

What are the Headless Compression Screws Market Dynamics?

Growth Drivers

The primary growth drivers for the Headless Compression Screws market include the escalating incidence of orthopedic injuries and fractures stemming from sports activities, road accidents, and an aging global population prone to bone degeneration. Advancements in minimally invasive surgical techniques have further propelled demand, as these screws enable precise fixation with reduced tissue disruption and faster recovery times. Additionally, innovations in biocompatible materials like titanium and bioresorbable compounds enhance implant performance, encouraging adoption among surgeons for improved patient outcomes in trauma and reconstructive procedures.

Restraints

High costs associated with advanced headless compression screws and specialized surgical tools pose significant restraints, particularly in cost-sensitive regions and emerging markets where healthcare budgets are limited. Stringent regulatory approval processes for new implants delay product launches and increase development expenses, hindering market entry for smaller players. Moreover, the need for skilled orthopedic surgeons trained in these specific fixation methods can limit widespread adoption in under-resourced healthcare settings.

Opportunities

Emerging opportunities in the Headless Compression Screws market lie in the development and commercialization of bioresorbable screws, which eliminate the need for secondary removal surgeries and align with patient preferences for less invasive long-term solutions. Expanding healthcare infrastructure in Asia-Pacific and Latin America regions presents untapped potential, driven by rising disposable incomes and increasing awareness of advanced orthopedic treatments. Strategic partnerships between manufacturers and healthcare providers could accelerate innovation in customizable implants tailored to specific anatomical needs.

Challenges

Key challenges include intense competition from alternative fixation devices like plates and pins, which may offer similar outcomes at lower costs in certain applications. Ensuring consistent product quality and biocompatibility amid varying global manufacturing standards remains a hurdle, potentially leading to recalls or safety concerns. Additionally, the market faces obstacles from fluctuating raw material prices for metals like titanium, impacting production costs and profitability for manufacturers.

Headless Compression Screws Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Headless Compression Screws Market |

| Market Size 2025 | USD 0.47 Billion |

| Market Forecast 2035 | USD 0.78 Billion |

| Growth Rate | CAGR of 5.2% |

| Report Pages | 240 |

| Key Companies Covered |

Stryker, DePuy Synthes (Johnson & Johnson), Zimmer Biomet, Smith & Nephew, Arthrex, Acumed, Medartis, and Others |

| Segments Covered | By Product Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Headless Compression Screws Market Segmentation?

The Headless Compression Screws market is segmented by product type, application, end-user, and region.

Based on Product Type Segment. The Fully Threaded Screw is the most dominant subsegment, holding a significant market share due to its versatility in providing stable fixation for bone fragments in non-compressive scenarios, while the Both Ends Threaded Screw is the second most dominant, favored for applications requiring targeted compression between bone segments. The dominance of Fully Threaded Screw stems from its broad applicability in small bone fractures, driving market growth by enabling efficient surgical outcomes and reducing operative time, whereas Both Ends Threaded Screw contributes by addressing specific needs in joint fusions, enhancing overall market expansion through specialized trauma solutions.

Based on Application Segment. The Hand application is the most dominant subsegment, capturing a substantial portion due to the high frequency of hand-related injuries and the screws’ ability to offer discreet, low-profile fixation, while Foot is the second most dominant, driven by common ankle and foot fractures in sports and elderly populations. Hand’s dominance arises from its critical role in restoring fine motor functions with minimal scarring, propelling market growth via increased demand in outpatient procedures, and Foot supports this by facilitating weight-bearing recovery, collectively boosting the market through improved patient mobility and surgical precision.

Based on End-User Segment. Hospitals represent the most dominant subsegment, accounting for the largest share owing to their equipped facilities for complex orthopedic interventions, while Ambulatory Surgical Centers are the second most dominant, gaining traction for cost-effective, same-day surgeries. Hospitals’ leading position is attributed to handling high-volume trauma cases and access to multidisciplinary teams, fueling market growth by integrating advanced implant technologies, whereas Ambulatory Surgical Centers drive expansion through efficient, minimally invasive operations that reduce hospital stays and healthcare costs.

What are the Recent Developments in Headless Compression Screws Market?

- In October 2025, Johnson & Johnson announced its intent to separate its orthopedics division, DePuy Synthes, as a standalone business, aiming to focus on innovation in fixation devices including headless compression screws to better address market demands.

- In October 2025, Zimmer Biomet completed the acquisition of Monogram Technologies, enhancing its portfolio in robotics and joint reconstruction, which indirectly supports advancements in screw technologies for musculoskeletal applications.

- In August 2023, Acumed launched the Acutrak 3 headless compression screw system, featuring an innovative thread pitch design to improve surgical performance and versatility in fracture fixation.

What is the Headless Compression Screws Market Regional Analysis?

North America to dominate the global market.

North America holds the leading position in the Headless Compression Screws market, driven by robust healthcare infrastructure, high adoption of advanced surgical technologies, and a large geriatric population susceptible to orthopedic conditions. The United States dominates within the region, benefiting from extensive research and development investments, favorable reimbursement policies, and a high volume of trauma-related surgeries, which collectively sustain demand for innovative fixation solutions.

Europe maintains a strong market presence, supported by well-established medical facilities and increasing orthopedic procedures amid an aging demographic. Germany stands out as the dominating country, owing to its advanced manufacturing capabilities, stringent quality standards, and emphasis on minimally invasive techniques that enhance the adoption of these screws in clinical settings.

Asia-Pacific is experiencing the fastest growth, fueled by expanding healthcare access, rising disposable incomes, and growing awareness of orthopedic treatments. China emerges as the dominating country in the region, propelled by rapid infrastructure development, increasing sports injuries, and government initiatives to improve surgical outcomes through imported and locally produced implants.

Latin America shows moderate growth potential, with improving healthcare systems and rising medical tourism contributing to market expansion. Brazil dominates the region, driven by a surge in orthopedic surgeries and investments in hospital modernization to address trauma and degenerative bone issues.

The Middle East and Africa region is gradually evolving, constrained by varying healthcare access but boosted by international collaborations. South Africa leads as the dominating country, supported by relatively advanced medical centers and efforts to tackle injury-related demands through imported orthopedic devices.

Who are the Key Headless Compression Screws Market Players and Strategies?

- Stryker focuses on continuous innovation through research and development, launching advanced screw systems like the PowerDrill 3 to enhance surgical efficiency, while expanding its global footprint via strategic acquisitions to strengthen its position in orthopedic fixation.

- DePuy Synthes (Johnson & Johnson) emphasizes product diversification and clinical collaborations, introducing bioabsorbable options to meet evolving surgeon needs, coupled with investments in digital surgical tools to improve precision and patient outcomes in trauma applications.

- Zimmer Biomet pursues growth through mergers and acquisitions, such as the Monogram Technologies deal, integrating robotics with screw technologies, and prioritizing customizable implants to address specific anatomical requirements in joint and fracture management.

- Smith & Nephew adopts a strategy of technological advancements in materials and design, partnering with healthcare providers for training programs, aiming to increase adoption in minimally invasive procedures and expand market share in emerging regions.

- Arthrex concentrates on specialized product launches, like screws with PEEK washers, and invests in surgeon education to promote its versatile fixation solutions, fostering loyalty and driving penetration in sports medicine and arthroscopic surgeries.

- Acumed leverages innovation in thread designs, as seen in the Acutrak 3 system, while focusing on quality manufacturing and global distribution networks to cater to diverse clinical needs in small bone fixation.

- Medartis prioritizes precision engineering and modular systems, engaging in strategic partnerships for market expansion, particularly in Europe and Asia, to offer reliable solutions for complex fractures and enhance surgical predictability.

What are the Headless Compression Screws Market Trends?

- Increasing adoption of bioresorbable materials like polylactic acid to reduce the need for secondary surgeries and improve long-term patient comfort.

- Rising preference for minimally invasive techniques, enabling faster recovery and lower complication rates in orthopedic procedures.

- Advancements in screw designs, such as variable thread pitches, to optimize compression and stability in small bone fractures.

- Growing integration of digital tools and robotics for precise implant placement, enhancing surgical accuracy and outcomes.

- Expansion in emerging markets driven by healthcare infrastructure improvements and rising awareness of advanced fixation options.

What are the Headless Compression Screws Market Segments and their Subsegment Covered in the Report?

-

By Product Type

- Fully Threaded Screw

- Both Ends Threaded Screw

- Others

-

By Application

- Hand

- Wrist

- Foot

- Ankle

- Others

-

By End-User

- Hospitals

- Ambulatory Surgical Centers

- Clinics

- Others

- By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Headless Compression Screws are orthopedic implants designed for internal bone fixation, featuring a headless structure that allows full embedding in bone to provide compression and stability without protruding hardware.

Key factors include rising orthopedic injuries, aging population, advancements in minimally invasive surgeries, and innovations in biocompatible materials.

The market is projected to grow from USD 0.47 billion in 2025 to USD 0.78 billion by 2035.

The CAGR is expected to be 5.2% during the forecast period.

North America will contribute notably, driven by advanced healthcare infrastructure and high surgical volumes.

Major players include Stryker, DePuy Synthes (Johnson & Johnson), Zimmer Biomet, Smith & Nephew, Arthrex, Acumed, and Medartis.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, and forecasts.

The value chain includes raw material sourcing, manufacturing, distribution, surgical application, and post-operative care.

Trends are shifting toward bioresorbable and customizable screws, with consumers preferring minimally invasive options for faster recovery.

Stringent regulatory approvals for implants and emphasis on sustainable, biocompatible materials are key factors influencing growth.