Gas Turbines Market Size, Share and Trends 2026 to 2035

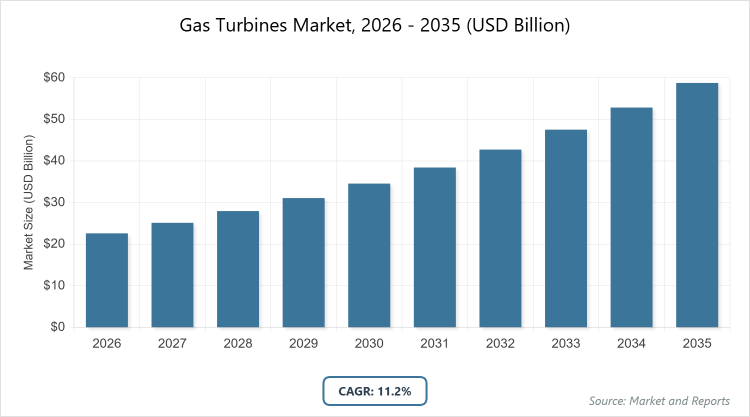

According to MarketnReports, the global gas turbines market size was estimated at USD 22.6 billion in 2025 and is expected to reach USD 64.8 billion by 2035, growing at a CAGR of 11.2% from 2026 to 2035. Gas Turbines Market is driven by the increasing global demand for electricity and the shift from coal to cleaner natural gas as a “bridge fuel,” coupled with the critical need for flexible, dispatchable power generation to balance the intermittency of growing renewable energy sources.

What are the Key Insights into the Gas Turbines Market?

- Global gas turbines market valued at approximately USD 22.6 billion in 2025, projected to reach USD 64.8 billion by 2035.

- Expected CAGR of around 11.2% from 2026 to 2035, driven by cleaner energy transitions and technological advancements.

- Dominant subsegment by type: Combined cycle turbines, accounting for the largest share due to high efficiency in power generation.

- Dominant subsegment by capacity: >300 MW, holding over 50% market share for utility-scale applications.

- Dominant subsegment by application: Power generation, contributing around 70% revenue for electricity production.

- Dominant region: North America, contributing over 35% of global revenue with the United States as the leading country.

What is the Gas Turbines Industry Overview?

Industry Overview

Gas turbines are rotating engines that convert fuel energy into mechanical power through combustion, compression, and expansion processes, widely used for power generation, propulsion in aircraft, and industrial applications where they provide high efficiency, low emissions, and flexibility in fuel types like natural gas, hydrogen, or biofuels. These turbines consist of components such as compressors, combustors, turbines, and generators, operating on the Brayton cycle to produce electricity or thrust, serving sectors like energy, aerospace, and oil & gas where they enable reliable, scalable operations with quick start-up capabilities for peak load management.

Gas turbines are categorized by design, capacity, and technology, emphasizing advancements in aerodynamics and materials for higher temperatures and efficiencies to meet environmental standards.The industry involves raw material suppliers for alloys and ceramics, manufacturers employing precision engineering and testing for durability, and service providers offering maintenance and upgrades, prioritizing innovation to reduce carbon footprints through hydrogen blending and carbon capture. This market is driven by the global energy transition, infrastructure demands, and aerospace growth, balancing traditional fossil fuel uses with renewable integrations in a competitive landscape focused on sustainability and digitalization.

What are the Market Dynamics in the Gas Turbines Sector?

Growth Drivers

The gas turbines market is propelled by the global shift toward cleaner energy sources, with natural gas-fired turbines offering lower emissions than coal, driven by government policies promoting decarbonization and investments in combined cycle plants that achieve over 60% efficiency for power generation amid rising electricity demands from urbanization and electrification. Increasing adoption in aerospace for fuel-efficient jet engines supports growth, while industrial applications in oil & gas for compression and pumping benefit from energy security needs.

Technological advancements in hydrogen-ready turbines and digital twins for predictive maintenance attract investments, and the expansion of renewable integration with gas turbines for grid stability further accelerates demand in hybrid systems.

Restraints

High capital costs for advanced gas turbines, often exceeding USD 1 million per MW, limit deployment in budget-constrained regions where coal remains cheaper, exacerbated by long lead times for manufacturing and installation. Volatility in natural gas prices affects operational economics, while environmental concerns over NOx and CO2 emissions require costly after-treatment systems like SCR. Supply chain disruptions for critical materials like nickel alloys cause delays, and competition from renewables like solar and wind in base-load power reduces market share in mature grids. Regulatory uncertainties in carbon pricing hinder long-term planning.

Opportunities

Opportunities lie in the development of hydrogen-blended and 100% hydrogen turbines for net-zero goals, supported by R&D funding from governments aiming for 2050 carbon neutrality, enabling retrofits in existing plants. Expansion into emerging markets with growing energy needs offers growth through modular, small-scale turbines for distributed power, while partnerships for carbon capture integration unlock incentives in Europe and North America. Innovations in additive manufacturing for faster component production reduce costs, and the aerospace sector’s demand for efficient turbofans in sustainable aviation fuels presents niches. Digital services for remote monitoring enable new revenue streams via subscriptions.

Challenges

Achieving high efficiency with alternative fuels like hydrogen poses technical challenges, requiring material upgrades to handle higher temperatures amid R&D constraints. Navigating diverse regulatory environments for emissions and fuel standards increases compliance costs, while geopolitical risks disrupt gas supply chains. Talent shortages for specialized engineering demand training, and integrating turbines with intermittent renewables requires advanced controls. Balancing affordability with performance in competitive bids remains a hurdle amid economic volatility affecting energy investments.

Gas Turbines Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Gas Turbines Market |

| Market Size 2025 | USD 22.6 billion |

| Market Forecast 2035 | USD 64.8 billion |

| Growth Rate | CAGR of 11.2% |

| Report Pages | 235 |

| Key Companies Covered | GE Vernova, Siemens Energy, Mitsubishi Heavy Industries, Ansaldo Energia, Solar Turbines (Caterpillar), Kawasaki Heavy Industries, and Bharat Heavy Electricals Limited. |

| Segments Covered | By Type, Capacity, Application, and Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Gas Turbines Market Segmented?

The Gas Turbines market is segmented by type, capacity, application, and region.

By Type, The combined cycle turbines segment dominates the gas turbines market, primarily because of their superior thermal efficiency exceeding 60% by recovering waste heat for steam generation, making them ideal for base-load power plants where cost-effective, low-emission electricity is essential, supported by global decarbonization efforts. This dominance drives the market by enabling compliance with emission regulations, attracting investments in natural gas infrastructure, and optimizing fuel use in utility-scale projects, thereby expanding adoption in energy transitions through higher output and reduced operational costs.

The open cycle turbines segment ranks second, valued for their quick start-up and flexibility in peaking applications where rapid response to demand fluctuations is critical, helping to propel market growth by supporting grid stability with renewables, enhancing reliability in industrial settings, and offering simpler, lower-cost options in emerging markets.

By Capacity, 300 MW leads the capacity segment, as these large-scale turbines provide economical power for utility grids and industrial complexes where high output and efficiency are paramount, driven by energy demand in populated regions. This subsegment drives the market by aligning with infrastructure projects, promoting combined cycle deployments for base-load, and complying with scale economies, thus increasing demand globally. 50-300 MW follows as the second dominant, suitable for mid-sized plants and distributed generation where flexibility and modularity are key, contributing to market expansion through industrial applications, enhancing energy security, and tapping into remote power needs.

By Application, Power generation dominates the application segment, fueled by gas turbines’ role in efficient, low-emission electricity production for grids, supported by natural gas abundance and renewable integrations. This leadership accelerates market growth by syncing with energy transitions, fostering investments in CCGT plants, and ensuring regulatory compliance, boosting adoption worldwide. Aerospace & marine ranks second, utilized for propulsion in jets and ships where compact, high-power turbines are essential, helping to drive the market through aviation growth, enhancing fuel efficiency, and supporting defense applications.

What are the Recent Developments in the Gas Turbines Market?

In 2025, GE Vernova launched a new H-class turbine with hydrogen capability, achieving 65% efficiency in combined cycle mode, targeting decarbonization in Europe and boosting orders from utility firms for net-zero transitions.

In late 2025, Siemens Energy acquired a startup specializing in digital twins for turbine optimization, integrating AI for predictive maintenance to reduce downtime by 20%, strengthening its service portfolio in North America.

In 2026, Mitsubishi Heavy Industries partnered with a Chinese firm for localized production of aero-derivative turbines, focusing on industrial applications to meet growing energy demands in Asia-Pacific.

In early 2026, Ansaldo Energia introduced a flexible open cycle turbine for peaking plants, compliant with Euro 7 emissions, gaining traction in renewable-heavy grids across Europe.

What is the Regional Analysis of the Gas Turbines Market?

- Asia-Pacific to dominate the market

Asia-Pacific is the fastest-growing region in the gas turbines market, driven by rapid industrialization, energy demand from urbanization, and shifts to natural gas for cleaner power, with China as the dominating country due to its massive installed capacity exceeding 100 GW, government policies like the 14th Five-Year Plan promoting gas-fired plants, and leadership in manufacturing through companies like Harbin Electric that supply domestically and export regionally.

The region’s growth is supported by India’s renewable integrations and Southeast Asia’s LNG imports; Japan’s hydrogen pilots contribute, but China’s dominance stems from its vast infrastructure investments, low-cost production, and policy-driven transitions from coal, boosting revenue through high-volume power generation and industrial applications amid population growth.

North America dominates the gas turbines market, characterized by abundant natural gas resources and regulatory focus on low-emission power, with the United States as the dominating country owing to its shale gas boom, FERC incentives for grid reliability, and major players like GE Vernova driving innovations in combined cycle plants for over 1,000 GW capacity. The region benefits from Canada’s hydropower synergies; the U.S. leads with investments in hydrogen-ready turbines, enhancing market expansion via premium aerospace and marine uses.

Europe exhibits steady growth in the gas turbines market, focused on energy security and decarbonization, with Germany as the dominating country due to its Energiewende policy, EU Green Deal, and firms like Siemens Energy advancing hydrogen turbines for sustainable grids. The region is propelled by the UK’s offshore wind backups and France’s nuclear complements; Germany’s leadership arises from exports and green tech, fostering market development by addressing renewable intermittency.

The Rest of the World shows emerging potential in the gas turbines market, with Saudi Arabia dominating in the Middle East through Vision 2030 diversification from oil with gas plants, while Brazil leads in Latin America with biofuel blends. Growth is driven by Africa’s LNG developments in Nigeria; the region’s progress relies on foreign investments, increasing share in power generation.

Who are the Key Market Players and Strategies in the Gas Turbines Industry?

GE Vernova: Focuses on hydrogen-capable turbines, expanding through R&D for efficiency and acquisitions for digital services to lead in decarbonization.

Siemens Energy: Emphasizes modular designs, investing in Europe expansions and partnerships for renewable integrations.

Mitsubishi Heavy Industries: Prioritizes aero-derivative tech, pursuing Asia-Pacific localizations for industrial applications.

Ansaldo Energia: Concentrates on flexible open cycle systems, leveraging European compliance for peaking plants.

Solar Turbines (Caterpillar): Adopts oil & gas-focused strategies, focusing on durability for remote operations.

Kawasaki Heavy Industries: Utilizes marine propulsion advancements, investing in hydrogen pilots.

Bharat Heavy Electricals Limited: Employs cost-effective manufacturing, targeting India expansions for utility-scale projects.

What are the Current Market Trends in the Gas Turbines Sector?

- Shift toward hydrogen-ready and low-emission turbines for net-zero goals.

- Growth in combined cycle plants for higher efficiency in power generation.

- Integration with renewables for hybrid grid stability.

- Advancements in digital twins and AI for predictive maintenance.

- Expansion in aero-derivative turbines for flexible peaking.

- Focus on modular designs for faster deployment in emerging markets.

What Market Segments are Covered in the Report?

By Type

-

- Combined Cycle Turbines

- Open Cycle Turbines

By Capacity

-

- <50 MW

- 50-300 MW

- 300 MW

By Application

-

- Power Generation

- Aerospace & Marine

- Oil & Gas

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Gas Turbines Market - Industry Analysis

Chapter 4. Global Gas Turbines Market- Competitive Landscape

Chapter 5. Global Gas Turbines Market - Type Analysis

Chapter 6. Global Gas Turbines Market - Capacity Analysis

Chapter 7. Global Gas Turbines Market - Application Analysis

Chapter 8. Gas Turbines Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Gas turbines are engines that convert fuel into mechanical energy through combustion, used for power generation, propulsion, and industrial processes with high efficiency and flexibility.

Key factors include emission regulations, hydrogen adoption, renewable integrations, and industrial expansions.

The gas turbines market is projected to grow from approximately USD 25.4 billion in 2026 to USD 64.8 billion by 2035.

The CAGR for the gas turbines market during 2026-2035 is expected to be around 11.2%, driven by energy transitions.

North America will contribute notably, accounting for over 35% of the market value, led by natural gas in the United States.

Major players include GE Vernova, Siemens Energy, Mitsubishi Heavy Industries, Ansaldo Energia, Solar Turbines (Caterpillar), Kawasaki Heavy Industries, and Bharat Heavy Electricals Limited.

The global gas turbines market report provides insights into size, segmentation, dynamics, regional analysis, players, trends, and forecasts.

The value chain includes component sourcing, turbine manufacturing, assembly, installation, and maintenance services.

Market trends are evolving toward hydrogen and modular designs, with preferences shifting to efficient, low-emission solutions for power and aerospace.

Regulatory factors include emission standards like Euro 7, while environmental factors involve decarbonization mandates, driving hydrogen innovations but increasing costs.