Gas Engine Market Size, Share and Trends 2026 to 2035

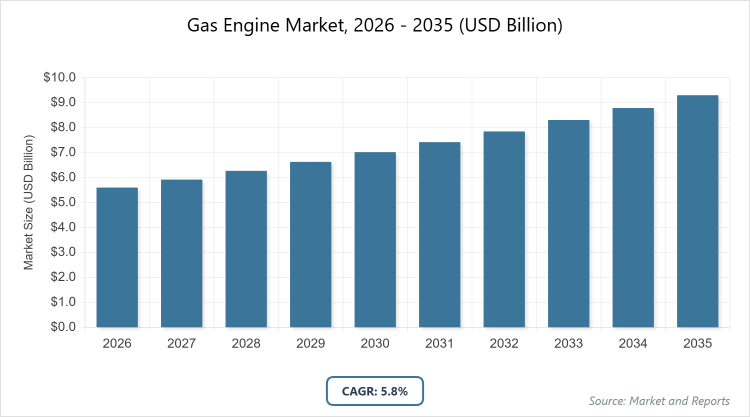

According to MarketnReports, the global Gas Engine market size was estimated at USD 5.6 billion in 2025 and is expected to reach USD 9.8 billion by 2035, growing at a CAGR of 5.8% from 2026 to 2035. The gas engine market is driven by increasing natural gas availability, demand for efficient power generation, and the transition to cleaner fuels in the industrial and utility sectors.

What are the Key Insights into Gas Engine?

- The global Gas Engine market was valued at USD 5.6 billion in 2025 and is projected to reach USD 9.8 billion by 2035.

- The market is expected to grow at a CAGR of 5.8% during the forecast period from 2026 to 2035.

- The market is driven by abundant natural gas supply, a shift toward cleaner fuels, cogeneration demand, and expansion in distributed power generation.

- In the type segment, natural gas engines dominate with a 62% share due to widespread availability and cost-effectiveness in power and mechanical applications.

- In the application segment, power generation dominates with a 45% share as it provides reliable baseload and peaking capacity with lower emissions.

- In the end-user segment, utilities & power generation dominate with a 38% share owing to large-scale deployment for grid stability and renewable integration.

- Asia Pacific dominates the regional market with a 40% share, driven by rapid industrialization, energy demand in China and India, and government support for gas infrastructure.

What is the Industry Overview of Gas Engine?

The Gas Engine market encompasses internal combustion engines powered by natural gas, biogas, or special gases, designed for reliable, efficient mechanical power and electricity generation across stationary and mobile applications. Market definition includes spark-ignited and dual-fuel engines that provide lower emissions than diesel alternatives, offering flexibility in fuel sourcing, cogeneration capabilities, and integration with renewable gas sources, while addressing challenges in emissions compliance, fuel quality variability, and operational efficiency in diverse industrial environments.

What are the Market Dynamics of Gas Engine?

Growth Drivers

The Gas Engine market is propelled by abundant natural gas reserves and falling prices, making it a cost-competitive alternative to diesel in power generation and industrial applications. The global push for cleaner energy sources favors gas engines for their lower CO2, NOx, and particulate emissions compared to liquid fuels, supporting compliance with tightening environmental regulations. Expansion of cogeneration (CHP) systems improves overall energy efficiency, reducing operational costs in manufacturing and commercial sectors. Rising demand for distributed and backup power in data centers, hospitals, and remote sites, along with biogas compatibility, further accelerates adoption. Government incentives for gas infrastructure and renewable gas blending enhance market penetration.

Restraints

High upfront capital costs for large-scale gas engine installations and infrastructure requirements limit adoption in developing regions with budget constraints. Fluctuations in natural gas prices and supply disruptions due to geopolitical factors create uncertainty for long-term investments. Stringent emissions regulations require expensive after-treatment systems, increasing total ownership costs. Competition from renewable energy sources like solar and wind, which offer zero-fuel costs, pressures market share in power generation. Limited biogas availability and upgrading costs hinder renewable gas engine deployment in some areas.

Opportunities

Opportunities arise from the transition to hydrogen and renewable natural gas blends, enabling future-proof engines for decarbonization goals. Expansion of microgrids and off-grid power in remote and developing regions creates demand for flexible gas engines. Partnerships between engine manufacturers and renewable gas producers can accelerate biogas adoption. Growth in data centers and EV charging infrastructure requires reliable backup power, opening new segments. Advancements in lean-burn and dual-fuel technologies improve efficiency and emissions, appealing to regulated markets.

Challenges

Challenges include competition from battery storage and renewables in peaking power applications, reducing baseload demand. Rapid evolution of emissions standards demands continuous R&D and retrofitting, straining manufacturer resources. Fuel quality variability, particularly with biogas, affects engine performance and longevity. Cybersecurity risks in connected engine controls threaten operational reliability. Talent shortages in gas engine maintenance and operation slow deployment in emerging markets.

Gas Engine Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Gas Engine Market |

| Market Size 2025 | USD 5.6 Billion |

| Market Forecast 2035 | USD 9.8 Billion |

| Growth Rate | CAGR of 5.8% |

| Report Pages | 190 |

| Key Companies Covered | Cummins Inc., Wärtsilä, INNIO Jenbacher, Caterpillar Inc., Rolls-Royce Power Systems, MAN Energy Solutions, Mitsubishi Heavy Industries, GE Vernova, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Gas Engine?

The Gas Engine market is segmented by type, application, end-user, and region.

By Type. Natural gas engines are the most dominant subsegment, holding approximately 62% market share, due to abundant supply, lower operating costs, and widespread infrastructure. This dominance drives the market by enabling reliable power generation and mechanical drive across industries, supporting energy transition goals. Special gas engines rank as the second most dominant, with around 20% share, accommodating biogas and syngas, propelling growth through renewable integration and waste-to-energy applications.

By Application. Power generation emerges as the most dominant subsegment, capturing about 45% share, primarily because it provides flexible, efficient electricity with low emissions. This leads to market growth by meeting baseload and peaking needs in utilities and distributed systems. Cogeneration follows as the second most dominant, with a roughly 25% share, offering combined heat and power efficiency, driving the market via energy cost savings in industrial facilities.

By End-User. Utilities & power generation represents the most dominant subsegment at about 38% share, driven by requirements for reliable grid support and renewable balancing. This dominance accelerates market expansion through large-scale deployments and policy support. Oil & gas industry ranks second most dominant, holding around 20% share, due to mechanical drive needs in extraction and processing, contributing to growth via operational efficiency.

What are the Recent Developments in Gas Engine?

- In February 2025, Cummins launched the X10 natural gas engine series compliant with 2027 EPA standards, targeting medium and heavy-duty applications with improved efficiency.

- In November 2024, Wärtsilä delivered two 34SG gas engines for a 15.5 MW captive power plant in Chennai, India, enhancing industrial power reliability.

- In October 2024, INNIO Jenbacher secured a contract for 50 MW hydrogen-ready gas engines at VPI’s Immingham energy hub in the UK.

- In August 2024, Caterpillar introduced hydrogen-blend capable gas engines for distributed generation, supporting decarbonization in utilities.

- In June 2024, Siemens Energy acquired a stake in a biogas upgrading firm to integrate renewable gas with its engine portfolio.

What is the Regional Analysis of Gas Engine?

- Asia Pacific to dominate the global market.

Asia Pacific holds the largest share at approximately 40%, with China as the dominating country, due to massive energy demand, rapid industrialization, and government support for gas infrastructure expansion. This region’s growth is fueled by increasing natural gas imports, coal-to-gas switching policies, and rising distributed power needs in manufacturing hubs, positioning it as the epicenter of gas engine consumption and production. India’s expanding power capacity and industrial growth drive demand for reliable mechanical drive engines.

Southeast Asian nations like Vietnam invest in gas-fired plants for energy security. Abundant labor and raw materials enable cost-effective manufacturing. Environmental policies push for cleaner gas engines in urban areas. Strong export orientation enhances global supply. Rising middle-class energy consumption increases backup power applications. Vocational training programs build operational expertise across the region.

North America follows closely, driven by shale gas abundance and distributed generation, where the United States dominates through its advanced energy sector and R&D investments. Growth stems from cogeneration in manufacturing and data centers, though higher costs moderate expansion compared to Asia. Canadian oil sands operations demand robust mechanical drive engines. Government incentives for clean energy promote biogas engines. The region’s focus on emissions reduction drives after-treatment innovations. Collaborations between utilities and manufacturers foster efficient solutions. Reshoring of manufacturing boosts industrial applications. A strong regulatory framework ensures high-quality deployments.

Europe exhibits strong performance with emphasis on sustainability and efficiency, led by Germany through its engineering excellence and transition from coal. The region’s expansion benefits from EU green deal policies favoring gas as a bridge fuel and focusing on CHP in district heating. Biogas engine adoption grows with renewable gas targets. The UK’s offshore wind integration requires flexible balancing power. Multilingual compliance aids diverse markets like France and Italy. Circular economy initiatives promote engine remanufacturing. Collaborative research networks advance hydrogen-ready technologies. Aging infrastructure renewal projects adopt gas engines for reliability. Vocational training ensures skilled workforce.

Latin America shows steady but moderate advancement, dominated by Brazil’s power and industrial sectors, supported by natural gas discoveries, though limited by economic fluctuations. Mexico benefits from U.S. gas supply ties, enhancing cross-border projects. Government energy reforms in Argentina promote gas-fired generation. The rise of renewables in Chile creates hybrid opportunities. However, infrastructure gaps affect deployment speed. Emerging oil & gas in Guyana demands mechanical drive engines. Regional trade agreements facilitate equipment imports. Vocational programs in Colombia build maintenance skills. Environmental concerns push for low-emission solutions. Urbanization drives distributed power demand.

The Middle East and Africa remain emerging, with Saudi Arabia and the UAE leading through energy diversification and infrastructure investments, constrained by lower industrialization but showing potential via power projects. Vision 2030 funds gas engine plants for grid reliability. South Africa’s mining and utilities adopt backup power. Technology transfers from European firms build local expertise in Egypt. However, fuel supply variability affects operations. Investments in solar-gas hybrids create hybrid applications. OPEC policies influence gas availability. Vocational initiatives in Nigeria train for future energy jobs. Emerging desalination plants require a reliable mechanical drive. Focusing on sustainable development promotes cleaner gas technologies.

What are the Key Market Players in Gas Engine?

- Cummins Inc. focuses on high-efficiency natural gas engines, investing in hydrogen-blend capabilities for future decarbonization.

- Wärtsilä. Wärtsilä specializes in flexible gas engines for power and marine, pursuing hybrid and renewable gas solutions.

- INNIO Jenbacher. INNIO emphasizes biogas and hydrogen-ready engines, targeting distributed generation with low emissions.

- Caterpillar Inc. develops durable gas engines for oil & gas and industrial use, focusing on reliability and service networks.

- Rolls-Royce Power Systems. Rolls-Royce offers mtu brand engines for backup and continuous power, strategizing on digital monitoring.

- MAN Energy Solutions. MAN targets large-bore engines for power plants, investing in low-emission technologies.

- Mitsubishi Heavy Industries. Mitsubishi focuses on high-output engines for utilities, expanding in the Asia-Pacific markets.

- GE Vernova. GE Vernova provides aeroderivative gas engines for fast-start applications, emphasizing grid stability.

What are the Market Trends in Gas Engine?

- Increasing hydrogen and biogas blending for decarbonization.

- Rise of hydrogen-ready engine designs.

- Growth in distributed and microgrid applications.

- Adoption of digital twins for predictive maintenance.

- Focus on low-emission after-treatment systems.

- Expansion of cogeneration in industrial sectors.

- Shift toward dual-fuel flexibility.

What Market Segments and Subsegments are Covered in the Gas Engine Report?

By Type

- Natural Gas Engines

- Special Gas Engines

- Biogas Engines

- Dual Fuel Engines

- Spark-Ignited Engines

- Compression-Ignited Engines

- Low-Speed Engines

- Medium-Speed Engines

- High-Speed Engines

- Lean-Burn Engines

- Others

By Application

- Power Generation

- Mechanical Drive

- Cogeneration

- Marine Propulsion

- Pump Drive

- Compressor Drive

- Oil & Gas Operations

- Distributed Generation

- Backup Power

- Combined Heat & Power

- Others

By End-User

- Utilities & Power Generation

- Oil & Gas Industry

- Manufacturing & Industrial

- Marine & Shipping

- Commercial & Institutional

- Agriculture

- Mining

- Transportation & Rail

- Data Centers

- Healthcare Facilities

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Gas Engines are internal combustion engines powered by natural gas, biogas, or special gases for power generation and mechanical drive with lower emissions.

Key factors include natural gas availability, cleaner fuel transition, cogeneration demand, and distributed power needs.

The market is projected to grow from USD 5.6 billion in 2025 to USD 9.8 billion by 2035.

The CAGR is expected to be 5.8%.

Asia Pacific will contribute notably, holding around 40% share due to industrialization and energy demand.

Major players include Cummins Inc., Wärtsilä, INNIO Jenbacher, Caterpillar Inc., and Rolls-Royce Power Systems.

The report provides detailed analysis of size, trends, segments, regional outlook, key players, and forecasts.

Stages include component sourcing, engine assembly, testing, distribution, installation, and after-sales service.

Trends evolve toward hydrogen-ready and biogas engines, with preferences for low-emission, efficient systems.

Emissions regulations and renewable gas mandates influence engine design and fuel blending.