Frozen Food Manufacturing Market Size, Share and Trends 2026 to 2035

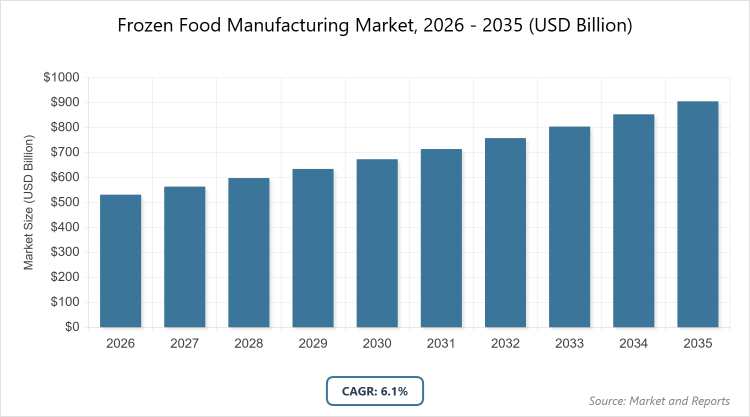

According to MarketnReports, the global Frozen Food Manufacturing market size was estimated at USD 531.5 billion in 2025 and is expected to reach USD 964.3 billion by 2035, growing at a CAGR of 6.1% from 2026 to 2035. Frozen Food Manufacturing Market is driven by increasing demand for convenient and ready-to-eat food options.

What is the Overview of Frozen Food Manufacturing Market?

The frozen food manufacturing market encompasses the production, processing, and packaging of food products that are preserved through freezing to extend shelf life while maintaining nutritional value, taste, and texture. This market involves a wide range of activities from sourcing raw ingredients to employing advanced freezing technologies like individual quick freezing (IQF) and blast freezing, ensuring products remain safe for consumption over extended periods. Market definition refers to the industry focused on creating frozen items such as ready meals, vegetables, meats, and desserts, catering to consumer needs for convenience, reduced food waste, and year-round availability of seasonal produce. It plays a crucial role in the global food supply chain by addressing urbanization-driven demands for quick-preparation foods and supporting food security in regions with limited fresh produce access.

What are the Key Insights into Frozen Food Manufacturing Market?

- The global frozen food manufacturing market was valued at USD 531.5 billion in 2025 and is projected to reach USD 964.3 billion by 2035.

- The market is expected to grow at a CAGR of 6.1% during the forecast period from 2026 to 2035.

- The market is driven by rising consumer preference for convenient, time-saving food solutions amid busy lifestyles and urbanization.

- In the product type segment, frozen ready meals dominate with a 35% share.

- This dominance is due to their convenience, variety of flavors, and alignment with fast-paced modern living, which boosts overall market growth by attracting working professionals and families seeking quick meal options.

- In the distribution channel segment, supermarkets/hypermarkets dominate with a 40% share.

- This is attributed to their widespread availability, extensive product ranges, and promotional strategies that enhance consumer accessibility and drive volume sales.

- In the end-user segment, residential users dominate with a 50% share.

- This stems from increasing home consumption trends, where households prioritize easy-to-prepare frozen foods for daily meals, supporting market expansion through repeat purchases.

- Europe dominates the global market with a 39% share.

- This is owing to high per capita consumption, advanced cold chain infrastructure, and strong demand in countries like the UK and Germany for premium frozen products.

What are the Market Dynamics in Frozen Food Manufacturing?

Growth Drivers

The growth drivers in the frozen food manufacturing market are primarily fueled by evolving consumer lifestyles that emphasize convenience and efficiency. Urbanization and the rise of dual-income households have significantly increased the demand for ready-to-eat and ready-to-cook frozen products, as they offer quick preparation without compromising on quality or nutrition. Technological advancements in freezing methods, such as IQF, have improved product quality by preserving taste, texture, and nutrients, making frozen foods more appealing than traditional preserved options.

Additionally, the expansion of e-commerce and organized retail channels has enhanced product accessibility, particularly in emerging markets where cold chain infrastructure is improving. Sustainability trends, including reduced food waste through longer shelf lives, further propel market growth by aligning with global efforts to minimize environmental impact.

Restraints

Restraints in the frozen food manufacturing market include high operational costs associated with maintaining cold chain logistics, which require substantial energy consumption and specialized equipment for storage and transportation. Perceptions among health-conscious consumers that frozen foods may contain preservatives or lose nutritional value compared to fresh alternatives pose a challenge, potentially limiting market penetration in premium segments. Supply chain vulnerabilities, such as disruptions from power outages or transportation delays, can lead to product spoilage and financial losses. Moreover, stringent regulatory requirements for food safety and labeling increase compliance burdens for manufacturers, particularly smaller players, hindering innovation and market entry in regulated regions.

Opportunities

Opportunities in the frozen food manufacturing market arise from the growing demand for plant-based and health-oriented frozen products, driven by rising veganism and wellness trends globally. Expansion into emerging economies in Asia-Pacific and Latin America presents untapped potential, where improving disposable incomes and retail infrastructure can boost adoption of frozen convenience foods. Innovations in sustainable packaging and eco-friendly freezing technologies offer avenues to attract environmentally aware consumers and comply with green regulations. The surge in online grocery platforms provides a platform for direct-to-consumer sales, enabling manufacturers to reach niche markets with customized offerings like organic or gluten-free frozen items.

Challenges

Challenges in the frozen food manufacturing market encompass fluctuating raw material prices, influenced by seasonal variations and climate change impacts on agriculture, which can affect production costs and profitability. Maintaining consistent product quality across global supply chains is difficult due to varying cold storage standards in different regions, leading to potential quality degradation. Intense competition from fresh and ambient food alternatives requires continuous innovation in product development to retain consumer interest. Environmental concerns over high energy use in freezing processes and plastic packaging waste add pressure to adopt sustainable practices, which may involve significant upfront investments for manufacturers.

Frozen Food Manufacturing Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Frozen Food Manufacturing Market |

| Market Size 2025 | USD 531.5 Billion |

| Market Forecast 2035 | USD 964.3 Billion |

| Growth Rate | CAGR of 6.1% |

| Report Pages | 235 |

| Key Companies Covered |

Nestlé, Conagra Brands, Tyson Foods, General Mills, Unilever, and Others |

| Segments Covered | By Product Type, By Distribution Channel, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

The Frozen Food Manufacturing market is segmented by product type, distribution channel, end-user, and region.

Based on Product Type Segment, the most dominant subsegment is frozen ready meals, while the second most dominant is frozen fruits and vegetables. Frozen ready meals lead due to their unparalleled convenience for time-strapped consumers, offering diverse cuisines and portion-controlled options that reduce cooking time and food waste, thereby driving market growth through high repeat purchase rates and alignment with urban lifestyles; meanwhile, frozen fruits and vegetables rank second as they appeal to health-focused buyers seeking nutrient-rich, seasonal produce year-round, contributing to overall expansion by supporting wellness trends and enabling manufacturers to innovate with organic variants.

Based on Distribution Channel Segment, the most dominant subsegment is supermarkets/hypermarkets, while the second most dominant is online retail. Supermarkets/hypermarkets dominate owing to their extensive shelf space, promotional displays, and one-stop shopping appeal that facilitate impulse buys and bulk purchases, propelling market growth by enhancing visibility and accessibility for a broad consumer base; online retail follows as the second dominant, driven by the rise of e-commerce platforms offering home delivery and subscription models, which boost the market through convenience for tech-savvy shoppers and expanded reach in remote areas.

Based on End-User Segment, the most dominant subsegment is residential, while the second most dominant is HoReCa (hotels, restaurants, and catering). Residential users lead because of increasing home-based consumption patterns where families and individuals prefer frozen foods for everyday meals due to ease of storage and preparation, fueling market growth via consistent demand and product diversification; HoReCa ranks second as it relies on frozen items for efficient inventory management and menu consistency, driving the market by supporting large-scale operations and innovations in premium frozen offerings for commercial use.

What are Recent Developments in Frozen Food Manufacturing?

- In January 2026, Conagra Brands released its “Future of Frozen Food 2026” report, highlighting trends like protein-packed meals and restaurant-inspired frozen options, which is expected to guide industry strategies for innovation and consumer engagement.

- In 2025, Nestlé expanded its plant-based frozen food line with new IQF technology implementations in its manufacturing facilities across Europe, aiming to meet rising demand for sustainable and vegan products while enhancing product quality and shelf life.

- In late 2024, Tyson Foods acquired a smaller frozen seafood manufacturer to bolster its portfolio, focusing on sustainable sourcing practices to address environmental concerns and strengthen its position in the North American market.

- In 2025, General Mills invested in advanced blast freezing equipment for its bakery products division, improving energy efficiency and reducing production costs, which supports broader industry efforts toward sustainability.

What is the Regional Analysis for Frozen Food Manufacturing Market?

- Europe to dominate the global market.

North America holds a significant share in the frozen food manufacturing market, driven by high consumer demand for convenience foods and a well-established cold chain infrastructure. The region’s growth is fueled by busy lifestyles, technological innovations in freezing processes, and a strong presence of key players like Tyson Foods and Conagra Brands. The United States dominates within North America, accounting for the majority of the regional market due to its large population, high disposable incomes, and extensive retail networks such as Walmart and Costco, which promote frozen products through promotions and variety. Canada contributes through its focus on export-oriented manufacturing, while Mexico benefits from increasing urbanization and NAFTA-related trade facilitations, though challenges like energy costs persist.

Europe dominates the global frozen food manufacturing market with the highest share, attributed to mature consumer preferences for premium frozen items and advanced distribution systems. The region’s emphasis on food safety regulations and sustainability drives innovation in eco-friendly packaging and organic frozen foods. Germany leads as the dominating country, supported by its efficient manufacturing hubs, high per capita consumption of frozen ready meals, and companies like Dr. Oetker leading in bakery products. The UK and France follow closely, with strong demand in urban areas for convenience foods amid rising health awareness, while Eastern European countries like Poland offer growth potential through expanding retail infrastructure, despite restraints from economic disparities.

Asia Pacific is the fastest-growing region in the frozen food manufacturing market, propelled by rapid urbanization, rising middle-class populations, and improving cold chain logistics. Increasing adoption of Western diets and e-commerce platforms accelerates demand for frozen snacks and meals. China dominates within the region, driven by its massive consumer base, government investments in food processing, and companies like Sanquan Food expanding production capacities. India contributes through growing organized retail and demand for frozen vegetables, while Japan focuses on premium seafood products, supported by technological advancements; however, challenges include inconsistent infrastructure in rural areas.

Latin America exhibits steady growth in the frozen food manufacturing market, influenced by improving economic conditions and shifting consumer habits toward convenient foods. The region’s tropical climate boosts demand for frozen fruits and seafood to preserve freshness. Brazil dominates as the key country, with its large agriculture sector supplying raw materials and companies like BRF S.A. leading in meat products, aided by export opportunities. Mexico benefits from proximity to North American markets, while Argentina focuses on bakery items; growth is tempered by supply chain inefficiencies and regulatory hurdles.

The Middle East and Africa (MEA) region shows emerging potential in the frozen food manufacturing market, driven by urbanization and tourism-related demand in food service sectors. Investments in cold storage facilities are key to overcoming infrastructural challenges. South Africa dominates within MEA, supported by its developed retail sector and companies like Irvin & Johnson focusing on seafood, while the UAE benefits from high expatriate populations demanding imported frozen goods; however, the region faces restraints from high import dependencies and environmental concerns over energy use.

Who are the Key Market Players in Frozen Food Manufacturing?

Nestlé focuses on innovation in plant-based and health-oriented frozen products, leveraging its global R&D network to introduce sustainable packaging and expand into emerging markets through acquisitions and partnerships, enhancing its competitive edge in premium segments.

Conagra Brands emphasizes consumer trends like high-protein meals via data-driven reports and product launches, investing in efficient manufacturing technologies to reduce costs and broaden its portfolio in frozen snacks and meals for North American dominance.

Tyson Foods prioritizes sustainable sourcing and vertical integration in its supply chain, expanding frozen meat and poultry offerings through mergers and advanced freezing techniques to meet demand for convenient protein options worldwide.

General Mills adopts a strategy of diversifying into organic and gluten-free frozen bakery products, utilizing marketing campaigns and e-commerce collaborations to target health-conscious consumers and strengthen its position in retail channels.

Unilever pursues growth through eco-friendly initiatives and brand expansions in frozen desserts and meals, focusing on digital marketing and supply chain optimizations to capture market share in Europe and Asia Pacific.

Nomad Foods concentrates on acquisitions of regional brands to build a diverse frozen portfolio, emphasizing operational efficiencies and innovation in ready meals to drive penetration in mature European markets.

What are the Market Trends in Frozen Food Manufacturing?

– Increasing focus on high-protein frozen meals to cater to health and fitness enthusiasts.

- Rise in restaurant-inspired frozen options for at-home convenience.

- Growing demand for plant-based and vegan frozen products amid sustainability trends.

- Adoption of premium, minimally processed frozen foods with clean labels.

- Expansion of portion-controlled and family-style frozen solutions for diverse household needs.

- Integration of sustainable packaging to reduce environmental impact.

- Surge in e-commerce sales of frozen goods with improved delivery logistics.

- Emphasis on all-day breakfast frozen items for flexible meal times.

What Market Segments and Subsegments are Covered in the Frozen Food Manufacturing Report?

By Product Type

-

- Frozen Ready Meals

- Frozen Fruits

- Frozen Vegetables

- Frozen Meat

- Frozen Poultry

- Frozen Seafood

- Frozen Bakery Products

- Frozen Desserts

- Frozen Snacks

- Frozen Potatoes

- Others

By Distribution Channel

-

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail

- Food Service Outlets

- Independent Retailers

- Departmental Stores

- Discount Stores

- Club Stores

- Pharmacies

- Others

By End-User

-

- Residential

- Commercial

- Institutional

- Food Processing Industry

- HoReCa

- Quick Service Restaurants

- Full Service Restaurants

- Caterers

- Hospitals

- Schools

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Frozen Food Manufacturing Market - Industry Analysis

Chapter 4. Global Frozen Food Manufacturing Market- Competitive Landscape

Chapter 5. Global Frozen Food Manufacturing Market - Product Type Analysis

Chapter 6. Global Frozen Food Manufacturing Market - Distribution Channel Analysis

Chapter 7. Global Frozen Food Manufacturing Market - End-User Analysis

Chapter 8. Frozen Food Manufacturing Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Frozen food manufacturing involves the process of producing, processing, and packaging food items that are preserved by freezing to maintain quality, nutrition, and extend shelf life for consumer convenience.

Key factors include rising demand for convenience foods, advancements in freezing technologies, urbanization, health trends toward plant-based options, and expansion of e-commerce and cold chain infrastructure.

The Frozen Food Manufacturing market is projected to grow from approximately USD 531.5 billion in 2025 to USD 964.3 billion by 2035.

The Frozen Food Manufacturing market is expected to register a CAGR of 6.1% during the forecast period from 2026 to 2035.

Europe will contribute notably, holding around 39% of the market share due to high consumption and advanced infrastructure.

Major players include Nestlé, Conagra Brands, Tyson Foods, General Mills, Unilever, and Nomad Foods, which drive growth through innovation and strategic expansions.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, and forecasts to guide stakeholders in decision-making.

The value chain includes production (sourcing raw materials), processing (cleaning, cutting, and freezing), distribution (cold storage and logistics), and consumption (retail and end-user delivery).

Trends are shifting toward high-protein, plant-based, and sustainable products, with consumers preferring clean-label, convenient options that align with health and eco-conscious lifestyles.

Regulatory factors include strict food safety standards like FDA and EU regulations on labeling and preservatives, while environmental factors involve energy-intensive cold chains contributing to carbon footprints, pushing for sustainable practices and eco-friendly packaging.