Foot Orthotic Insoles Market Size, Share and Trends 2026 to 2035

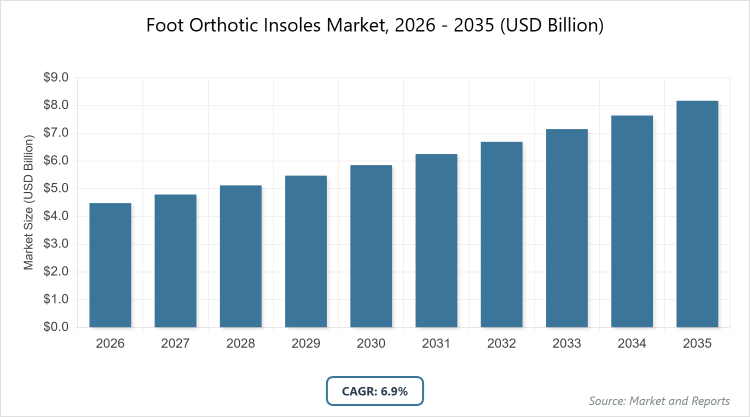

According to our latest research, the global foot orthotic insoles market size reached USD 4.48 billion in 2026, demonstrating robust expansion. The market is poised to grow at a CAGR of 6.9% from 2026 to 2035, with the market projected to reach USD 8.22 billion by 2035.

This significant growth is propelled by the increasing prevalence of chronic foot-related conditions such as diabetes, plantar fasciitis, and arthritis, coupled with a growing geriatric population and rapid technological advancements in 3D printing and custom digital fabrication.

What are the Key Insights into the Foot Orthotic Insoles Market?

- The global foot orthotic insoles market is projected to grow from approximately USD 4.48 billion in 2026 to USD 8.22 billion by 2035, reflecting a compound annual growth rate (CAGR) of around 6.9%.

- Among types, the customized segment dominates, offering personalized fit for specific foot conditions.

- In material segments, thermoplastics hold the leading position, prized for durability and moldability.

- By distribution channel, hospitals and specialty clinics are the most prominent, driven by professional recommendations.

- North America emerges as the dominant region, contributing the largest market share due to advanced healthcare and high awareness.

What is the Foot Orthotic Insoles Industry?

Industry Overview

The foot orthotic insoles industry encompasses the design, manufacturing, and distribution of specialized shoe inserts aimed at providing arch support, correcting biomechanical imbalances, alleviating foot pain, and enhancing overall comfort for individuals with conditions such as flat feet, plantar fasciitis, diabetes-related issues, or sports-induced strains. These insoles, available in prefabricated or custom-molded forms, are crafted from materials like thermoplastics, foams, gels, or composite fibers to redistribute pressure, improve gait, and prevent injuries, serving both therapeutic and preventive purposes in medical, athletic, and everyday applications.

Positioned at the intersection of healthcare, orthopedics, and consumer wellness, the market focuses on personalization through technologies like 3D scanning and printing, while addressing diverse needs from elderly care to athletic performance, ultimately promoting mobility and quality of life amid growing health consciousness.

What Drives the Foot Orthotic Insoles Market?

Growth Drivers

The foot orthotic insoles market is fueled by the escalating prevalence of foot disorders linked to aging populations, obesity, and sedentary lifestyles, coupled with heightened awareness of preventive healthcare that encourages adoption for pain management and posture correction. Technological innovations, such as 3D-printed custom insoles and smart sensors for real-time monitoring, enhance product efficacy and appeal to tech-savvy consumers in sports and fitness sectors. Additionally, expanding e-commerce platforms and retail accessibility, alongside supportive insurance reimbursements in developed regions, broaden market reach, driving demand through affordable, tailored solutions that cater to diverse demographics and promote long-term foot health.

Restraints

High costs associated with custom orthotic insoles, including fitting consultations and premium materials, restrict affordability for low-income groups, particularly in emerging economies with limited healthcare coverage. Lack of standardization and varying quality in prefabricated options lead to consumer dissatisfaction and hesitation, while competition from alternative therapies like physical exercises or over-the-counter pain relievers dilutes market share. Furthermore, supply chain disruptions for raw materials and regulatory delays in product approvals increase operational expenses, impeding growth for smaller manufacturers.

Opportunities

The integration of sustainable and bio-based materials opens pathways for eco-friendly insoles, aligning with consumer preferences for green products and enabling premium positioning in environmentally conscious markets. Rising sports participation and athletic endorsements create demand for performance-enhancing insoles, while untapped potential in developing regions through mobile health clinics and online customization platforms facilitates expansion. Moreover, partnerships with podiatrists and telemedicine services offer innovative delivery models, capitalizing on digital health trends to reach remote consumers.

Challenges

Stringent regulatory requirements for medical-grade insoles, including certifications for safety and efficacy, elevate compliance costs and prolong market entry for new entrants. Consumer education gaps regarding proper usage and benefits result in underutilization, compounded by counterfeit products eroding trust in unregulated markets. Additionally, economic fluctuations affecting disposable incomes challenge sustained demand, necessitating adaptive pricing strategies amid raw material price volatility.

Foot Orthotic Insoles Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Foot Orthotic Insoles Market |

| Market Size 2025 | USD 4.48 Billion |

| Market Forecast 2035 | USD 8.22 Billion |

| Growth Rate | CAGR of 6.9% |

| Report Pages | 215 |

| Key Companies Covered | Superfeet Worldwide, Inc., Aetrex Worldwide, Inc, Birkenstock Digital GmbH, Reckitt Benckiser Group PLC (Scholl’s), Ottobock SE & Co. KGaA, Össur hf, and Bauerfeind AG |

| Segments Covered | By Type, By Material, By Distribution Channel, By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Foot Orthotic Insoles Market Segmented?

The foot orthotic insoles market is segmented by type, material, distribution channel, and region.

By type, including prefabricated and customized, with customized emerging as the most dominant due to its tailored design that addresses individual biomechanical needs, providing superior comfort and efficacy for chronic conditions like plantar fasciitis; this dominance drives the market by commanding higher prices and fostering loyalty through personalized healthcare, while prefabricated ranks as the second most dominant, offering cost-effective, ready-to-use options for mild issues, supporting growth via mass accessibility and quick retail availability.

By material, the market divides into thermoplastics, ethyl-vinyl acetate (EVA), foams, composite carbon fibers, and others, where thermoplastics dominates owing to its heat-moldable properties, durability, and lightweight nature ideal for custom fitting; its prevalence propels market expansion by enabling versatile applications in medical and sports, whereas composite carbon fibers follows as the second dominant, valued for rigidity and energy return in athletic use, contributing through performance enhancements and premium segments.

By distribution channel, segments include hospitals and specialty clinics, drug stores, online, and others, with hospitals and specialty clinics leading as they provide expert consultations and prescriptions, driving trust and compliance; this segment fuels dynamics by integrating with healthcare systems, while online secures second place, surging with convenience and direct-to-consumer models, broadening reach amid digital trends.

What are the Recent Developments in the Foot Orthotic Insoles Market?

- In November 2023, Upstep launched the first AI-powered technology system for customized insoles, enabling users to create personalized orthotics via app-based foot scans, revolutionizing accessibility and boosting market innovation in digital health solutions.

- In mid-2024, Scholl’s Wellness Co. introduced a new line of sustainable EVA-based insoles with recycled materials, targeting eco-conscious consumers and aligning with global sustainability trends to enhance brand positioning.

- In early 2025, Ottobock expanded its custom orthotic portfolio through a partnership with 3D printing firms, offering faster production times for medical-grade insoles, catering to rising demand in orthopedic clinics.

How Does Regional Performance Vary in the Foot Orthotic Insoles Market?

- North America to dominate the market

North America dominates the foot orthotic insoles market, supported by advanced healthcare infrastructure, high prevalence of foot disorders from obesity and aging, and strong insurance coverage for orthotics; the United States leads this region with widespread podiatry services, innovative 3D customization, and major retail chains promoting awareness, driving exports and domestic growth amid sports culture. Canada complements with similar reimbursement policies and focus on diabetic care, while rising telehealth integrations further accelerate adoption across diverse demographics.

Europe exhibits robust growth through emphasis on preventive care and regulatory standards for medical devices; Germany stands out as the dominating country, leveraging engineering expertise for high-quality composites and exports, while the UK and France contribute via national health programs addressing diabetic foot care. Italy and Nordic countries add to regional strength with wellness-focused lifestyles, supported by EU-funded research in biomechanics and increasing elderly population needs.

Asia Pacific emerges dynamically, propelled by urbanization and rising disposable incomes; China predominates with massive manufacturing and increasing diabetes rates, fostering affordable prefabricated options, supported by Japan’s tech integrations in smart insoles. India accelerates through e-commerce and growing middle-class health spending, with South Korea contributing advanced material innovations for athletic applications.

Latin America advances moderately amid healthcare improvements; Brazil excels with urban foot health campaigns and agricultural worker needs, promoting local production of EVA insoles. Mexico supports growth via trade integrations and rising awareness, bolstered by expanding private clinics and cross-border medical tourism trends.

The Middle East & Africa region shows nascent expansion, focused on diabetes management; the United Arab Emirates leads via luxury wellness sectors and imports of custom orthotics, with South Africa growing through public health initiatives and urban lifestyles. Saudi Arabia enhances potential through Vision 2030 healthcare investments, though affordability and distribution remain key challenges in broader African markets.

Who are the Key Market Players in the Foot Orthotic Insoles Industry?

- Superfeet Worldwide, Inc. invests in sustainable materials and athlete endorsements, expanding via e-commerce for performance insoles.

- Aetrex Worldwide, Inc. focuses on 3D scanning tech for custom fits, partnering with retailers for global reach.

- Birkenstock Digital GmbH emphasizes ergonomic designs and brand loyalty, leveraging direct sales for premium cork-based products.

- Reckitt Benckiser Group PLC (Scholl’s) pursues mass-market innovation with odor-control features, using advertising for consumer awareness.

- Ottobock SE & Co. KGaA adopts medical-grade R&D, collaborating with clinics for prosthetic-integrated insoles.

- Össur hf prioritizes biomechanical research, targeting sports segments through acquisitions.

- Bauerfeind AG diversifies into compression-enhanced insoles, focusing on European exports.

What are the Current Market Trends in Foot Orthotic Insoles?

- Adoption of 3D printing for rapid custom insoles, reducing lead times and costs.

- Integration of smart sensors for gait analysis and app connectivity.

- Shift toward sustainable, bio-based materials like recycled EVA.

- Growth in e-commerce with virtual fitting tools.

- Focus on diabetic-friendly designs with pressure-relief features.

- Rise in athletic-specific insoles for injury prevention.

- Expansion of over-the-counter options in pharmacies.

What Market Segments are Covered in the Report?

By Type

-

- Prefabricated

- Customized

By Material

-

- Thermoplastics

- Ethyl-Vinyl Acetate (EVA)

- Foams

- Composite Carbon Fibers

- Others

By Distribution Channel

-

- Hospitals and Specialty Clinics

- Drug Stores

- Online

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Foot orthotic insoles are shoe inserts designed to support foot arches, correct alignment, relieve pain, and improve mobility for various conditions.

Key factors include aging populations, rising foot disorders, technological advancements, e-commerce growth, and sustainability trends.

The market is projected to grow from approximately USD 4.48 billion in 2026 to USD 8.22 billion by 2035, driven by health awareness.

The CAGR is expected to be around 6.9% from 2026 to 2035, indicating robust expansion.

North America will contribute notably, holding the largest share due to advanced infrastructure and disorder prevalence.

Major players include Superfeet Worldwide, Inc., Aetrex Worldwide, Inc, Birkenstock Digital GmbH, Reckitt Benckiser Group PLC (Scholl's), Ottobock SE & Co. KGaA, Össur hf, and Bauerfeind AG, driving through innovation.

The report offers insights into size, trends, segmentation, regions, players, and forecasts for informed strategies.

Stages include raw material sourcing, manufacturing/molding, distribution, retail sales, and after-sales fitting services.

Trends evolve toward smart, sustainable, and customized designs, with consumers preferring tech-integrated and eco-friendly options.

Regulations on medical devices ensure safety but raise costs; environmental pushes for recyclables drive green innovations.