Food Processing and Handling Equipment Market Size, Share and Trends 2026 to 2035

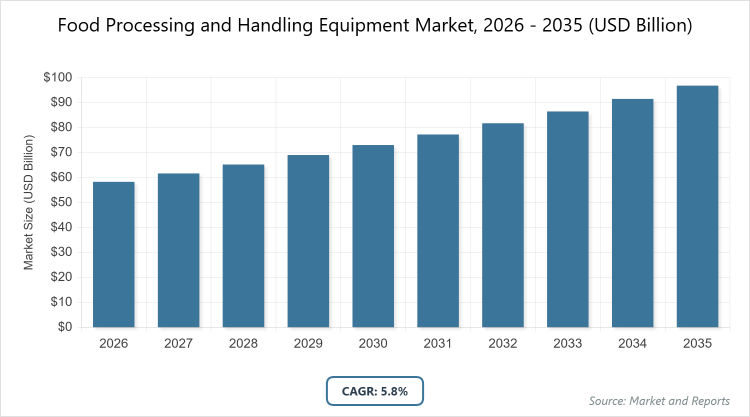

According to MarketnReports, the global Food Processing and Handling Equipment market size was estimated at USD 58.3 billion in 2025 and is expected to reach USD 102.7 billion by 2035, growing at a CAGR of 5.8% from 2026 to 2035. The Food Processing and Handling Equipment Market is driven by increasing demand for processed foods and automation in the food industry.

What are the Key Insights into Food Processing and Handling Equipment?

- The global Food Processing and Handling Equipment market was valued at USD 58.3 billion in 2025 and is projected to reach USD 102.7 billion by 2035.

- The market is expected to grow at a CAGR of 5.8% during the forecast period from 2026 to 2035.

- The market is driven by rising processed food consumption, food safety regulations, automation trends, and expansion in emerging markets.

- In the type segment, filling & packaging machines dominate with a 30% share due to their critical role in ensuring product integrity and efficiency in high-volume production.

- In the application segment, bakery & confectionery dominates with a 25% share as it requires precise equipment for mixing and baking to meet consumer demand for ready-to-eat products.

- In the end-user segment, food manufacturing companies dominate with a 40% share owing to large-scale operations needing advanced equipment for cost optimization.

- Asia Pacific dominates the regional market with a 35% share, driven by rapid urbanization, growing food industry in China and India, and low-cost manufacturing.

What is the Industry Overview of Food Processing and Handling Equipment?

The Food Processing and Handling Equipment market encompasses machinery and systems designed to transform raw ingredients into consumable products through operations like mixing, cutting, packaging, and preservation, ensuring safety, efficiency, and quality in food production chains. Market definition includes equipment for handling, preparing, and packaging food items, utilizing technologies like automation, robotics, and IoT for hygienic processing, waste reduction, and compliance with food safety standards, while addressing challenges in energy consumption, customization for diverse food types, and integration with supply chains for enhanced productivity in global food manufacturing.

What are the Market Dynamics of Food Processing and Handling Equipment?

Growth Drivers

The Food Processing and Handling Equipment market is propelled by the surging global demand for processed and convenience foods, where advanced equipment enables efficient production lines that reduce labor costs, minimize waste, and ensure consistent quality through automation and precision controls, catering to urban lifestyles and busy consumers. Stringent food safety regulations from bodies like FDA and EU standards mandate hygienic, traceable processing, driving investments in stainless steel and IoT-integrated machines for real-time monitoring. Rising e-commerce for food delivery increases need for packaging equipment, while technological advancements in robotics and AI optimize operations in large-scale facilities. Government incentives for food industry modernization in developing regions further accelerate adoption by enhancing competitiveness.

Restraints

High capital investment for advanced equipment, including installation and training, limits adoption among small and medium enterprises in developing regions, where traditional methods remain cost-effective. Volatility in raw material prices for steel and components increases manufacturing costs, impacting profitability. Strict regulatory compliance for hygiene and safety requires frequent upgrades, adding burdens. Supply chain disruptions from global events affect component availability, while competition from low-cost imports pressures pricing in mature markets.

Opportunities

Opportunities arise from integrating AI and IoT for smart equipment that predicts maintenance and optimizes energy use, appealing to sustainability-focused industries and attracting investments in green processing. Expansion into emerging markets with growing middle classes offers potential for affordable, modular systems tailored to local food types. Partnerships with food tech startups for innovative packaging can differentiate offerings, while the rise of plant-based foods creates demand for specialized processing lines. Government incentives for food security in Asia and Africa open avenues for localized production.

Challenges

Challenges include ensuring equipment adaptability to diverse food types, requiring R&D to prevent contamination or damage in sensitive processing like dairy or fruits. Rapid technological obsolescence demands continuous innovation, straining resources for smaller players. Skill gaps in skilled maintenance for automated systems hinder operations, while environmental concerns over energy consumption necessitate low-impact designs. Varying global food safety standards complicate international expansion.

Food Processing and Handling Equipment Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Food Processing and Handling Equipment Market |

| Market Size 2025 | USD 58.3 Billion |

| Market Forecast 2035 | USD 102.7 Billion |

| Growth Rate | CAGR of 5.8% |

| Report Pages | 220 |

| Key Companies Covered | Tetra Pak International S.A., Buhler AG, GEA Group AG, JBT Corporation, Key Technology, Inc., Alfa Laval AB, SPX FLOW, Inc., Marel hf., and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Food Processing and Handling Equipment?

The Food Processing and Handling Equipment market is segmented by type, application, end-user, and region.

By Type. Filling & packaging machines are the most dominant subsegment, holding approximately 30% market share, due to their essential role in product preservation and compliance with labeling standards. This dominance drives the market by enabling high-speed, hygienic packaging that meets e-commerce and export demands, reducing spoilage. Mixers & blenders rank as the second most dominant, with around 20% share, offering versatility for ingredient blending, propelling growth through efficiency in bakery and dairy processing.

By Application. Bakery & confectionery emerges as the most dominant subsegment, capturing about 25% share, primarily because it requires precise temperature and mixing control for quality products. This leads to market growth by catering to the rising demand for baked goods and snacks. Meat & poultry processing follows as the second most dominant, with roughly 20% share, ensuring hygienic handling, driving the market via food safety compliance.

By End-User. Food manufacturing companies represent the most dominant subsegment at about 40% share, driven by large-scale production needs. This dominance accelerates market expansion through automation for cost reduction. Beverage producers rank second most dominant, holding around 15% share for bottling lines, contributing to growth via high-volume efficiency.

What are the Recent Developments in Food Processing and Handling Equipment?

- In January 2025, Tetra Pak launched an AI-integrated packaging line for dairy, improving efficiency by 20%.

- In December 2024, Buhler Group expanded its sorting equipment with optical sensors for grain processing.

- In November 2024, GEA Group partnered with a startup for robotic meat slicing systems.

- In October 2024, JBT Corporation introduced energy-efficient freezers for seafood.

- In September 2024, Key Technology released a new vibratory conveyor for snack foods.

What is the Regional Analysis of Food Processing and Handling Equipment?

- Asia Pacific to dominate the global market.

Asia Pacific holds the largest share at approximately 35%, with China as the dominating country, due to rapid urbanization and food industry growth. This region’s expansion is fueled by low-cost labor and investments in processing plants, positioning it as a production hub. High population density drives demand for convenience foods. India’s food export growth boosts packaging needs. Southeast Asian nations like Thailand adopt for seafood processing. Environmental regulations push for efficient washing equipment. Strong supply chains enable quick customization.

North America follows with steady growth, driven by automation and food safety standards, where the United States dominates through tech innovations. Growth stems from e-commerce and convenience food demand. Canada’s dairy industry uses advanced homogenizers. Government rebates support energy-efficient upgrades. The region’s focus on organic foods increases washing equipment demand. Venture capital funds startups in robotics.

Europe exhibits strong performance with emphasis on sustainability, led by Germany through engineering firms. The region’s expansion benefits from EU regulations and organic trends. The UK’s snack industry adopts filling machines. France’s wine sector uses specialized washing systems. Italy and Spain focus on olive oil processing. Circular economy policies recycle equipment parts.

Latin America shows moderate advancement, dominated by Brazil’s agro-processing, supported by exports though limited by infrastructure. Mexico benefits from NAFTA ties for beverage equipment. Government plans in Argentina promote meat processing. Chile’s fruit exports drive sorting systems. However, economic volatility affects investments. Emerging cooperatives share equipment resources.

The Middle East and Africa remain emerging, with South Africa leading through food exports, constrained by water scarcity but promising via diversification. Saudi Arabia’s Vision 2030 funds dairy plants. Egypt’s affordable processing grows in rural areas. UAE’s hospitality sector adopts for commercial kitchens. However, power issues slow adoption. International aid supports training programs.

What are the Key Market Players in Food Processing and Handling Equipment?

- Tetra Pak International S.A. Tetra Pak focuses on aseptic packaging, expanding through sustainable materials.

- Buhler AG. Buhler emphasizes grain processing, investing in digital twins for optimization.

- GEA Group AG. GEA specializes in dairy equipment, pursuing energy-efficient designs.

- JBT Corporation. JBT offers freezing solutions, strategizing on food safety integrations.

- Key Technology, Inc. develops sorting systems, focusing on AI enhancements.

- Alfa Laval AB. Alfa Laval invests in heat exchangers, expanding in beverage processing.

- SPX FLOW, Inc. SPX FLOW targets mixing equipment, pursuing hygienic innovations.

- Marel hf. Marel focuses on poultry processing, emphasizing robotics.

What are the Market Trends in Food Processing and Handling Equipment?

- Increasing automation with robotics for labor reduction.

- Rise of sustainable and energy-efficient machines.

- Adoption of AI for predictive maintenance.

- Growth in hygienic designs for food safety.

- Expansion of modular equipment for flexibility.

- Integration with IoT for real-time monitoring.

What Market Segments and Subsegments are Covered in the Food Processing and Handling Equipment Report?

By Type

- Mixers & Blenders

- Cutting & Slicing Equipment

- Filling & Packaging Machines

- Washing & Cleaning Equipment

- Drying & Dehydrating Machines

- Sorting & Grading Equipment

- Cooking & Baking Ovens

- Freezing & Cooling Systems

- Homogenizers

- Extruders

- Others

By Application

- Bakery & Confectionery

- Meat & Poultry Processing

- Dairy Products Processing

- Beverages Processing

- Fruits & Vegetables Processing

- Seafood Processing

- Convenience Foods

- Snack Foods

- Pharmaceutical Processing

- Pet Food Processing

- Others

By End-User

- Food Manufacturing Companies

- Commercial Kitchens

- Pharmaceutical Companies

- Beverage Producers

- Dairy Farms & Processors

- Meat Processing Plants

- Bakery & Confectionery Units

- Fruit & Vegetable Processors

- Seafood Processors

- Pet Food Manufacturers

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Food Processing and Handling Equipment are machines used to transform raw ingredients into processed foods through operations like mixing, packaging, and preservation.

Key factors include processed food demand, automation trends, and food safety regulations.

The market is projected to grow from USD 58.3 billion in 2025 to USD 102.7 billion by 2035.

The CAGR is expected to be 5.8%.

Asia Pacific will contribute notably, holding around 35% share due to food industry growth.

Major players include Tetra Pak International S.A., Buhler AG, GEA Group AG, JBT Corporation, and Key Technology, Inc.

The report provides comprehensive analysis of size, trends, segments, regions, players, and forecasts.

Stages include design, manufacturing, assembly, distribution, installation, and maintenance.

Trends evolve toward automation and sustainability, with preferences for hygienic, efficient equipment.

Food safety regulations and environmental standards for energy efficiency influence design and adoption.