Flexible Office Market Size, Share and Trends 2026 to 2035

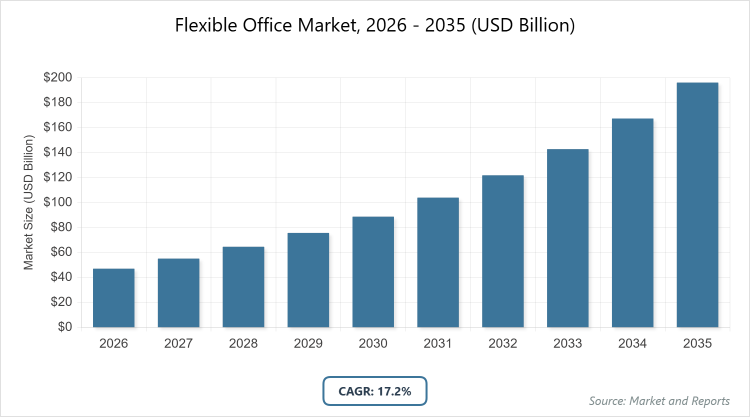

According to MarketnReports, the global Flexible Office market size was estimated at USD 47.02 billion in 2025 and is expected to reach USD 229.91 billion by 2035, growing at a CAGR of 17.20% from 2026 to 2035. Flexible Office Market is driven by the rising adoption of hybrid work models and demand for cost-effective workspace solutions.

What is the Industry Overview of the Flexible Office Market?

The Flexible Office Market encompasses workspaces that offer adaptable leasing terms, shared amenities, and scalable environments, catering to diverse needs from short-term desks to private suites, enabling businesses to avoid long-term commitments while accessing professional facilities. This market supports modern work dynamics by providing coworking spaces, serviced offices, and virtual setups that integrate technology, collaboration tools, and wellness features to enhance productivity and employee satisfaction.

It addresses the shift towards agile operations in a post-pandemic era, where remote and hybrid models prevail, reducing overhead costs and fostering innovation through community-driven ecosystems. The market definition includes all flexible real estate solutions, excluding traditional fixed leases, driven by urbanization, gig economy growth, and corporate strategies for portfolio optimization, ensuring accessibility for startups, enterprises, and freelancers alike.

What are the Key Insights into the Flexible Office Market?

- The global Flexible Office Market size was estimated at USD 47.02 Billion in 2025 and is expected to reach USD 229.91 Billion by 2035.

- Growing at a CAGR of 17.20% from 2026 to 2035.

- The Flexible Office Market is driven by the rising adoption of hybrid work models, demand for cost-effective and scalable workspaces, and increasing focus on employee well-being amid urbanization.

- Dominated subsegment in Type: Private Offices with 45% share, because of their appeal to enterprises seeking dedicated, secure spaces with flexible terms that balance privacy and collaboration.

- Dominated subsegment in Application: IT and Communications with 35% share, because of the sector’s need for agile environments supporting remote teams and rapid scaling in tech hubs.

- Dominated subsegment in End-User: Large Enterprises with 50% share, because of their shift towards portfolio optimization and cost savings through flexible leasing in volatile economic conditions.

- Dominated region: North America with 41% share, because of advanced infrastructure, high corporate adoption of hybrid models, and presence of major operators in the United States.

What are the Market Dynamics of the Flexible Office Market?

Growth Drivers

The growth drivers for the Flexible Office Market include the widespread adoption of hybrid and remote work models, which necessitate adaptable spaces that allow companies to scale operations without long-term financial commitments, thereby reducing real estate costs and enhancing operational agility. Increasing urbanization and the rise of the gig economy further fuel demand, as freelancers, startups, and mobile workforces seek accessible, community-oriented environments equipped with high-speed internet, meeting facilities, and wellness amenities.

Technological integrations, such as AI-driven booking systems and smart building features, improve user experiences and efficiency, attracting tech-savvy tenants. Government incentives for sustainable developments and corporate emphasis on employee retention through flexible arrangements also propel expansion, with operators innovating to meet evolving preferences for eco-friendly and health-focused workspaces.

Restraints

Restraints in the Flexible Office Market arise from economic uncertainties and fluctuating occupancy rates, as businesses hesitate to commit amid recessions or policy changes, leading to underutilized spaces and revenue instability for operators. High initial setup costs for premium amenities and technology integrations can strain smaller providers, limiting market entry in emerging regions. Regulatory challenges, including zoning laws and building codes varying by location, complicate expansions and increase compliance expenses. Moreover, competition from traditional offices and home-based setups persists, particularly in areas with poor infrastructure, while concerns over data privacy in shared environments deter sensitive industries like finance.

Opportunities

Opportunities in the Flexible Office Market are evident through expansions into suburban and secondary cities, where hybrid work drives demand for localized hubs reducing commute times and supporting work-life balance, enabled by partnerships with real estate developers for integrated mixed-use projects. Innovations in sustainable designs, incorporating green certifications and energy-efficient systems, attract eco-conscious tenants and qualify for incentives, opening avenues for premium pricing.

Collaborations with tech firms for VR-enhanced virtual offices and AI analytics can differentiate offerings, targeting global remote teams. The growing focus on wellness, with features like biophilic designs and mental health spaces, positions operators to capture health-oriented corporate clients, fostering long-term leases.

Challenges

Challenges in the Flexible Office Market involve maintaining consistent occupancy amid volatile demand, as economic shifts and return-to-office mandates can lead to sudden vacancies, requiring adaptive pricing and marketing strategies. Ensuring high-quality amenities and security in shared spaces demands ongoing investments, balancing cost control with user satisfaction to retain tenants. Supply chain disruptions for fit-outs and technology can delay openings, impacting revenue timelines. Additionally, differentiating in a saturated market requires unique value propositions, while addressing inclusivity for diverse user needs, such as accessibility and cultural adaptations, adds complexity in global expansions.

Flexible Office Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Flexible Office Market |

| Market Size 2025 | USD 47.02 Billion |

| Market Forecast 2035 | USD 229.91 Billion |

| Growth Rate | CAGR of 17.20% |

| Report Pages | 220 |

| Key Companies Covered |

WeWork Companies Inc., IWG PLC (Regus), UCOMMUNE, The Office Group, Spaces, SMARTWORKS, Industrious, KNOTEL, Kr Space, Serendipity Labs, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Market Segmentation Structured in the Flexible Office Market?

The Flexible Office market is segmented by type, application, end-user, and region.

Based on Type Segment, The most dominant segment is Private Offices, which holds the largest market share due to their provision of secure, customizable spaces for teams needing privacy while benefiting from shared amenities and short-term flexibility; this dominance drives the market by catering to enterprises transitioning from traditional leases, reducing costs, and enabling rapid scaling that supports overall industry growth. The second most dominant segment is Coworking Space, favored for its collaborative environment and networking opportunities; it contributes to market expansion by attracting startups and freelancers, fostering innovation ecosystems, and increasing accessibility in urban areas.

Based on Application Segment, The most dominant segment is IT and Communications, leading due to the sector’s agile nature requiring scalable, tech-equipped spaces for remote collaboration and innovation; this drives market growth by integrating advanced digital tools, attracting high-value tenants, and promoting hybrid models that accelerate adoption. The second most dominant segment is Media and Entertainment, driven by project-based work needing flexible setups; it propels expansion by supporting creative workflows, enabling cost-effective production hubs, and enhancing content creation efficiency.

Based on End-User Segment, The most dominant segment is Large Enterprises, commanding the majority share owing to their focus on cost optimization and workforce flexibility in global operations; this dominance fuels market growth by investing in premium spaces, driving operator revenues, and setting standards for hybrid integrations. The second most dominant segment is Small and Medium-Sized Enterprises, driven by affordable entry points; it aids growth by democratizing access to professional environments, supporting business scalability, and stimulating local economies.

What are the Recent Developments in the Flexible Office Market?

- In October 2025, The Instant Group reported a 164% surge in flexible space demand in U.S. towns under 5,000 population, driven by hybrid work, with operators like IWG expanding into suburban areas.

- In August 2025, Cushman & Wakefield’s Global Flexible Office Trends highlighted a 55% adoption rate among global occupiers, with meeting room bookings up 22% in the Americas, emphasizing collaboration-focused spaces.

- In December 2025, JLL’s Workplace Trends noted over 70% of firms enacting in-office policies, boosting flexible workspaces amid AI integration and return-to-office trends.

How Does Regional Analysis Impact the Flexible Office Market?

- North America to dominate the global market.

North America, valued at USD 19.35 billion in 2025 and projected to reach USD 94.45 billion by 2035 at a CAGR of 17.20%, dominates with over 41% revenue share due to its advanced technological ecosystem, high corporate density in tech and finance sectors, and widespread hybrid work adoption supported by robust infrastructure investments exceeding billions in urban redevelopment; Canada contributes through sustainable initiatives in cities like Toronto, but the United States as the dominating country leads with major hubs in New York and San Francisco, where companies like WeWork and Industrious drive innovation through AI-enhanced spaces and policy incentives for green buildings, fostering a mature market with high occupancy rates and premium pricing.

Europe demonstrates robust growth, propelled by EU sustainability mandates and urban revitalization projects allocating funds for flexible workspaces, with emphasis on wellness-integrated designs and cross-border collaborations enhancing accessibility; the United Kingdom stands as the dominating country with London’s vibrant ecosystem, supported by post-Brexit incentives for startups and media firms, leading to expansions by operators like IWG in mixed-use developments.

Asia Pacific is witnessing explosive expansion, fueled by rapid urbanization and gig economy booms in populous nations, with government subsidies for digital infrastructure boosting coworking in tech corridors; China dominates the region as the leading country, leveraging state-backed initiatives in Shanghai and Beijing for smart city integrations, attracting IT giants and achieving high growth through affordable, scalable models.

Latin America exhibits emerging momentum, driven by economic recovery and remote work trends in megacities, with international investments funding eco-friendly spaces; Brazil leads as the dominating country with Sao Paulo’s thriving startup scene, supported by fintech growth and flexible leasing reforms that enhance accessibility for SMEs.

The Middle East and Africa are progressively advancing, influenced by diversification from oil economies and tourism-driven developments, with pilot projects in smart cities; the United Arab Emirates dominates through Dubai’s ambitious visions, integrating flexible offices in free zones with incentives for global firms, promoting high-end, tech-savvy environments.

Who are the Key Market Players in the Flexible Office Market?

WeWork Companies Inc. WeWork Companies Inc. offers vibrant coworking spaces with community events, employing strategies like partnerships with corporations for customized enterprise solutions and investments in sustainable designs to attract eco-conscious tenants.

IWG PLC (Regus). IWG PLC (Regus) provides a global network of serviced offices, strategizing through franchise expansions and hybrid model integrations to serve remote workers with flexible memberships.

UCOMMUNE. UCOMMUNE focuses on tech-enabled spaces in Asia, with strategies involving AI analytics for occupancy optimization and collaborations with startups for innovation hubs.

The Office Group. The Office Group emphasizes design-led offices, employing strategies like wellness-focused amenities and acquisitions to broaden its premium portfolio in Europe.

Spaces. Spaces offers creative coworking environments, strategizing via parent company IWG’s resources for global scaling and digital booking platforms.

SMARTWORKS. SMARTWORKS targets Indian enterprises with managed offices, with strategies including tech integrations for smart access and cost-effective scaling.

Industrious. Industrious provides hospitality-inspired workspaces, strategizing through partnerships with landlords for revenue-sharing models and expansions in U.S. suburbs.

KNOTEL. KNOTEL specializes in flexible headquarters, employing strategies like data-driven site selections and custom fit-outs for mid-sized firms.

Kr Space. Kr Space focuses on Chinese markets with community-driven spaces, strategizing via ecosystem partnerships for startup support and rapid urban expansions.

Serendipity Labs. Serendipity Labs offers upscale coworking, with strategies emphasizing privacy and professional networking events to retain high-end clients.

What are the Market Trends in the Flexible Office Market?

- Surging demand for hybrid workspaces integrating remote and in-office elements for better work-life balance.

- Expansion into suburban and smaller towns driven by reduced commutes and cost savings.

- Integration of AI and smart technologies for occupancy management and personalized experiences.

- Focus on sustainability with green certifications and wellness amenities attracting tenants.

- Rise in revenue per desk through premium services and diversified offerings.

What Market Segments and their Subsegments are Covered in the Flexible Office Report?

By Type

-

- Coworking Space

- Private Offices

- Virtual Offices

- Serviced Offices

- Managed Offices

- Hot Desks

- Day Passes

- Meeting Rooms

- Collaborative Spaces

- Hybrid Spaces

- Others

By Application

-

- IT and Communications

- Media and Entertainment

- Retail

- Consumer Goods

- Real Estate

- Finance

- Healthcare

- Education

- Manufacturing

- Professional Services

- Others

By End-User

-

- Large Enterprises

- Small and Medium-Sized Enterprises

- Startups

- Freelancers

- Government

- Non-Profits

- Corporates

- Individuals

- Consultants

- Remote Workers

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Flexible Office Market - Industry Analysis

Chapter 4. Global Flexible Office Market- Competitive Landscape

Chapter 5. Global Flexible Office Market - Type Analysis

Chapter 6. Global Flexible Office Market - Application Analysis

Chapter 7. Global Flexible Office Market - End-User Analysis

Chapter 8. Flexible Office Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Flexible offices are adaptable workspaces offering short-term leases, shared amenities, and scalable options like coworking, private suites, or virtual setups, designed for hybrid work and cost efficiency.

Key factors include hybrid work adoption, urbanization, gig economy growth, technological integrations, and sustainability demands.

The market is projected to grow from USD 55.11 billion in 2026 to USD 229.91 billion by 2035.

The CAGR is expected to be 17.20% during 2026-2035.

North America will contribute notably, holding 41% share, driven by infrastructure in the United States.

Major players include WeWork Companies Inc., IWG PLC (Regus), UCOMMUNE, The Office Group, Spaces, and SMARTWORKS, among others.

The report offers insights on size, forecasts, segmentation, dynamics, regions, players, trends, and strategies.

The value chain includes site acquisition, design and fit-out, operations management, tenant acquisition, and maintenance services.

Trends emphasize sustainability and tech, with preferences for flexible, wellness-focused spaces.

Regulations on zoning and sustainability incentives drive eco-friendly designs, while environmental factors push green certifications.