Flexible Display Market Size, Share and Trends 2026 to 2035

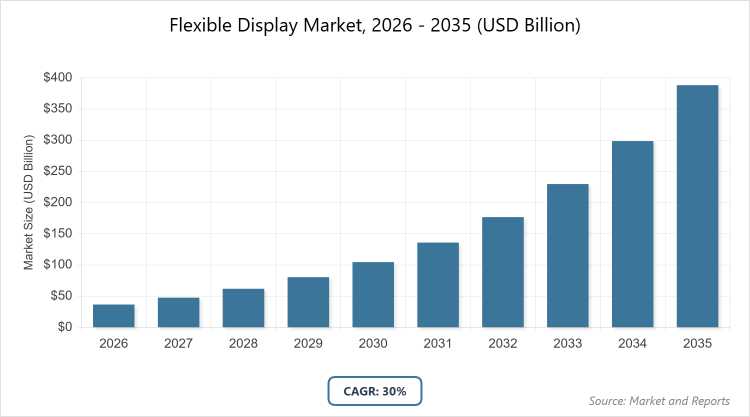

According to MarketnReports, the global Flexible Display market size was estimated at USD 36.6 billion in 2025 and is expected to reach USD 504.2 billion by 2035, growing at a CAGR of 30% from 2026 to 2035. Flexible Display Market is driven by increasing demand for innovative and portable consumer electronics.

What are the Key Insights into the Flexible Display Market?

- The global flexible display market size was valued at USD 36.6 billion in 2025 and is projected to reach USD 504.2 billion by 2035.

- The global flexible display market is expected to grow at a CAGR of 30% from 2026 to 2035.

- The global flexible display market is driven by rising adoption of foldable smartphones, wearables, and automotive displays.

- The OLED subsegment dominates the technology segment with a 47% share due to its superior image quality, energy efficiency, and flexibility enabling innovative device designs.

- The smartphones and tablets subsegment dominates the application segment with a 45% share as it benefits from consumer demand for portable, large-screen devices in compact forms.

- The consumer electronics subsegment dominates the end-use segment with a 64% share owing to widespread integration in everyday gadgets like phones and wearables.

- Asia Pacific dominates the global flexible display market with a 50% share attributed to robust manufacturing ecosystems in countries like South Korea and China.

What is the Flexible Display Market Overview?

The flexible display market encompasses technologies that enable screens to bend, fold, or roll without compromising functionality, revolutionizing device design across various industries. Flexible displays are defined as electronic visual interfaces built on pliable substrates like plastic or thin glass, allowing for curved, foldable, or rollable form factors that enhance portability, durability, and user experience in applications ranging from consumer gadgets to automotive interfaces. This market integrates advanced materials such as organic light-emitting diodes (OLED) and electronic paper displays (EPD), addressing the need for lightweight, energy-efficient alternatives to rigid screens while supporting emerging trends in wearable and foldable electronics.

What are the Market Dynamics in the Flexible Display Market?

Growth Drivers

The primary growth drivers in the flexible display market include advancements in OLED and micro-LED technologies, which enable higher resolution and durability in bendable screens, coupled with surging consumer demand for innovative devices like foldable smartphones and wearables. Increasing investments in research and development by key players are accelerating material innovations, such as flexible substrates and thin-film encapsulation, reducing production costs and expanding applications into automotive and healthcare sectors. Additionally, the push for energy-efficient and lightweight electronics aligns with global sustainability trends, further propelling market expansion through enhanced device portability and user-centric designs.

Restraints

High manufacturing costs and complex production processes pose significant restraints in the flexible display market, as achieving consistent yield rates for large-scale flexible panels remains challenging, leading to elevated prices that limit mass adoption. Technical limitations, including vulnerability to mechanical stress and shorter lifespan compared to rigid displays, hinder reliability in demanding applications like automotive dashboards. Moreover, supply chain disruptions for specialized materials such as polyimide substrates and encapsulation films exacerbate delays and increase dependency on a few dominant suppliers, constraining overall market growth.

Opportunities

Opportunities in the flexible display market are abundant with the rise of emerging applications in augmented reality (AR), virtual reality (VR), and Internet of Things (IoT) devices, where flexible screens can enable seamless integration into curved or irregular surfaces for immersive experiences. Expanding into automotive interiors for customizable dashboards and heads-up displays presents untapped potential, driven by the shift toward electric vehicles and smart mobility. Furthermore, advancements in roll-to-roll manufacturing and sustainable materials open avenues for cost reduction and eco-friendly innovations, attracting investments and fostering partnerships across industries.

Challenges

Challenges in the flexible display market stem from durability issues, as repeated bending can cause creases, delamination, or pixel degradation, necessitating ongoing improvements in protective coatings and hinge mechanisms. Intellectual property disputes and patent barriers among leading manufacturers slow innovation and increase litigation risks, particularly in competitive regions like Asia Pacific. Additionally, standardization of testing protocols for flexibility and longevity remains inconsistent, complicating quality assurance and consumer trust in new products.

Flexible Display Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Flexible Display Market |

| Market Size 2025 | USD 36.6 Billion |

| Market Forecast 2035 | USD 504.2 Billion |

| Growth Rate | CAGR of 30% |

| Report Pages | 220 |

| Key Companies Covered | Samsung Electronics Co., Ltd., LG Display Co., Ltd., BOE Technology Group Co., Ltd., Japan Display Inc., AU Optronics Corp., Sharp Corporation, Innolux Corporation, Visionox Company, Royole Corporation, Corning Incorporated, and Others |

| Segments Covered | By Technology, By Application, By End-Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Flexible Display Market Segmented?

The Flexible Display market is segmented by technology, application, end-use, and region.

Based on Technology Segment. The OLED subsegment is the most dominant in the technology segment, holding a 47% share, primarily because of its self-emissive properties that deliver vibrant colors, high contrast, and thin profiles ideal for foldable applications, driving market growth by enabling premium smartphones and wearables with superior visual performance. The LCD subsegment follows as the second most dominant, with a 25% share, offering cost-effective alternatives for mid-range devices while supporting market expansion through broader accessibility in tablets and automotive displays.

Based on Application Segment. The smartphones and tablets subsegment dominates the application segment with a 45% share, fueled by consumer preference for compact yet expansive screens that enhance multitasking and media consumption, propelling overall market growth via high-volume sales from brands like Samsung. The wearables subsegment is the second most dominant at 20%, providing lightweight, curved displays for fitness trackers and smartwatches, contributing to market momentum by addressing health monitoring trends and integrating seamlessly with daily lifestyles.

Based on End-Use Segment. The consumer electronics subsegment leads the end-use segment with a 64% share, driven by widespread adoption in personal devices where flexibility improves portability and user engagement, significantly boosting market growth through rapid innovation cycles. The automotive subsegment ranks second with a 15% share, utilizing flexible displays for intuitive dashboards and infotainment systems, aiding market development by aligning with the rise of connected and autonomous vehicles.

What are the Recent Developments in the Flexible Display Market?

- In May 2025, BOE began construction of an 8.6-Gen AMOLED line in Chengdu at USD 8.72 billion, enhancing premium flexible capacity and targeting increased production for foldable devices.

- In March 2025, Samsung Display secured a multi-year order for OLED MacBook Pro panels starting 2026, with initial annual volumes of 3-5 million units, expanding flexible display applications into laptops.

- In January 2025, Samsung confirmed an October 2025 launch for a tri-fold smartphone using 360-degree ultra-thin glass, pushing boundaries in multi-fold technology.

- In September 2024, Huawei launched a tri-foldable phone with a 10-inch main display and dual hinges, differentiating it from standard foldables and boosting interest in advanced flexible formats.

- In May 2024, Visionox Technology invested USD 7.6 billion in a new 8.6-generation AMOLED plant in Hefei, China, to strengthen production capabilities for flexible displays.

What is the Regional Analysis of the Flexible Display Market?

Asia Pacific to dominate the global market.

Asia Pacific leads the flexible display market with a 50% share, driven by robust manufacturing hubs in South Korea, where Samsung and LG dominate OLED production, and China, with BOE’s expansive facilities accelerating cost-effective scaling for global exports.

North America holds a significant position, supported by innovation in the U.S., where companies like Apple integrate flexible displays into premium devices, fostering growth through R&D investments and strong consumer demand for advanced electronics.

Europe exhibits steady expansion, led by Germany, which emphasizes high-end applications in automotive sectors, with firms like Mercedes-Benz adopting flexible dashboards to enhance vehicle interfaces amid regulatory pushes for sustainable tech.

Latin America is emerging gradually, with Brazil as the key country, benefiting from increasing smartphone penetration and partnerships with Asian manufacturers to localize production and meet rising demand for affordable foldables.

The Middle East and Africa show promising growth, dominated by the United Arab Emirates, where smart city initiatives incorporate flexible digital signage, driven by infrastructure investments and tourism-focused applications.

Who are the Key Market Players in the Flexible Display Market?

- Samsung Electronics Co., Ltd. focuses on vertical integration, securing patents for foldable hinges and ultra-thin glass, while expanding Gen-8.6 OLED fabs to maintain leadership in smartphones and wearables through aggressive R&D investments.

- LG Display Co., Ltd. emphasizes sustainable manufacturing and partnerships, such as supplying OLED panels for automotive dashboards, leveraging its expertise in large-format flexible displays to diversify beyond consumer electronics.

- BOE Technology Group Co., Ltd. pursues cost leadership via massive capacity expansions in China, targeting mid-tier markets with affordable flexible OLEDs and collaborating with global OEMs for automotive and IoT applications.

- Japan Display Inc. specializes in niche innovations like micro-LED integration for wearables, forming alliances with tech giants to enhance resolution and durability in compact devices.

- AU Optronics Corp. adopts a hybrid strategy, combining LCD and OLED technologies for cost-effective flexible solutions in tablets and digital signage, while investing in roll-to-roll processes for scalability.

- Sharp Corporation prioritizes high-brightness flexible displays for outdoor and automotive uses, utilizing its IGZO technology to improve energy efficiency and partner with vehicle manufacturers.

- Innolux Corporation focuses on modular designs, enabling customizable flexible panels for smart home appliances, and expands through acquisitions to strengthen supply chain resilience.

- Visionox Company invests in AMOLED R&D for foldables, aiming at emerging markets with price-competitive offerings and strategic joint ventures for technology transfer.

- Royole Corporation pioneers rollable displays, targeting premium niches like e-readers, with a strategy centered on intellectual property development and licensing agreements.

- Corning Incorporated concentrates on substrate materials like ultra-thin glass, collaborating with display makers to enhance durability and enable thinner, more flexible screens across applications.

What are the Market Trends in the Flexible Display Market?

- Advancements in OLED and micro-LED technologies for higher durability and resolution.

- Increasing adoption of foldable and rollable devices in consumer electronics.

- Expansion into automotive applications for curved dashboards and heads-up displays.

- Focus on sustainable materials and energy-efficient manufacturing processes.

- Integration with AR/VR for immersive, flexible interfaces.

- Growth in wearables driven by health monitoring trends.

- Rising investments in roll-to-roll production for cost reduction.

- Emergence of hybrid form factors combining flexible and rigid elements.

- Enhanced thin-film encapsulation to improve lifespan and reliability.

- Shift toward Asia Pacific for supply chain optimization and innovation.

What Market Segments and their Subsegments are Covered in the Flexible Display Report?

By Technology

- OLED

- LCD

- EPD

- LED

- Quantum Dot

- Micro-LED

- E-Paper

- Flexible OLED

- AMOLED

- PMOLED

- Others

By Application

- Smartphones and Tablets

- Wearables

- Televisions

- Automotive Displays

- Laptops and PCs

- Digital Signage

- E-Readers

- Smart Home Appliances

- Medical Devices

- Aerospace

- Others

By End-Use

- Consumer Electronics

- Automotive

- Healthcare

- Media and Entertainment

- Aerospace and Defense

- IT and Telecommunication

- Sports and Fashion

- Retail

- Education

- Transportation

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Flexible displays are electronic screens made from pliable materials that can bend, fold, or roll, offering innovative form factors for devices while maintaining high image quality and functionality.

Key factors include technological advancements in OLED, rising demand for foldables, expanding automotive applications, cost reductions in manufacturing, and integration with emerging tech like AR/VR.

The flexible display market is projected to grow from USD 45.3 billion in 2026 to USD 504.2 billion by 2035.

The flexible display market is expected to grow at a CAGR of 30% from 2026 to 2035.

Asia Pacific will contribute notably, driven by manufacturing prowess in South Korea and China.

Major players include Samsung Electronics Co., Ltd., LG Display Co., Ltd., BOE Technology Group Co., Ltd., Japan Display Inc., and AU Optronics Corp.

The report provides comprehensive analysis including size, trends, segmentation, regional insights, key players, and forecasts from 2026 to 2035.

Stages include raw material sourcing (substrates like plastic), component manufacturing (OLED layers), assembly into panels, integration into devices, and distribution to end-users.

Trends lean toward foldable and rollable designs, with consumers preferring lightweight, durable devices for portability and enhanced experiences in smartphones and wearables.

Regulations on e-waste and sustainability push for eco-friendly materials, while environmental concerns drive innovations in energy-efficient displays and recyclable substrates.