Electronic Toll Collection Market Size, Share and Trends 2026 to 2035

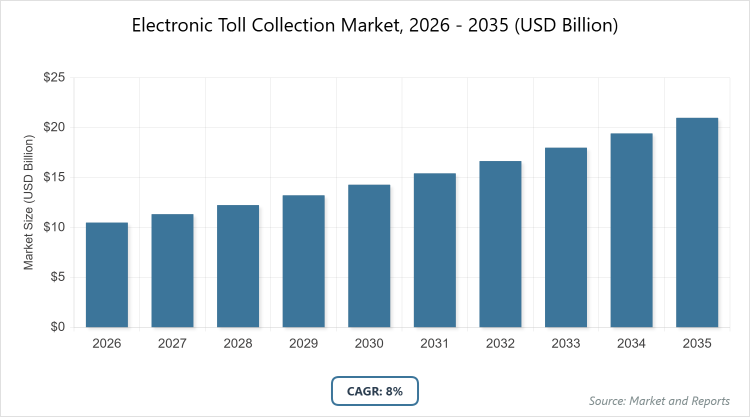

According to MarketnReports, the global Electronic Toll Collection Market size was estimated at USD 10.5 billion in 2025 and is expected to reach USD 25 billion by 2035, growing at a CAGR of 8% from 2026 to 2035. Electronic Toll Collection Market is driven by increasing government initiatives for smart transportation and reducing traffic congestion.What are the key insights into the Electronic Toll Collection Market?

- The global Electronic Toll Collection Market was valued at USD 10.5 billion in 2025 and is projected to reach USD 25 billion by 2035.

- The market is expected to grow at a CAGR of 8% during the forecast period from 2026 to 2035.

- The market is driven by rising urbanization, government mandates for efficient tolling, and advancements in contactless payment technologies.

- In the technology segment, RFID dominates with approximately 55% market share due to its cost-effectiveness, reliability, and widespread adoption in existing infrastructures.

- In the subsystem segment, automated vehicle identification holds about 40% share because of its critical role in real-time vehicle detection, enabling seamless toll transactions.

- In the application segment, highways lead with around 65% share owing to high traffic volumes and the need for uninterrupted flow on major roadways.

- North America dominates the regional market with approximately 40% share, attributed to advanced tolling infrastructure, regulatory support, and high adoption in the United States.

What is the industry overview of the Electronic Toll Collection Market?

The Electronic Toll Collection Market encompasses systems that enable automated, cashless toll payments on highways and bridges using technologies like RFID, DSRC, and GNSS to identify vehicles and deduct fees without stopping, thereby improving traffic flow and operational efficiency. Market definition refers to ETC as an integrated solution comprising hardware, software, and services for toll management, including transponders, readers, and back-office processing, aimed at minimizing congestion, enhancing revenue collection, and supporting smart city infrastructures. This market intersects with transportation and technology sectors, serving governments and private operators to modernize tolling while addressing environmental concerns through reduced emissions from idling vehicles.

What are the market dynamics of the Electronic Toll Collection Market?

Growth Drivers

The growth drivers of the Electronic Toll Collection Market are primarily fueled by escalating traffic congestion in urban areas and government initiatives worldwide, such as India's FASTag mandate and the U.S. Interstate Tolling Equity Act, which promote seamless, cashless systems to reduce delays and emissions. Technological integrations like GNSS for satellite-based tolling and AI for predictive analytics enhance accuracy and scalability, attracting investments in smart highways. Rising fuel efficiency demands and partnerships between tech firms and toll operators further propel adoption, as ETC systems cut operational costs by up to 50% through automated processing, driving expansion in emerging economies with burgeoning infrastructure projects.

Restraints

Restraints in the Electronic Toll Collection Market include high initial installation costs for infrastructure like gantries and back-end systems, which can exceed millions per kilometer, deterring deployment in budget-constrained regions. Interoperability issues between different ETC technologies and legacy systems lead to fragmented networks, complicating cross-border travel and increasing maintenance expenses. Privacy concerns over vehicle tracking and data security also hinder consumer acceptance, while regulatory variations across countries add compliance burdens, slowing market penetration in less developed areas.

Opportunities

Opportunities in the Electronic Toll Collection Market emerge from the rise of smart cities and connected vehicles, enabling integrations with IoT for dynamic pricing and congestion management, particularly in Asia Pacific through initiatives like China's Belt and Road infrastructure. Expansion into multi-lane free-flow systems and video-based tolling offers growth in urban applications, while collaborations with fintech for mobile payments open new revenue streams. Emerging markets in Latin America and Africa present untapped potential via public-private partnerships, supported by global funding for sustainable transport, fostering innovation in low-cost, scalable solutions.

Challenges

Challenges in the Electronic Toll Collection Market involve cybersecurity threats, as interconnected systems are vulnerable to hacking, potentially disrupting toll operations and eroding trust, necessitating robust encryption investments. Achieving nationwide interoperability remains difficult due to diverse standards, as seen in Europe's fragmented toll networks, requiring harmonization efforts. High dependency on power and network reliability in remote areas poses operational risks, while educating users on ETC benefits in low-adoption regions adds to implementation hurdles, impacting overall market maturity.

Electronic Toll Collection Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Electronic Toll Collection Market |

| Market Size 2025 | USD 10.5 Billion |

| Market Forecast 2035 | USD 25 Billion |

| Growth Rate | CAGR of 8% |

| Report Pages | 220 |

| Key Companies Covered |

Kapsch TrafficCom AG, Conduent Incorporated, TransCore, Thales Group, EFKON GmbH, and Others. |

| Segments Covered | By Technology, By Subsystem, By Application, and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Electronic Toll Collection Market segmented?

The Electronic Toll Collection Market is segmented by technology, subsystem, application, and region.By Technology Segment, RFID is the most dominant, holding about 55% market share, followed by DSRC as the second most dominant with around 25%. RFID's dominance arises from its affordability, ease of deployment, and compatibility with existing transponders, driving the market by facilitating quick upgrades in high-traffic areas and ensuring efficient revenue collection; DSRC contributes by offering secure, short-range communications for precise tolling, enhancing growth in advanced infrastructures.

By Subsystem Segment, automated vehicle identification is the most dominant with approximately 40% share, while violation enforcement system is the second most dominant at about 30%. Automated vehicle identification leads due to its foundational role in detecting and classifying vehicles in real-time, driving market expansion by minimizing errors and supporting scalable toll networks; violation enforcement systems aid growth by ensuring compliance through automated fines, reducing revenue leakage.

By Application Segment, highways are the most dominant with around 65% share, followed by urban areas as the second most dominant at roughly 35%. Highways' prevalence stems from the need for high-speed, non-stop tolling on long-distance routes, boosting market growth through improved traffic management; urban areas support expansion by addressing congestion in cities with compact systems.

What are the recent developments in the Electronic Toll Collection Market?

- In January 2025, TransCore introduced next-generation tolling technology on the West Virginia Turnpike, featuring enhanced RFID and AI integration for improved accuracy and reduced congestion.

- In September 2024, EFKON announced a collaboration to integrate AI-driven analytics into its automated toll systems, aiming to optimize traffic flow and predictive maintenance.

- In July 2025, Kapsch TrafficCom launched an interoperable ETC solution in Europe, complying with new EU directives for cross-border tolling.

- In March 2025, Conduent expanded its video-based tolling services in North America, incorporating machine learning for better vehicle classification.

What is the regional analysis of the Electronic Toll Collection Market?

North America to dominate the global market.North America leads the Electronic Toll Collection Market, driven by extensive highway networks and regulatory frameworks like the FAST Act, with the United States as the dominating country due to widespread E-ZPass adoption and investments in smart infrastructure, generating significant revenue from reduced emissions and efficient tolling.

Europe exhibits strong growth through interoperability initiatives like the European Electronic Toll Service, led by Germany with its advanced DSRC systems and focus on sustainable transport, supporting cross-border mobility.

Asia Pacific shows rapid expansion fueled by urbanization and government projects like India's FASTag, dominated by China through massive infrastructure developments and GNSS integrations for nationwide coverage.

Latin America presents emerging opportunities from toll road privatizations, with Brazil dominating due to its extensive concession networks and adoption of RFID for urban tolling.

The Middle East and Africa offer growth amid smart city investments, led by the United Arab Emirates with luxury highway projects, while South Africa contributes via GNSS-based systems for regional connectivity.

Who are the key market players in the Electronic Toll Collection Market?

Kapsch TrafficCom AG focuses on interoperable solutions and R&D in GNSS technology, partnering with governments for large-scale deployments to expand in Europe and Asia Pacific.

Conduent Incorporated employs strategies of digital transformation and AI integrations, leveraging acquisitions to enhance back-office processing and capture North American markets.

TransCore prioritizes violation enforcement and vehicle classification innovations, collaborating with U.S. agencies for efficient, scalable systems.

Thales Group adopts a focus on secure communications and smart city integrations, investing in DSRC to drive growth in defense-linked toll projects.

EFKON GmbH concentrates on AI analytics and sustainable tolling, utilizing partnerships for video-based systems in emerging regions.

What are the market trends in the Electronic Toll Collection Market?

- Shift toward cashless and contactless payments integrating with mobile wallets.

- Adoption of GNSS-based tolling for flexible, infrastructure-light solutions.

- Integration with smart city ecosystems for dynamic pricing and congestion management.

- Emphasis on interoperability standards for cross-border and multi-vendor systems.

- Rise in AI and machine learning for predictive analytics and fraud detection.

- Focus on sustainable practices reducing emissions through efficient traffic flow.

What market segments and their subsegments are covered in the Electronic Toll Collection Market report?

By Technology

- RFID

- DSRC

- GNSS/GPS

- Video Analytics

- Others

By Subsystem

- Automated Vehicle Identification

- Automated Vehicle Classification

- Violation Enforcement System

- Transaction Processing

By Application

- Highways

- Urban Areas

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

The Electronic Toll Collection Market involves automated systems for cashless toll payments using technologies like RFID and GNSS to enhance traffic efficiency.

Key factors include government infrastructure initiatives, technological advancements in AI, and rising urbanization demands.

The market is projected to grow from USD 10.5 billion in 2026 to USD 25 billion by 2035.

The CAGR is expected to be 8%.

North America will contribute notably, driven by advanced systems in the United States.

Major players include Kapsch TrafficCom AG, Conduent Incorporated, TransCore, Thales Group, and EFKON GmbH.

The report offers in-depth analysis of size, trends, segments, regions, players, and forecasts.

Stages include component manufacturing, system integration, deployment, operations, and maintenance.

Trends evolve toward contactless solutions, with consumers preferring seamless, app-integrated payments.

Factors include mandates for emission reductions and interoperability standards promoting green transport.