E-Learning Market Size, Share and Trends 2026 to 2035

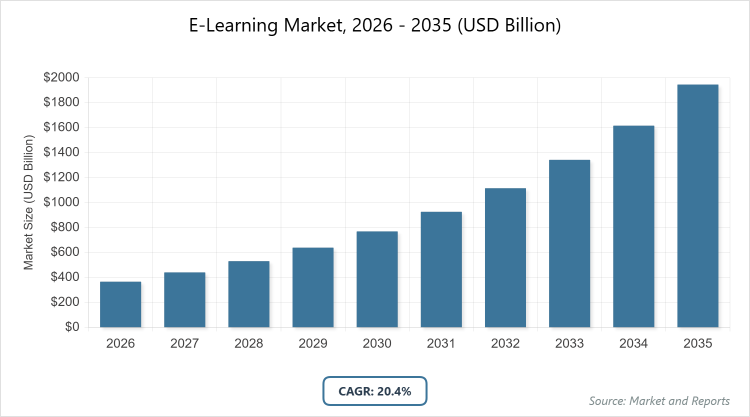

According to our latest research, the global e-learning market is valued at approximately USD 366 billion in 2025 and is projected to reach USD 2,335 billion by 2036, growing at a CAGR of 20.4% from 2026 to 2035. The E-Learning Market is primarily driven by the massive adoption of AI-driven personalization and the increasing demand for continuous workforce upskilling, which enable flexible, cost-effective, and scalable learning solutions across both academic and corporate sectors.

Industry Overview

The e-learning market encompasses the digital delivery of educational and training content through online platforms, mobile applications, and virtual classrooms, enabling learners to access materials anytime and anywhere without the constraints of traditional physical settings. It includes a wide array of solutions such as learning management systems (LMS), interactive courses, video lectures, simulations, and assessment tools designed for diverse audiences ranging from students in academic institutions to professionals seeking skill enhancement in corporate environments. This market integrates technologies like artificial intelligence, virtual reality, and cloud computing to provide personalized, scalable, and cost-effective learning experiences that cater to the evolving needs of a global workforce and education sector, fostering lifelong learning and bridging geographical barriers in knowledge dissemination.

Key Insights

- The global e-learning market is valued at approximately USD 366 billion in 2024 and is projected to reach USD 2,335 billion by 2034.

- The market is expected to grow at a compound annual growth rate (CAGR) of 20.4% from 2025 to 2034.

- Among deployment models, the cloud segment dominates due to its flexibility and cost-effectiveness.

- In course types, primary and secondary education is the leading subsegment, driven by post-pandemic digital adoption in K-12.

- By end-user, the corporate segment holds the largest share, fueled by workforce training needs.

- North America is the dominated region, supported by advanced infrastructure and high adoption rates.

E-Learning Market Dynamics

Growth Drivers

The e-learning market is propelled by the rapid adoption of advanced technologies such as artificial intelligence, augmented reality, and virtual reality, which enable personalized and immersive learning experiences that enhance engagement and retention rates among users. Increasing internet penetration and smartphone usage worldwide have made education more accessible, particularly in remote areas, while the shift toward remote and hybrid work models post-pandemic has heightened the demand for flexible training solutions in corporate sectors.

Government initiatives promoting digital education infrastructure, coupled with rising investments in employee upskilling to address skill gaps in evolving job markets, further accelerate growth by making e-learning a vital tool for continuous professional development and academic advancement.

Restraints

Despite its potential, the e-learning market faces significant hurdles including digital fatigue from prolonged screen time and the lack of personal interaction, which can lead to higher dropout rates and reduced motivation among learners compared to traditional classroom settings. Quality control issues, such as ensuring consistent educational standards and preventing cheating in online assessments, pose challenges, while budget constraints for small and medium enterprises limit investments in high-quality platforms. Additionally, the high operational costs associated with developing advanced content and maintaining technological infrastructure can restrain market expansion, particularly in regions with economic instability or limited funding for digital initiatives.

Opportunities

The integration of generative AI and immersive technologies like AR and VR presents lucrative opportunities for the e-learning market by allowing the creation of adaptive, interactive content that simulates real-world scenarios, thereby improving learning outcomes in high-stakes fields such as healthcare and manufacturing. Expanding partnerships between educational institutions and tech companies can tap into emerging markets, while the growing demand for microlearning and mobile-first solutions opens avenues for innovative, bite-sized content delivery that caters to busy professionals. Furthermore, government-led digital transformation initiatives in developing regions offer potential for scalable platforms that address educational inequities and support lifelong learning at premium pricing models.

Challenges

Key challenges in the e-learning market include bridging the digital divide in underdeveloped regions where limited access to stable internet, devices, and electricity hinders widespread adoption, exacerbating inequalities in education access. Ensuring learner engagement and completion rates remain difficult without face-to-face interactions, while concerns over data privacy and cybersecurity in online platforms add layers of complexity for providers. Regulatory variations across countries regarding online education accreditation and the need for continuous updates to keep content relevant amid rapid technological changes also pose ongoing obstacles that require strategic investments and adaptive strategies from market players.

E-Learning Market: Report Scope

| Report Attributes | Report Details |

| Report Name | E-Learning Market |

| Market Size 2025 | USD 366 Billion |

| Market Forecast 2035 | USD 2,335 Billion |

| Growth Rate | CAGR of 20.4% |

| Report Pages | 220 |

| Key Companies Covered | Adobe, Inc., Coursera, Udemy, Inc, Blackboard Inc, Microsoft Corporation, Oracle Corporation, D2L Corporation, Skillsoft, Infosys, Accenture |

| Segments Covered | By Provider, By Deployment Model, By Course Type, By End-User By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

E-Learning Market – Segmentation

The simulation software market is segmented by provider, deployment model, course type, end-user, and region, each delineating adoption patterns and growth levers that inform competitive maneuvers and investment foci.

By provider, The provider segmentation in the e-learning market is divided into content providers and service providers, with content providers emerging as the most dominant due to their role in creating high-quality, engaging educational materials that form the core of digital learning experiences, driving market growth through scalable, customizable content that meets diverse learner needs and enables platforms to differentiate themselves in a competitive landscape. Service providers rank as the second most dominant, offering essential support like platform integration and maintenance, which helps sustain long-term user engagement and operational efficiency, although they trail content providers because the latter directly influences learner satisfaction and retention, thereby accelerating overall market expansion through innovative content delivery.

By Deployment Model, In deployment models, cloud-based solutions dominate the e-learning market owing to their scalability, accessibility, and lower upfront costs, allowing seamless updates and remote access that cater to the growing demand for flexible learning in both academic and corporate settings, thus propelling market growth by reducing barriers to entry for users worldwide. On-premise deployments are the second most dominant, preferred by organizations requiring high data security and customization, such as government entities, but they lag behind cloud options because the latter’s cost-effectiveness and ease of integration better align with the rapid shift toward digital transformation, enhancing market dynamics through broader adoption.

By Course Type, the course type segmentation sees primary and secondary education as the most dominant subsegment, attributed to the widespread integration of digital tools in K-12 curricula post-COVID, which drives market growth by making education more interactive and accessible for young learners, supported by government funding and parental demand for supplemental online resources. Higher education follows as the second most dominant, benefiting from universities adopting low-cost, advanced methodologies that boost productivity and global reach, though it is secondary because primary education’s foundational role and higher volume of users provide a stronger impetus for market expansion through early digital literacy initiatives.

By End-User, Among end-users, the corporate segment is the most dominant in the e-learning market, driven by substantial investments in employee training to address skill gaps in technologies like AI and automation, which fuels growth by enhancing workforce productivity and competitiveness in a dynamic job market. The academic segment is the second most dominant, encompassing schools and universities that leverage e-learning for curriculum delivery, but it trails corporate due to the latter’s higher spending power and urgent need for continuous upskilling, thereby significantly contributing to market advancement through scalable training solutions.

Recent Developments

- In April 2025, the Punjab and Haryana High Court in India ruled that qualifications obtained through remote distance learning from deemed universities, private institutions, and state universities are valid, provided they are verified by government departments or the University Grants Commission, which is expected to boost confidence in online education and expand market accessibility in the region.

- In September 2025, Coursera introduced Skill Tracks, a data-driven learning solution that maps skills from foundational to expert levels using labor market insights and competency frameworks, enhancing personalized professional development and driving user engagement on the platform.

- In May 2025, Udemy launched Role Play, an AI-powered tool for soft skills development through realistic simulations, addressing the growing need for interactive training in corporate environments and contributing to higher retention rates.

- In July 2024, the Apparel Made-ups Home Furnishing Sector Skill Council (AMHSSC) partnered with Bluesign Technologies AG to introduce the “Foundation to Apparel Sustainability” e-learning course, focusing on sustainable practices in India’s apparel industry, including circular economy principles and recycling, thereby promoting sector-specific skill enhancement.

- In March 2025, Infosys unveiled the Infosys Springboard Makerlab at Symbiosis International University, providing hands-on STEM experiences to improve student employability, reflecting the trend toward collaborative educational initiatives.

- In July 2023, College Vidya released an AI-powered tool to help students choose suitable online universities, streamlining decision-making and increasing enrollment in digital programs.

- In August 2023, Edmingle collaborated with McGraw Hill to offer resources for students preparing for national competitive exams in India, fostering digital innovation and expanding access to quality preparatory content.

E-Learning Market – Regional Analysis

- North America To Dominate The Global Market

North America dominates the e-learning market with a significant share, primarily driven by advanced technological infrastructure, high internet penetration, and the presence of leading edtech companies and universities that invest heavily in digital learning tools; the United States is the dominating country, accounting for the majority of regional revenue through innovations in corporate training and online higher education, supported by substantial funding and a culture of lifelong learning that accelerates adoption rates and market growth.

Europe exhibits remarkable growth in the e-learning market due to well-established education systems, government funding for digital initiatives, and private sector involvement in vocational training; Germany and the United Kingdom are dominating countries, with Germany leading in corporate upskilling programs amid its strong industrial base and the UK excelling in academic platforms, together fostering a robust ecosystem that enhances accessibility and personalization through EU-wide policies on skill development.

Asia Pacific holds the largest revenue share and the highest growth potential in the e-learning market, fueled by rapid digital infrastructure development, increasing smart device users, and government initiatives for distance education; China and India are the dominating countries, with China leading through massive public-private investments in K-12 and higher education platforms, while India contributes via affordable mobile learning solutions and partnerships that address a vast young population’s educational needs, driving exponential market expansion.

Latin America is emerging in the e-learning market with growing internet and smartphone penetration supported by government efforts to improve educational access; Brazil dominates the region, leveraging its large population and initiatives like digital inclusion programs to expand online learning in both academic and corporate sectors, though challenges like infrastructure gaps persist, the focus on remote education helps bridge socioeconomic divides and stimulates steady growth.

The Middle East & Africa region is witnessing gradual e-learning market growth driven by increasing digital adoption and government investments in education technology; Saudi Arabia and the United Arab Emirates are dominating countries, with Saudi Arabia leading through Vision 2030 initiatives that promote online training for workforce development, and the UAE excelling in innovative platforms for higher education, collectively advancing the market by addressing skill shortages in key sectors like oil and tourism despite connectivity hurdles.

Key Market Players and Strategies

- Adobe, Inc.: Adobe focuses on strategies like product innovation through tools such as Captivate for interactive content creation, partnerships with educational institutions for seamless integration, and acquisitions to expand its ecosystem, aiming to enhance user engagement and dominate in content development.

- Coursera: Coursera’s strategies include collaborations with top universities for credentialed courses, AI-driven personalization for learner recommendations, and expansions into enterprise training, driving growth by offering accessible, high-quality education that boosts completion rates and market penetration.

- Udemy, Inc.: Udemy employs a marketplace model with user-generated content, frequent promotions to attract learners, and AI tools like Role Play for skill simulations, focusing on affordability and variety to capture the professional development segment and foster organic growth.

- Blackboard Inc.: Blackboard’s strategies revolve around LMS enhancements for hybrid learning, integrations with third-party tools, and acquisitions for analytics capabilities, targeting academic institutions to improve administrative efficiency and student outcomes.

- Microsoft Corporation: Microsoft leverages its Azure cloud for scalable platforms, integrations with Teams for virtual classrooms, and partnerships with governments for digital education initiatives, emphasizing accessibility and security to lead in the corporate and academic sectors.

- Oracle Corporation: Oracle focuses on cloud-based HCM solutions with embedded learning modules, AI for adaptive paths, and global expansions through acquisitions, aiming to streamline enterprise training and compliance.

- D2L Corporation: D2L’s Brightspace platform strategies include user-centric design for engagement, integrations with AR/VR, and collaborations with K-12 providers, prioritizing personalization to gain traction in academic markets.

- Skillsoft: Skillsoft pursues content library expansions via acquisitions, AI-powered skill assessments, and enterprise-focused subscriptions, targeting reskilling needs to enhance workforce productivity.

- Infosys: Infosys strategies involve launching initiatives like Springboard for STEM education, partnerships with universities, and AI integrations for customized training, focusing on emerging markets like India for rapid expansion.

- Accenture: Accenture emphasizes generative AI programs with Stanford collaborations, on-demand learning platforms, and consulting services for digital transformation, driving corporate adoption through tailored solutions.

Market Trends

- Integration of AI and machine learning for personalized learning paths and automated grading, enhancing user engagement and outcomes.

- Rise of mobile-first and microlearning modules for flexible, bite-sized content accessible on smartphones.

- Adoption of VR and AR for immersive simulations in high-risk training sectors like healthcare and manufacturing.

- Shift toward hybrid learning models combining online and in-person elements post-pandemic.

- Growing emphasis on generative AI for content creation, translation, and adaptive assessments to reduce costs.

- Expansion of cloud deployment for anytime-anywhere access and cost efficiency.

- Increased focus on soft skills development through role-playing and interactive platforms.

- Surge in government partnerships for digital education infrastructure in developing regions.

- Emphasis on data privacy and cybersecurity in online platforms amid rising regulations.

- Trend toward skill-based credentials and certifications over traditional degrees for career advancement.

Market Segments Covered in the Report

By Provider

- Content Providers

- Service Providers

By Deployment Model

- Cloud

- On-premise

By Course Type

- Primary and Secondary Education

- Higher Education

- Online Certification and Professional Courses

- Test Preparation

By End-User

- Academic

- Corporate

- Government

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global E-Learning Market - Industry Analysis

Chapter 4. Global E-Learning Market- Competitive Landscape

Chapter 5. Global E-Learning Market - Provider Analysis

Chapter 6. Global E-Learning Market Market - Deployment Model Analysis

Chapter 7. Global E-Learning Market Market - Course Type Analysis

Chapter 8. Global E-Learning Market Market - End-User Analysis

Chapter 15. E-Learning Market Market - Regional Analysis

Chapter 16. Company Profiles

Frequently Asked Questions

The e-learning market refers to the industry involved in the digital provision of educational and training services through online platforms, encompassing tools like LMS, virtual classrooms, and mobile apps for accessible, flexible learning across academic, corporate, and government sectors.

Key factors include technological advancements in AI, VR, and AR for personalized experiences, increasing internet and smartphone penetration, government initiatives for digital education, workforce upskilling demands, and the shift to hybrid work models, while challenges like digital divide and quality control may temper growth.

The e-learning market is projected to grow from approximately USD 441 billion in 2026 to USD 2,335 billion by 2035, reflecting substantial expansion driven by global digital adoption.

The compound annual growth rate (CAGR) for the e-learning market is expected to be 20.4% from 2026 to 2035.

North America will contribute notably, holding the largest market share due to its advanced infrastructure, high adoption rates, and significant investments in edtech, with the United States as the key driver.

Major players include Adobe, Inc., Coursera, Udemy, Inc., Blackboard Inc., Microsoft Corporation, Oracle Corporation, D2L Corporation, Skillsoft, Infosys, and Accenture, which drive growth through innovations, partnerships, and AI integrations.

The global e-learning market report provides comprehensive insights into market size, growth forecasts, segmentation analysis, drivers, restraints, opportunities, regional trends, key players, recent developments, and future outlook to guide stakeholders in strategic decision-making.

The value chain includes content creation and development, platform and technology provision (like LMS and cloud services), distribution through online channels, end-user delivery and support, and ongoing assessment and updates for continuous improvement.

Market trends are shifting toward AI-driven personalization, mobile microlearning, and immersive VR/AR experiences, while consumer preferences favor flexible, skill-focused content that offers quick certifications and real-world applicability over traditional long-form education.

Regulatory factors include accreditation standards for online qualifications and data privacy laws like GDPR, which ensure quality and security but may increase compliance costs; environmental factors involve the push for sustainable digital practices, such as energy-efficient cloud computing, amid growing awareness of tech's carbon footprint.