E-KYC Market Size, Share, and Trends 2026 to 2035

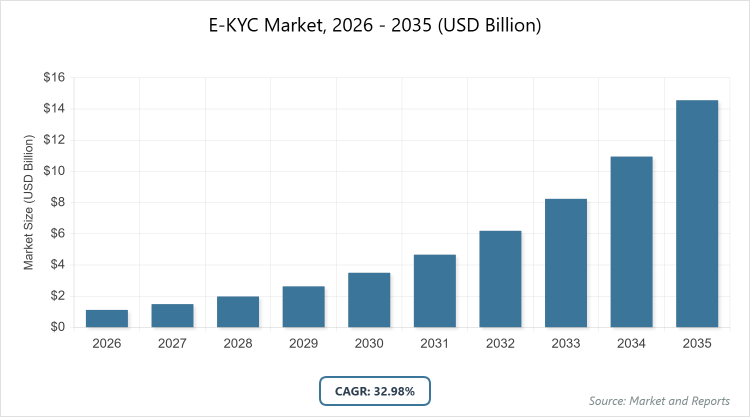

The global E-KYC market size was estimated at USD 1.12 billion in 2025 and is expected to reach USD 13.28 billion by 2035, growing at a CAGR of 32.98% from 2026 to 2035. The E-KYC market is primarily driven by the increasing global demand for digital identity verification to prevent fraud and ensure regulatory compliance in financial services.

What Are the Key Insights from the E-KYC Market?

- The global E-KYC market is projected to grow from USD 1.10 billion in 2026 to USD 13.23 billion by 2035, at a CAGR of 31.86%.

- Dominated Subsegment in Product: Identity Authentication & Matching holds the largest share due to its essential function in compliance-driven verifications.

- Dominated Subsegment in Deployment Mode: Cloud-Based deployment dominates owing to its scalability and cost advantages.

- Dominated Subsegment in End-Use: Banking, Financial Services, and Insurance (BFSI) leads with widespread regulatory mandates.

- Dominated Region: North America contributes the highest value, accounting for over 40% of the global market.

What Defines the E-KYC Market?

Industry Overview

The E-KYC market involves digital technologies and processes that enable remote verification of customer identities to meet regulatory requirements such as Know Your Customer (KYC) and Anti-Money Laundering (AML) standards. It incorporates tools like biometric authentication, AI-based facial recognition, video verification, document scanning, and real-time database checks to facilitate secure, efficient onboarding in industries including banking, telecommunications, insurance, government services, and e-commerce.

By eliminating the need for physical presence or paper documents, E-KYC enhances operational efficiency, reduces fraud, lowers costs, and promotes financial inclusion, particularly in digital-first economies where rapid customer acquisition is crucial. As cyber threats evolve and global regulations tighten, E-KYC plays a pivotal role in balancing compliance with user experience in an interconnected digital landscape.

What Drives the Growth of the E-KYC Market?

Growth Drivers

The E-KYC market is driven by the rapid expansion of digital financial services, increasing regulatory pressures for AML and KYC compliance worldwide, and the growing prevalence of identity theft and cyber fraud that demand advanced verification mechanisms. Innovations in AI, machine learning, and biometrics allow for quicker and more reliable identity checks, while the surge in mobile and internet usage in developing regions enables broader access to remote services. The post-pandemic emphasis on contactless interactions, along with government initiatives for digital identities, further fuels adoption across fintech, telecom, and other sectors, leading to cost efficiencies and improved customer satisfaction.

Restraints

Restraints include stringent data privacy regulations varying by region, which increase compliance burdens and operational complexities for providers. Issues like unreliable internet in remote areas, integration challenges with outdated systems, and the potential for AI errors or biases in verification processes undermine confidence. Additionally, high implementation costs for cutting-edge technologies and concerns over data security breaches, especially with rising deepfake threats, limit market penetration among smaller organizations.

Opportunities

Opportunities lie in leveraging blockchain for decentralized and reusable digital identities, expanding into untapped markets in Asia and Africa through mobile-first solutions, and integrating E-KYC with emerging tech like 5G for instantaneous verifications. Collaborations between tech firms and regulators to standardize global frameworks, along with applications in non-traditional sectors such as healthcare and online gaming, could unlock new revenue streams and enhance inclusivity for unbanked populations.

Challenges

Challenges encompass adapting to frequently changing privacy laws, ensuring equitable access for individuals without digital footprints, and combating advanced fraud techniques like synthetic identities. The need for substantial investments in skilled talent and infrastructure, coupled with achieving seamless interoperability across borders, poses ongoing obstacles to scalable growth.

E-KYC Market: Report Scope

| Report Attributes | Report Details |

| Report Name | E-KYC Market |

| Market Size 2025 | USD 1.12 Billion |

| Market Forecast 2035 | USD 13.28 Billion |

| Growth Rate | CAGR of 32.98% |

| Report Pages | 195 |

| Key Companies Covered | Jumio Corporation, Trulioo, Onfido (Entrust IDV), Sumsub, Veriff, GB Group plc, and IDnow GmbH |

| Segments Covered | By Product, By Deployment Mode, By End-Use, By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the E-KYC Market Segmented?

The E-KYC market is segmented by product, deployment mode, end-use, and region.

By product, where Identity Authentication & Matching is the most dominant subsegment, followed by Video Verification as the second most dominant; Identity Authentication & Matching dominates as it provides the core infrastructure for cross-referencing customer data with authoritative sources like government databases, ensuring high accuracy in meeting AML/KYC requirements for high-stakes industries, which propels overall market growth by minimizing risks and enabling swift, scalable digital transformations.

By deployment mode, Cloud-Based is the most dominant subsegment, with On-Premise as the second most dominant; Cloud-Based leads because of its ability to offer real-time updates, reduced capital expenditure, and global accessibility, allowing businesses to adapt quickly to regulatory changes and integrate with diverse systems, thereby driving market expansion through enhanced agility and affordability for a broad range of enterprises.

By end-use, Banking, Financial Services, and Insurance (BFSI) is the most dominant subsegment, followed by Telecom as the second most dominant; BFSI dominates due to intense regulatory scrutiny and the need for secure handling of vast customer data volumes, fostering market growth by integrating E-KYC to streamline operations, combat fraud, and support innovative services like digital wallets that attract more users.

What Are the Recent Developments in the E-KYC Market?

- In early 2026, regulatory bodies in the EU advanced guidelines under eIDAS 2.0 to promote interoperable digital wallets, encouraging financial institutions to adopt AI-enhanced E-KYC for cross-border compliance and reducing verification times significantly.

- India expanded its Aadhaar-based E-KYC framework in January 2026, integrating blockchain elements to enhance security for fintech and telecom sectors, aiming to include more rural users and boost financial inclusion metrics.

- Major providers like Jumio introduced perpetual KYC monitoring tools in late 2025, rolling out in 2026 with AI-driven continuous risk assessments, addressing evolving fraud landscapes in North American banking.

Which Regions Lead the E-KYC Market?

- North America to dominate the market

North America dominates the E-KYC market with over 40% share, driven by stringent AML/KYC regulations from bodies like FinCEN, advanced technological infrastructure, high digital banking adoption, and substantial investments in AI and biometrics; the United States leads the region through its innovation ecosystem in Silicon Valley, collaborations between tech giants and financial institutions, and responses to identity fraud costing billions annually, with market growth supported by regulatory expansions such as FinCEN’s 2026 rules for investment advisers, e-commerce surges, and focus on perpetual KYC and liveness detection, though challenges like privacy laws (CCPA) and legacy system integration costs exist, the region’s mature fintech landscape and R&D emphasis ensure continued leadership in secure verification solutions.

Asia-Pacific is the fastest-growing region at a CAGR exceeding 24%, fueled by rapid digitalization, government-led initiatives like India’s Aadhaar and China’s digital IDs, booming fintech ecosystems, and massive mobile penetration; India dominates due to its population scale, Digital India and UPI programs reducing onboarding costs dramatically, widespread adoption in banking and telecom for financial inclusion, and high growth potential amid rising cyber threats, while countries like Indonesia and Southeast Asia contribute through smartphone proliferation and e-commerce expansion, despite hurdles in rural connectivity and varying privacy standards, opportunities in 5G and blockchain integrations position the region for significant future gains.

Europe holds approximately 20-25% of the market, emphasizing privacy-compliant solutions under GDPR and eIDAS 2.0 frameworks promoting interoperable digital wallets; the United Kingdom and Germany lead through strong fintech hubs in London and Berlin, post-Brexit regulatory flexibility in the UK, and harmonized standards facilitating cross-border banking and insurance verifications, projecting steady growth with a focus on explainable AI and sustainable practices to build trust, although regulatory fragmentation and compliance costs challenge smaller players, trends in biometric enhancements and open banking drive resilience and innovation.

Latin America accounts for 5-7% share, emerging with fintech growth and initiatives to reduce unbanked populations in Brazil and Mexico; Brazil dominates via Pix payment integrations and Central Bank support for E-KYC, enabling secure e-commerce and remittances amid digital transaction booms, with regional CAGR around 25% supported by mobile solutions addressing inclusion barriers, though economic instability and inconsistent regulations slow progress, partnerships for advanced verification could accelerate adoption in underserved markets.

The Middle East & Africa represents about 11%, advancing through digital transformation in the UAE, Saudi Arabia, and South Africa; the United Arab Emirates leads with UAE Pass and blockchain in smart cities, supporting verifications in finance and tourism under AML frameworks, with growth at 22% CAGR fueled by financial inclusion and investments in AI compliance, despite varying adoption rates and connectivity issues in Africa, regional partnerships enhance fraud security and economic diversification.

Who Are the Leading Companies in the E-KYC Market and Their Approaches?

- Jumio Corporation employs AI-powered biometrics and liveness detection, forming alliances with fintechs to penetrate emerging markets and prioritize fraud prevention.

- Trulioo offers extensive global data networks via APIs, focusing on regulatory compliance and reusable identities to enable seamless cross-border operations.

- Onfido (Entrust IDV) utilizes machine learning for document and facial analysis, incorporating hybrid AI-human oversight to ensure accuracy in regulated environments.

- Sumsub delivers comprehensive platforms with advanced anti-fraud features, targeting crypto and fintech with efficient, scalable onboarding solutions.

- Veriff emphasizes intuitive designs and wide document compatibility, using AI to optimize pass rates and meet diverse compliance needs.

- GB Group plc expands through acquisitions, enhancing biometric and data tools for insurance and telecom with a focus on regulatory adherence.

- IDnow GmbH specializes in video verification with automated ID tech, obtaining EU certifications to support rapid digital onboarding in banking.

What Emerging Patterns Are Influencing the E-KYC Market?

- Adoption of AI-driven liveness detection to counter deepfakes and synthetic fraud.

- Transition to perpetual KYC for ongoing monitoring over traditional periodic checks.

- Use of blockchain for decentralized, user-owned identities enhances privacy.

- Growth in video-based KYC for real-time, high-assurance customer interactions.

- Integration of explainable AI to comply with transparency-focused regulations.

- Development of interoperable digital IDs via frameworks like eIDAS in Europe.

- Focus on inclusive technologies for underserved populations in emerging regions.

What Market Segments Are Covered in the E-KYC Report?

By Product

- Identity Authentication & Matching

- Video Verification

- Digital ID Schemes

- Enhanced vs Simplified Due Diligence

By Deployment Mode

- Cloud-Based

- On-Premise

By End-Use

- Banks

- Financial Institutions

- E-Payment Service Providers

- Telecom Companies

- Government Entities

- Insurance Companies

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

E-KYC is the remote, digital verification of customer identities using technologies such as biometrics, AI, and video to fulfill KYC regulations efficiently.

Influential factors include AI advancements, escalating fraud risks, regulatory evolutions like eIDAS and FinCEN, digital banking surges, and digital ID programs in developing areas.

The market value is forecasted to rise from USD 1.10 billion in 2026 to USD 13.23 billion by 2035.

The CAGR is projected at 31.86% for the period.

North America will contribute notably with over 40% share, driven by regulatory stringency and technological maturity.

Key players are Jumio Corporation, Trulioo, Onfido (Entrust IDV), Sumsub, Veriff, GB Group plc, and IDnow GmbH.

Expect detailed coverage of market sizing, trends, segments, regions, competitors, drivers, restraints, and projections for strategic insights.

Stages comprise technology R&D (AI/biometrics), data aggregation, platform development, compliance integration, deployment, and maintenance/monitoring.

Trends lean toward privacy-enhanced biometrics and continuous verification, with consumers favoring quick, secure, and user-centric processes.

Regulations such as GDPR, AML directives, and eIDAS mandate robust systems but add costs; environmentally, digital shifts reduce paper use for sustainability.