E-Glass Fiber Market Size, Share and Trends 2026 to 2035

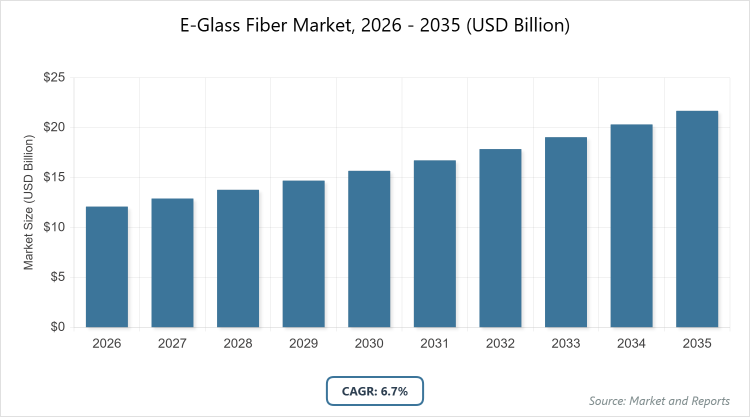

According to MarketnReports, the global E-Glass Fiber market size was estimated at USD 12.1 billion in 2025 and is expected to reach USD 23.1 billion by 2035, growing at a CAGR of 6.7% from 2026 to 2035. E-Glass Fiber Market is driven by increasing demand for lightweight and high-strength materials in automotive, construction, and renewable energy sectors.

What are the Key Insights of E-Glass Fiber Market?

- Market size valued at USD 12.1 billion in 2025 and projected to reach USD 23.1 billion by 2035

- CAGR of 6.7% during the forecast period 2026-2035

- Market is driven by rising adoption in lightweight composites for automotive electrification, construction boom, and renewable energy expansion

- Roving dominates the product type segment with 57% share due to its versatility in filament winding and pultrusion processes enabling high-strength composites

- Construction dominates the application segment with 35% share as it provides durable reinforcement in building materials like panels and pipes amid urbanization trends

- Building & construction dominates the end-user industry segment with 40% share owing to demand for corrosion-resistant and lightweight materials in infrastructure projects

- Asia Pacific dominates with 45% market share attributed to rapid industrialization, manufacturing hubs in China and India, and supportive policies for composites

What is E-Glass Fiber?

The E-glass fiber market revolves around a type of alkali-free borosilicate glass fiber known for its excellent electrical insulation properties, high tensile strength, corrosion resistance, and cost-effectiveness, making it a staple reinforcement material in composite manufacturing. It is produced through melting raw materials like silica sand, limestone, and alumina at high temperatures, then extruding into fine filaments that are bundled into various forms for enhanced mechanical performance in end products. The market definition includes the production, distribution, and application of these fibers in industries requiring durable, lightweight composites, such as automotive for fuel efficiency, construction for structural integrity, wind energy for turbine blades, and electronics for circuit boards, driven by the shift toward sustainable and high-performance materials that reduce weight while maintaining strength and thermal stability.

What are the Market Dynamics in E-Glass Fiber?

Growth Drivers

The growth drivers in the E-glass fiber market are anchored in the escalating need for lightweight materials across transportation and renewable energy sectors, where E-glass fibers enable significant weight reduction in electric vehicles and wind turbine blades, improving energy efficiency and performance. Advancements in composite manufacturing techniques, such as automated fiber placement and resin infusion, enhance production scalability and cost-effectiveness, allowing broader adoption in aerospace and marine applications. The global push for sustainability, including regulations favoring recyclable composites and low-emission materials, further accelerates demand as E-glass offers an eco-friendly alternative to metals. Rising infrastructure investments in emerging economies, coupled with innovations in fiber coatings for better adhesion and durability, support market expansion by addressing performance requirements in harsh environments.

Restraints

Restraints in the E-glass fiber market include volatility in raw material prices, such as silica and boric acid, which increase production costs and impact profitability for manufacturers. Environmental concerns over energy-intensive glass melting processes and waste generation during fiber production pose regulatory challenges, potentially slowing adoption in eco-sensitive regions. Competition from advanced alternatives like carbon fiber, which offers superior strength-to-weight ratios despite higher costs, limits E-glass penetration in high-end applications like aerospace. Supply chain disruptions, including geopolitical tensions affecting mineral sourcing, and the need for specialized equipment in downstream processing add barriers for smaller players.

Opportunities

Opportunities in the E-glass fiber market emerge from the expanding electric vehicle sector, where fibers can be integrated into battery enclosures and structural components for enhanced safety and range. Innovations in bio-based resins and hybrid composites open doors for sustainable product lines, appealing to green building initiatives and consumer goods. Growth in Asia Pacific and Latin America through infrastructure projects and wind farm developments provides untapped potential for localized production and partnerships. Collaborations with tech firms for smart composites embedded with sensors could revolutionize applications in IoT-enabled construction and automotive, driving premium segment growth.

Challenges

Challenges in the E-glass fiber market involve achieving consistent quality in large-scale production, as variations in fiber diameter and sizing can affect composite performance and lead to defects. Recycling complexities for glass fiber composites hinder circular economy efforts, requiring investments in new technologies for fiber recovery. Skilled labor shortages in advanced manufacturing and the high capital costs for upgrading furnaces to low-emission models strain smaller suppliers. Balancing cost pressures with demands for higher-performance variants, amid fluctuating energy prices, remains a key hurdle for sustained competitiveness.

E-Glass Fiber Market: Report Scope

| Report Attributes | Report Details |

| Report Name | E-Glass Fiber Market |

| Market Size 2025 | USD 12.1 Billion |

| Market Forecast 2035 | USD 23.1 Billion |

| Growth Rate | CAGR of 6.7% |

| Report Pages | 220 |

| Key Companies Covered | Owens Corning, Jushi Group Co. Ltd., PPG Industries Inc., Saint-Gobain Vetrotex, Nippon Electric Glass Co. Ltd., Taishan Fiberglass Inc., 3B-The Fibreglass Company, Johns Manville, Chongqing Polycomp International Corp., Knauf Insulation, and Others |

| Segments Covered | By Product Type (Roving, Chopped Strand, Yarn, Mat, Fabric, CSM, CFM, DUCS, Woven Roving, Multi-End Roving, and Others), By Application (Construction, Automotive, Aerospace, Wind Energy, Electronics, Marine, Pipe & Tank, Consumer Goods, Electrical, Industrial, and Others), By End-User Industry (Building & Construction, Transportation, Electrical & Electronics, Renewable Energy, Aerospace & Defense, Marine, Pipe & Tank, Consumer Goods, and Others), and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the E-Glass Fiber Market Segmented?

The E-Glass Fiber market is segmented by product type, application, end-user industry, and region.

Based on Product Type Segment. Roving is the most dominant with 57% share, followed by chopped strand as the second most dominant at 25%. Roving’s dominance arises from its suitability for continuous processes like pultrusion and weaving, which drive the market by enabling high-volume production of strong, lightweight composites for wind blades and automotive parts, reducing material waste and enhancing structural integrity; chopped strand supports growth as the second dominant through its use in injection molding for quick-dispersing reinforcement in thermoplastics, propelling efficiency in construction and consumer goods applications.

Based on Application Segment. Construction is the most dominant with 35% share, followed by automotive at 28%. Construction’s leading role stems from the fiber’s corrosion resistance and strength in reinforcing concrete, panels, and roofing, driving market growth by supporting durable infrastructure amid global urbanization; automotive follows as second dominant by leveraging E-glass in composites for weight reduction in vehicles, particularly EVs, which helps lower emissions and improve fuel economy, contributing to overall sector expansion.

Based on End-User Industry Segment. Building & construction is the most dominant with 40% share, followed by transportation at 30%. Building & construction dominates due to extensive use in insulation, facades, and structural elements for enhanced durability and energy efficiency, propelling market growth through compliance with green building standards; transportation as second dominant utilizes fibers in vehicle bodies and interiors for lightweighting, driving the market by aligning with regulatory demands for reduced carbon footprints in automotive and aerospace.

What are the Recent Developments in E-Glass Fiber?

- In October 2025, Owens Corning announced the launch of a new sustainable E-glass roving line with improved recyclability features, targeting wind energy applications to reduce environmental impact while maintaining high tensile strength.

- In November 2025, Jushi Group expanded its production capacity in India with a new facility focused on chopped strands for automotive composites, aiming to meet rising demand from electric vehicle manufacturers.

- In December 2025, Nippon Electric Glass partnered with a European aerospace firm to develop advanced E-glass yarns for lightweight aircraft interiors, incorporating fire-resistant coatings for enhanced safety.

- In January 2026, Saint-Gobain introduced bio-based sizing technologies for E-glass fabrics, designed for construction panels to improve adhesion and lower VOC emissions in building materials.

How is the Regional Analysis for E-Glass Fiber Market?

Asia Pacific to dominate the global market.

Asia Pacific dominates the E-glass fiber market due to rapid industrialization, massive infrastructure projects, and a booming automotive sector, supported by low production costs and abundant raw materials. China leads as the dominating country with extensive manufacturing capabilities, government incentives for renewable energy, and high export volumes, fostering innovations in composites for wind and EV applications.

North America holds a strong position with advanced R&D in composites and stringent regulations promoting lightweight materials in aerospace and transportation. The United States dominates the region through major investments in wind energy farms and automotive electrification, driving demand for high-performance E-glass products.

Europe exhibits steady growth fueled by sustainability initiatives and green building directives under the EU framework. Germany dominates within Europe owing to its engineering expertise in automotive and wind sectors, emphasizing recyclable composites for reduced emissions.

Latin America shows emerging growth through increasing construction and renewable energy investments amid economic recovery. Brazil leads the region with expanding wind power installations and infrastructure developments utilizing E-glass for durable reinforcements.

The Middle East and Africa are gradually expanding with focus on oil & gas alternatives and construction. Saudi Arabia dominates through Vision 2030 projects promoting diversified industries like renewables, incorporating E-glass in building and energy applications.

Who are the Key Market Players in E-Glass Fiber?

- Owens Corning leads with a focus on sustainable innovations like low-emission glass melting and recycled content fibers, employing global expansions and R&D partnerships to enhance composite performance in wind and automotive sectors.

- Jushi Group Co. Ltd. emphasizes high-volume production of rovings and chopped strands, with strategies centered on cost optimization and capacity builds in emerging markets to capture construction and transportation demand.

- PPG Industries Inc. specializes in advanced sizings and coatings for E-glass, using acquisition-driven growth and technology integrations to improve fiber-resin compatibility in aerospace and electronics.

- Saint-Gobain Vetrotex prioritizes eco-friendly fibers for building applications, with strategies involving circular economy initiatives and collaborations for bio-based composites.

- Nippon Electric Glass Co. Ltd. targets electronics and industrial uses with precision yarns, focusing on quality enhancements and Asian market dominance through localized manufacturing.

- Taishan Fiberglass Inc. concentrates on multi-end rovings for wind energy, employing export strategies and efficiency upgrades to compete in global renewables.

- 3B-The Fibreglass Company develops specialized mats and fabrics, with growth through European partnerships and sustainability certifications for construction.

- Johns Manville focuses on insulation and roofing reinforcements, using innovation in thermal-resistant fibers and North American expansions.

- Chongqing Polycomp International Corp. aims at automotive composites, with strategies on cost-competitive production and supply chain integrations in Asia.

- Knauf Insulation specializes in building insulation fibers, emphasizing energy-efficient products and regulatory compliance for green construction.

What are the Market Trends in E-Glass Fiber?

- Increasing integration of E-glass in electric vehicle components for weight reduction and battery protection

- Shift toward sustainable, recyclable E-glass composites to meet circular economy regulations

- Growth in wind energy applications with longer, stronger turbine blades using advanced rovings

- Adoption of bio-based sizings and low-VOC coatings for environmental compliance in construction

- Expansion of hybrid composites combining E-glass with thermoplastics for faster processing

- Rise in smart fibers embedded with sensors for structural health monitoring in infrastructure

- Focus on cost-effective production through automation and energy-efficient melting technologies

- Proliferation in aerospace for lightweight interiors and fuel-efficient designs

- Emphasis on corrosion-resistant variants for marine and pipe & tank sectors

- Integration with 3D printing for customized industrial parts and prototypes

What Market Segments and Subsegments are Covered in the E-Glass Fiber Report?

By Product Type

- Roving

- Chopped Strand

- Yarn

- Mat

- Fabric

- CSM

- CFM

- DUCS

- Woven Roving

- Multi-End Roving

- Others

By Application

- Construction

- Automotive

- Aerospace

- Wind Energy

- Electronics

- Marine

- Pipe & Tank

- Consumer Goods

- Electrical

- Industrial

- Others

By End-User Industry

- Building & Construction

- Transportation

- Electrical & Electronics

- Renewable Energy

- Aerospace & Defense

- Marine

- Pipe & Tank

- Consumer Goods

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

E-glass fiber is a type of borosilicate glass reinforcement material known for its electrical insulation, high strength, and corrosion resistance, widely used in composites for various industries.

Key factors include demand for lightweight composites in EVs and renewables, infrastructure growth, sustainability regulations, and advancements in manufacturing processes.

The market is projected to grow from approximately USD 12.9 billion in 2026 to USD 23.1 billion by 2035.

The CAGR is expected to be 6.7% during 2026-2035.

Asia Pacific will contribute notably, holding around 45% of the market share due to industrialization and manufacturing growth.

Major players include Owens Corning, Jushi Group Co. Ltd., PPG Industries Inc., Saint-Gobain Vetrotex, Nippon Electric Glass Co. Ltd., Taishan Fiberglass Inc., 3B-The Fibreglass Company, Johns Manville, Chongqing Polycomp International Corp., and Knauf Insulation.

The report offers in-depth analysis of market size, trends, segmentation, regional outlook, key players, drivers, and forecasts from 2026 to 2035.

Stages include raw material sourcing (silica, limestone), glass melting and fiber extrusion, sizing and bundling, composite manufacturing, distribution to end-users, and recycling or disposal.

Trends are evolving toward sustainable and recyclable fibers, with preferences shifting to lightweight, high-performance composites for eco-friendly applications in EVs and green buildings.

Regulatory factors include emissions standards for production and recycling mandates, while environmental factors involve reducing energy use in manufacturing and promoting low-impact materials.