E-Compass Market Size, Share and Trends 2026 to 2035

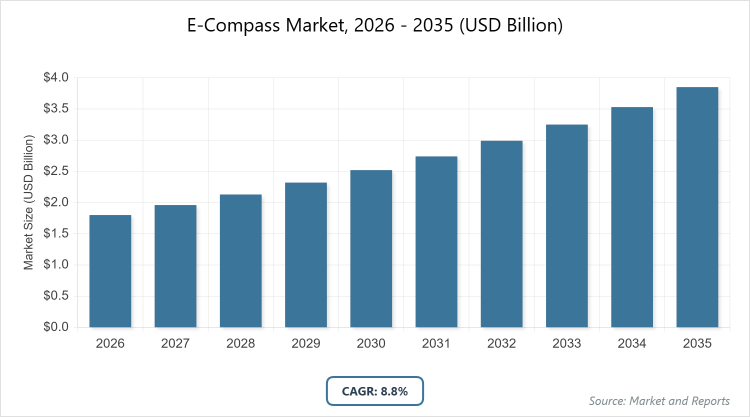

According to MarketnReports, the global E-Compass market size was estimated at USD 1.8 billion in 2025 and is expected to reach USD 4.2 billion by 2035, growing at a CAGR of 8.8% from 2026 to 2035. E-Compass Market is driven by increasing demand for navigation in consumer electronics, automotive, and drones.

What are the Key Insights into E-Compass?

- The global E-Compass market was valued at USD 1.8 billion in 2025 and is projected to reach USD 4.2 billion by 2035.

- The market is expected to grow at a CAGR of 8.8% during the forecast period from 2026 to 2035.

- The market is driven by the proliferation of smartphones and wearables, growth in autonomous vehicles, advancements in MEMS technology, and demand for AR/VR navigation.

- In the type segment, magneto-resistive e-compasses dominate with a 45% share due to their high sensitivity and low power consumption in consumer devices.

- In the application segment, consumer electronics dominate with a 50% share, as it enables accurate orientation in smartphones and tablets.

- In the end-user segment, consumer electronics manufacturers dominate with a 40% share owing to high-volume integration in gadgets.

- Asia Pacific dominates the regional market with a 50% share, driven by electronics manufacturing hubs in China and Taiwan, low costs, and rapid tech adoption.

What is the Industry Overview of E-Compass?

The E-Compass market involves electronic sensors that provide directional heading information by detecting the Earth’s magnetic field, integrated with accelerometers and gyroscopes for tilt compensation and accurate orientation in devices. Market definition includes magneto-resistive, hall-effect, and fluxgate-based compasses used in navigation systems, offering low-power, compact solutions for precise positioning while addressing challenges in magnetic interference, calibration, and integration with GPS for enhanced accuracy in diverse applications requiring orientation data.

What are the Market Dynamics of E-Compass?

Growth Drivers

The E-Compass market is propelled by the explosion of consumer electronics like smartphones and wearables, where accurate orientation enhances user experience in navigation apps and AR games, driving demand for compact, low-power sensors. Advancements in MEMS technology enable integration with accelerometers for tilt-compensated performance, expanding applications in drones and robotics. Rising adoption of autonomous vehicles requires reliable heading data for safe navigation, while IoT growth in smart cities demands e-compasses for asset tracking. Government investments in defense for UAVs and marine navigation further accelerate innovation and market expansion.

Restraints

High sensitivity to magnetic interference from urban environments and electronics limits accuracy, requiring complex calibration that increases costs. Competition from GPS and IMU alternatives offers more robust positioning in some applications, reducing e-compass reliance. Regulatory standards for electromagnetic compatibility add testing expenses. Supply chain vulnerabilities for rare earth materials in magnets affect production. Limited battery life in portable devices constrains power-hungry sensors, while economic slowdowns reduce consumer electronics spending.

Opportunities

Opportunities emerge from integrating e-compasses with 5G for enhanced AR/VR experiences, appealing to gaming and education sectors. Expansion into emerging markets with smartphone penetration offers growth for affordable sensors. Partnerships between chipmakers and auto firms can develop automotive-grade compasses for ADAS. The rise of wearable health devices requires precise motion tracking, opening niches. Development of interference-resistant designs using AI calibration presents innovative avenues.

Challenges

Challenges include mitigating magnetic distortions in complex environments, requiring ongoing R&D for robust algorithms. Rapid tech evolution demands frequent upgrades, straining manufacturer resources. Privacy concerns in location-based services complicate adoption. Shortage of skilled engineers in sensor design hinders innovation. Environmental factors like temperature variations affect performance, while trade tensions disrupt material supply.

E-Compass Market: Report Scope

| Report Attributes | Report Details |

| Report Name | E-Compass Market |

| Market Size 2025 | USD 1.8 Billion |

| Market Forecast 2035 | USD 4.2 Billion |

| Growth Rate | CAGR of 8.8% |

| Report Pages | 220 |

| Key Companies Covered | Bosch Sensortec, STMicroelectronics, Honeywell International, Asahi Kasei Microdevices, NXP Semiconductors, AKM (Asahi Kasei), MEMSIC Inc., PNI Sensor Corporation, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of E-Compass?

The E-Compass market is segmented by type, application, end-user, and region.

By Type. Magneto-resistive e-compasses are the most dominant subsegment, holding approximately 45% market share, due to their small size and low power, ideal for mobile devices. This dominance drives the market by enabling seamless integration in smartphones, boosting navigation accuracy. Hall-effect e-compasses rank as the second most dominant, with around 30% share, offering cost-effectiveness, propelling growth through automotive applications.

By Application. Consumer electronics emerges as the most dominant subsegment, capturing about 50% share, primarily because of smartphone and tablet demand. This leads to market growth by supporting location services and AR. Automotive navigation follows as the second most dominant, with roughly 25% share, enhancing vehicle systems, driving the market via ADAS adoption.

By End-User. Consumer electronics manufacturers represent the most dominant subsegment at about 40% share, driven by gadget integration needs. This dominance accelerates market expansion through high-volume production. The automotive industry ranks second most dominant, holding around 30% share, due to navigation requirements, contributing to growth via EV trends.

What are the Recent Developments in E-Compass?

- In January 2025, Bosch launched a new MEMS e-compass with AI calibration for automotive use.

- In October 2024, STMicroelectronics expanded its 9-axis sensor line for wearables.

- In July 2024, Honeywell partnered with a drone firm for interference-resistant compasses.

- In April 2024, Asahi Kasei introduced low-power hall-effect sensors for IoT.

- In February 2024, NXP Semiconductors acquired a startup for advanced magneto-resistive tech.

What is the Regional Analysis of E-Compass?

- Asia Pacific to dominate the global market.

Asia Pacific holds the largest share at approximately 50%, with China as the dominating country, due to massive electronics manufacturing, low production costs, and rapid 5G adoption. This region’s growth is fueled by smartphone exports, automotive boom, and investments in drones, positioning it as the epicenter of e-compass consumption and innovation. Massive smartphone clusters in Shenzhen drive demand for magneto-resistive sensors. India’s consumer electronics growth subsidizes wearable integration. Japan’s precision engineering tradition favors high-sensitivity compasses.

South Korea’s automotive industry requires automotive-grade solutions. Cultural emphasis on tech adoption accelerates training programs. Export-oriented policies enhance global competitiveness. Rising middle-class consumption increases smartphone and wearable demand. Environmental regulations push for low-power designs. Vocational programs build expertise in sensor integration across the region. Strong supply chains enable quick deployment of MEMS sensors.

North America follows closely, driven by tech R&D and defense applications, where the United States dominates through companies like Honeywell. Growth stems from AR/VR demand and autonomous vehicles, though higher costs moderate expansion. Defense contracts in California drive high-precision fluxgate compasses. NASA’s use in spacecraft navigation sets benchmarks. University-industry partnerships at MIT and Stanford advance sensor fusion. High investment in drones boosts UAV compasses. Strict quality standards ensure market preference for certified devices. Reshoring of electronics manufacturing boosts domestic demand. Emphasis on autonomous driving increases the demand for automotive components. Collaborative networks with Canada enhance cross-border supply chains. Focus on AR/VR gaming drives consumer sensor demand. Tech hubs in Texas expand industrial applications. Government incentives for defense tech promote innovation. Corporate consolidation in robotics increases large-scale deployments.

Europe exhibits strong performance with emphasis on automotive and IoT, led by Germany through Bosch and automotive giants. The region’s expansion benefits from EU funding for digital tech and focus on smart cities. Horizon Europe programs finance sensor fusion projects. The UK’s advanced robotics hubs in Bristol promote the adoption of drones. Multilingual compliance aids diverse markets like France and Italy. REACH regulations ensure safe material usage. Industry consortia share calibration best practices. Aging infrastructure renewal projects adopt surveying compasses. Vocational training centers build expertise in sensor applications. Green deal policies promote low-power designs. Nordic countries emphasize sustainable IoT sensors. Eastern European expansion in automotive drives demand. Strict export standards enhance global competitiveness. Focus on industrial automation increases factory sensor needs. Collaborative R&D across borders advances automotive components.

Latin America shows moderate advancement, dominated by Brazil’s growing electronics and auto sectors, supported by foreign investments, though limited by infrastructure. Mexico benefits from NAFTA ties, facilitating tech transfers from North America. Government digital initiatives in Argentina promote education in sensor technologies. The rise of EVs in Chile creates demand for navigation compasses. However, currency fluctuations impact import costs for high-end devices. Emerging drone manufacturing in Colombia is adopted for mapping. Regional trade pacts like Mercosur ease equipment imports. Vocational training expands in Peru for industrial applications. Biodiversity concerns influence eco-friendly sensor designs. Urban expansion drives consumer electronics demand. Foreign aid supports tech park development in smaller nations. Collaborative efforts with U.S. firms enhance supply chains. Focus on affordable devices increases smartphone compasses.

The Middle East and Africa remain emerging, with the United Arab Emirates leading through smart city and drone projects, constrained by lower tech access but promising via diversification. Saudi Arabia’s Vision 2030 funds R&D centers for localized sensor use. South Africa’s mining sector adopts equipment navigation. Technology partnerships with European firms build expertise in Egypt. However, water scarcity impacts cooling in high-end systems. Investments in solar farms create demand for drone compasses. OPEC policies stabilize oil-related applications. Vocational initiatives in Nigeria train for future jobs. Emerging labs in Kenya require sensor tech for research. Focusing on sustainable development goals promotes green innovations. Oil-funded smart city projects in Qatar drive high-end deployments. Collaborative regional efforts enhance knowledge sharing.

What are the Key Market Players in E-Compass?

- Bosch Sensortec. Bosch focuses on MEMS e-compasses for automotive, investing in AI for calibration.

- STMicroelectronics. STMicroelectronics emphasizes low-power sensors, pursuing integration in wearables.

- Honeywell International. Honeywell develops interference-resistant compasses, targeting aerospace and drones.

- Asahi Kasei Microdevices. Asahi Kasei offers hall-effect solutions, expanding in IoT markets.

- NXP Semiconductors. NXP acquires tech for magneto-resistive sensors, focusing on automotive ADAS.

- AKM (Asahi Kasei). AKM specializes in high-sensitivity compasses, strategizing on consumer electronics.

- MEMSIC Inc. MEMSIC invests in tilt-compensated designs, targeting robotics.

- PNI Sensor Corporation. PNI emphasizes fluxgate for precision, expanding in marine navigation.

What are the Market Trends in E-Compass?

- Integration with IMU for 9-axis sensor fusion.

- Rise of low-power designs for battery life in wearables.

- Growth in interference mitigation with AI.

- Expansion in AR/VR for immersive navigation.

- Adoption in autonomous robots and drones.

- Focus on miniaturization for IoT devices.

What Market Segments and Subsegments are Covered in the E-Compass Report?

By Type

- Hall-Effect E-Compasses

- Magneto-Resistive E-Compasses

- Fluxgate E-Compasses

- MEMS E-Compasses

- Tilt-Compensated E-Compasses

- 3-Axis E-Compasses

- 6-Axis E-Compasses

- 9-Axis E-Compasses

- Digital E-Compasses

- Analog E-Compasses

- Others

By Application

- Consumer Electronics

- Automotive Navigation

- Aerospace & Defense

- Marine Navigation

- Robotics

- Surveying & Mapping

- Drones & UAVs

- Wearables

- Gaming Devices

- Industrial Equipment

- Others

By End-User

- Consumer Electronics Manufacturers

- Automotive Industry

- Aerospace & Defense

- Marine Industry

- Robotics Companies

- Surveying Firms

- Drone Manufacturers

- Wearable Device Makers

- Gaming Industry

- Industrial Sector

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

E-Compasses are electronic sensors that detect magnetic fields for directional navigation in devices like smartphones and vehicles.

Key factors include consumer electronics growth, autonomous vehicle demand, MEMS advancements, and AR/VR expansion.

The market is projected to grow from USD 1.8 billion in 2025 to USD 4.2 billion by 2035.

The CAGR is expected to be 8.8%.

Asia Pacific will contribute notably, holding around 50% share due to electronics manufacturing.

Major players include Bosch Sensortec, STMicroelectronics, Honeywell International, Asahi Kasei Microdevices, and NXP Semiconductors.

The report provides detailed analysis of size, trends, segments, regional outlook, key players, and forecasts.

Stages include component sourcing, sensor assembly, calibration, integration, distribution, and after-sales support.

Trends evolve toward sensor fusion and miniaturization, with preferences for low-power, accurate devices.

Electromagnetic compatibility regulations and environmental standards for rare earth materials influence production.