Dry Mortar Market Size, Share and Trends 2026 to 2035

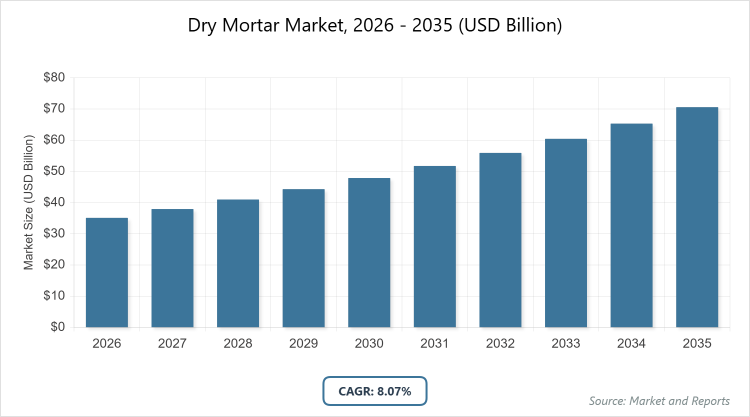

According to MarketReports, the global dry mortar market size was estimated at USD 35.1 billion in 2026 and is expected to reach USD 70.6 billion by 2035, growing at a CAGR of 8.07% from 2026 to 2035. The global dry mortar market is primarily driven by rapid urbanization and a surge in infrastructure development, which necessitate faster, more efficient, and high-quality construction materials over traditional on-site mixing.

What are the Key Insights into the Dry Mortar Market?

- The global dry mortar market is projected to grow from approximately USD 35.0 billion in 2026 to USD 70.0 billion by 2035, reflecting a compound annual growth rate (CAGR) of around 7.0%.

- Among types, masonry mortar dominates as the leading subsegment, essential for bricklaying and structural integrity.

- In application segments, render holds the dominant position, widely used for exterior and interior wall finishes.

- By end-use, residential is the most prominent, driven by housing construction demands.

- Asia Pacific emerges as the dominant region, contributing the largest market share due to rapid urbanization and infrastructure growth.

What is the Dry Mortar Industry?

Industry Overview

The dry mortar industry involves the production and distribution of pre-mixed, ready-to-use construction materials composed of cement, sand, and additives that require only water addition at the site for applications such as plastering, masonry, tiling, and flooring. These products offer advantages like consistent quality, reduced waste, faster application, and enhanced performance compared to traditional wet mortars, catering to residential, commercial, and industrial building projects where efficiency and durability are paramount.

Blending modern manufacturing techniques with sustainable formulations, the market addresses key construction needs by minimizing on-site mixing errors and labor costs, while incorporating specialized variants for waterproofing, insulation, or repair, ultimately supporting global infrastructure development and renovation activities in an era of rapid urbanization and eco-conscious building practices.

What Drives the Dry Mortar Market?

Growth Drivers

The dry mortar market is driven by accelerating urbanization and infrastructure projects worldwide, which demand efficient, high-quality construction materials to meet tight deadlines and reduce labor dependencies, coupled with rising adoption in emerging economies where modern building techniques are replacing traditional methods.

Technological advancements in formulation, such as eco-friendly additives and automated mixing systems, enhance product performance and appeal to sustainability-focused regulations, while increasing investments in residential and commercial real estate boost demand for specialized applications like tile adhesives and renders. Additionally, the shift toward prefabricated construction and green building certifications promotes dry mortar for its minimal waste and consistent results, propelling market expansion through improved supply chain efficiencies and cost savings.

Restraints

Fluctuating raw material prices for cement and additives, influenced by global supply chain disruptions and geopolitical factors, increase production costs and challenge pricing stability for manufacturers in competitive markets. Limited awareness and skilled labor in developing regions hinder widespread adoption, as traditional wet mortar practices persist due to perceived lower upfront costs. Moreover, stringent environmental regulations on emissions and waste during production add compliance burdens, while overcapacity in certain areas leads to price wars that erode profit margins.

Opportunities

The push for sustainable construction opens avenues for bio-based and recycled additive formulations in dry mortar, aligning with green building standards and attracting premium pricing in eco-regulated markets. Emerging infrastructure booms in Asia and Africa present untapped potential through localized production facilities and partnerships with governments for affordable housing initiatives. Furthermore, digitalization in supply chains, including IoT for inventory management and customized product delivery, enables differentiation and entry into niche segments like repair mortars for aging structures.

Challenges

Navigating diverse regional building codes and quality standards complicates product customization and international trade, increasing R&D expenses for compliant formulations. Intense competition from low-cost imports in unregulated markets undermines established players, while environmental scrutiny over high-energy production processes demands investments in cleaner technologies. Additionally, logistical issues in transporting bulky dry mixes to remote sites pose distribution challenges, requiring innovative packaging solutions amid volatile fuel costs.

Dry Mortar Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Dry Mortar Market |

| Market Size 2025 | USD 35.1 Billion |

| Market Forecast 2035 | USD 70.6 Billion |

| Growth Rate | CAGR of 8.07% |

| Report Pages | 225 |

| Key Companies Covered | Saint-Gobain Weber, Sika AG, LafargeHolcim, Ardex Group, Mapei S.p.A., BASF SE, and CEMEX S.A.B. de C.V. |

| Segments Covered | By Type, By Application, By End-Use, By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Dry Mortar Market Segmented?

The dry mortar market is segmented by type, material, end-use, and region.

By type, including masonry mortar, plaster mortar, tile adhesive mortar, and others, with masonry mortar emerging as the most dominant due to its critical role in structural bonding for bricks and blocks, offering superior strength and ease of use in large-scale projects; this dominance drives the market by supporting foundational construction needs and enabling volume sales in infrastructure, while tile adhesive mortar ranks as the second most dominant, prized for its adhesion properties in flooring and wall tiling, contributing through growth in interior finishing and renovation sectors.

By application, the market divides into render, plaster, tile adhesive, grouts, and others, where render dominates owing to its extensive use in exterior wall coatings for weather resistance and aesthetics, fueled by urban development; its prevalence propels market expansion by integrating with architectural trends, whereas plaster follows as the second dominant, essential for smooth interior surfaces, enhancing growth via residential and commercial finishing demands.

By end-use, segments include residential, commercial, and industrial, with residential leading as it addresses housing booms and renovations, driven by population growth; this segment fuels overall dynamics by generating steady demand and fostering innovations like quick-set formulas, while commercial secures second place, utilized in offices and retail for durable finishes, supporting resilience through large-project procurements.

What are the Recent Developments in the Dry Mortar Market?

- In 2023, Saint-Gobain Weber expanded its dry mortar production capacity in Asia with a new facility in India, incorporating sustainable additives to meet green building standards and capture growing residential demand.

- In 2024, Sika AG launched an eco-friendly tile adhesive mortar line with reduced carbon footprint, targeting European markets amid stringent environmental regulations and boosting its sustainability portfolio.

- In early 2025, LafargeHolcim partnered with a tech firm for AI-optimized mixing processes, enhancing product consistency and efficiency for industrial applications in North America.

How Does Regional Performance Vary in the Dry Mortar Market?

- Asia Pacific to dominate the market

Asia Pacific leads the dry mortar market, propelled by massive infrastructure investments, urbanization, and government housing schemes; China dominates this region with its vast manufacturing base, export prowess, and demand from mega-projects, fostering innovation in cost-effective formulations, while India contributes through rapid construction growth. Japan and Southeast Asian nations further bolster the region with advanced formulations for seismic-resistant buildings and sustainable urban developments, alongside South Korea’s focus on high-tech additives for smart cities and Vietnam’s emerging role in export-oriented production.

North America exhibits strong performance, supported by renovation trends and sustainable building codes; the United States stands out as the dominating country, leveraging advanced R&D and commercial projects, with Canada adding through infrastructure upgrades. Mexico enhances regional ties via cross-border trade and growing residential demand, driven by NAFTA/USMCA benefits and increasing adoption in affordable housing initiatives.

Europe maintains a mature market, influenced by EU green directives and heritage restorations; Germany emerges as the leading country, excelling in high-quality exports and eco-innovations, while France and the UK propel adoption in residential sectors. Italy and Spain contribute via tourism-driven renovations and Mediterranean climate-adapted products, with the Netherlands and Scandinavia emphasizing energy-efficient mortars for cold-weather applications and circular economy compliance.

Latin America shows emerging growth, driven by urban housing needs; Brazil predominates with industrial expansions and public works, supporting local adaptations amid economic recovery. Argentina and Chile support through mining-related infrastructure and seismic-resistant mortars, while Colombia gains traction via post-conflict rebuilding and Peru through coastal development projects.

The Middle East & Africa region represents developing potential, focused on oil-funded projects; the United Arab Emirates leads via luxury developments and imports, with Saudi Arabia advancing through Vision 2030 initiatives. South Africa grows via affordable housing programs, though logistics and raw material access remain hurdles in sub-Saharan areas, complemented by Qatar’s World Cup legacy infrastructure and Egypt’s New Administrative Capital driving specialized demand.

Who are the Key Market Players in the Dry Mortar Industry?

- Saint-Gobain Weber focuses on sustainability through eco-additives and facility expansions in emerging markets.

- Sika AG invests in R&D for specialized formulations and acquisitions for global reach.

- LafargeHolcim pursues partnerships for tech optimization and supply chain efficiencies.

- Ardex Group emphasizes quality certifications and niche repair products.

- Mapei S.p.A. adopts vertical integration for cost control and innovation in adhesives.

- BASF SE leverages chemical expertise for advanced additives and green solutions.

- CEMEX S.A.B. de C.V. focuses on regional expansions and sustainable sourcing.

What are the Current Market Trends in Dry Mortar?

- Increasing adoption of eco-friendly formulations with recycled aggregates and low-emission additives.

- Integration of automation in production for consistent quality and reduced labor.

- Growth in specialized mortars for waterproofing and insulation applications.

- Expansion of e-commerce for direct procurement in construction.

- Focus on rapid-setting mixes for faster project timelines.

- Rise in hybrid mortars combining cement with polymers for enhanced durability.

- Shift toward regional manufacturing to cut logistics costs.

What Market Segments are Covered in the Report?

By Type

-

- Masonry Mortar

- Plaster Mortar

- Tile Adhesive Mortar

- Others

By Application

-

- Render

- Plaster

- Tile Adhesive

- Grouts

- Others

By End-Use

-

- Residential

- Commercial

- Industrial

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Dry mortar is a pre-blended mixture of cement, sand, and additives used in construction, requiring only water addition for applications like plastering and masonry.

Key factors include urbanization, sustainable construction trends, technological advancements, and infrastructure investments in emerging regions.

The market is projected to grow from approximately USD 35.1 billion in 2026 to USD 70.6 billion by 2035, driven by construction demands.

The compound annual growth rate (CAGR) is expected to be around 8.07% from 2026 to 2035, reflecting steady expansion.

Asia Pacific will contribute notably, holding the largest share due to rapid development and population growth.

Major players include Saint-Gobain Weber, Sika AG, LafargeHolcim, Ardex Group, Mapei S.p.A., BASF SE, and CEMEX S.A.B. de C.V., driving growth via sustainability and expansions.

The report provides insights into size, trends, segmentation, regional analysis, players, and forecasts for strategic planning.

Stages include raw material sourcing (cement, sand), blending and packaging, distribution, and end-user application in construction.

Trends are shifting toward eco-friendly and automated products, with preferences for quick-set, durable mixes in sustainable projects.

Regulations on emissions drive green innovations, while environmental concerns promote low-waste formulations, increasing costs but fostering growth.