Distributed Energy Generation Market Size, Share and Trends 2026 to 2035

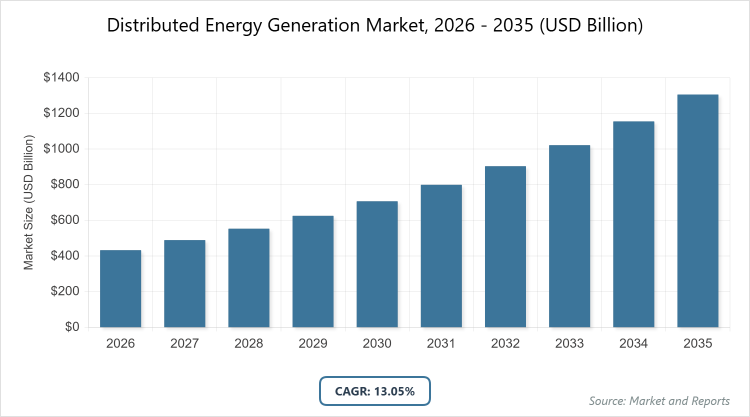

The global Distributed Energy Generation Market size was estimated at USD 433.11 Billion in 2025 and is expected to reach USD 1,303.34 Billion by 2035, growing at a CAGR of 13.05% from 2026 to 2035. The distributed energy generation market is primarily driven by the rising global demand for grid resilience and energy security, the rapidly declining costs of solar and battery storage, and aggressive government decarbonization mandates aimed at reducing greenhouse gas emissions.

What are the Key Insights?

- Global market value projected at USD 433.11 billion in 2026, reaching USD 1,303.34 billion by 2035.

- Anticipated CAGR of 13.05% from 2026 to 2035.

- Dominant subsegment in technology: Solar PV, holding the largest share due to widespread adoption and cost reductions.

- Dominant subsegment in end-use industry: Commercial, leading owing to high demand for efficient on-site power.

- Dominant region: Asia-Pacific, accounting for the highest market share driven by rapid urbanization and renewable investments.

What is the Industry Overview?

The Distributed Energy Generation Market refers to the decentralized production of electricity from various small-scale energy sources located close to the point of consumption, such as solar photovoltaic panels, wind turbines, fuel cells, and microgrids, which reduce transmission losses and enhance energy reliability compared to traditional centralized power plants. This market encompasses technologies that integrate renewable and conventional sources to provide resilient, efficient power solutions for residential, commercial, and industrial users, supporting grid independence, sustainability goals, and energy security in diverse applications without incorporating quantitative metrics in its core definition.

What are the Market Dynamics?

Growth Drivers

The Distributed Energy Generation Market is fueled by the global shift toward renewable energy sources, driven by declining costs of solar and wind technologies, government incentives for clean energy adoption, and increasing electricity demand from urbanization and electrification trends, which collectively promote decentralized systems that offer flexibility, reduced carbon emissions, and enhanced grid resilience in regions prone to power outages. Technological advancements in energy storage and smart grid integration enable efficient management of intermittent renewables, attracting investments from utilities and private sectors aiming to optimize energy distribution and meet sustainability targets. Additionally, rising awareness of energy independence and the need for reliable power in remote areas further accelerate market growth, as distributed systems minimize dependency on aging infrastructure and support economic development through localized energy solutions.

Restraints

High initial capital investments for installing distributed energy systems, including solar panels, batteries, and microgrids, act as a major restraint in the Distributed Energy Generation Market, particularly in developing regions where financing options are limited and return on investment timelines are extended due to variable energy yields. Regulatory inconsistencies and grid interconnection challenges hinder seamless integration, as outdated policies may not accommodate bidirectional power flows or incentivize decentralized generation adequately. Moreover, technical issues like intermittency of renewables and the need for advanced control systems increase operational complexities, deterring widespread adoption among cost-sensitive consumers and utilities.

Opportunities

The expansion of microgrids and hybrid systems presents significant opportunities in the Distributed Energy Generation Market, as they enable resilient power supply in off-grid and disaster-prone areas, attracting funding from governments and international organizations focused on energy access and climate adaptation. Advancements in digital technologies, such as AI-driven optimization and blockchain for peer-to-peer energy trading, open avenues for innovative business models that empower consumers and enhance market efficiency. Furthermore, the growing electric vehicle ecosystem and demand for sustainable infrastructure in emerging economies create potential for integrated solutions that combine generation with storage and charging, fostering partnerships across sectors.

Challenges

Intermittency and variability of renewable sources pose ongoing challenges in the Distributed Energy Generation Market, requiring robust storage solutions and forecasting tools to ensure stable supply, which can escalate costs and complicate system design. Cybersecurity threats to connected smart grids and distributed assets increase vulnerability, necessitating advanced protective measures that may strain resources for smaller operators. Additionally, supply chain dependencies for critical components like semiconductors and rare earth materials can lead to delays and price fluctuations, impacting project timelines and scalability in a rapidly evolving market.

Currency Sorter Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Distributed Energy Generation Market |

| Market Size 2025 | USD 433.11 Billion |

| Market Forecast 2035 | USD 1,303.34 Billion |

| Growth Rate | CAGR of 13.05% |

| Report Pages | 215 |

| Key Companies Covered |

Siemens AG, General Electric (GE), Schneider Electric SE, Vestas Wind Systems A/S, Bloom Energy Corporation, Tesla, Inc., Enel Green Power, ABB Ltd. |

| Segments Covered | By Technology, By End-Use Industry, By Region. |

| Regions Covered | Asia Pacific, North America, Europe, Latin America, The Middle East and Africa |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation?

Technology Segmentation

In the technology segmentation of the Distributed Energy Generation Market, solar PV emerges as the most dominant subsegment, followed by fuel cells as the second most dominant. Solar PV leads because of its scalability, declining installation costs, and supportive policies like tax credits and net metering, driving the market by enabling widespread deployment in residential and commercial sectors to reduce reliance on fossil fuels and lower electricity bills through efficient, clean energy production. Fuel cells, the second dominant, gain prominence for their high efficiency and low emissions in continuous power applications, contributing to market growth by providing reliable backup and baseload power in industrial and data center settings, aligning with decarbonization goals.

End-Use Industry Segmentation

Within the end-use industry segmentation of the Distributed Energy Generation Market, commercial stands out as the most dominant subsegment, with industrial as the second most dominant. Commercial dominates owing to the sector’s focus on cost savings and sustainability, where distributed systems like rooftop solar and microgrids optimize energy use in offices and retail spaces, fueling market expansion by meeting corporate ESG targets and reducing operational expenses amid rising utility rates. Industrial, the second dominant, benefits from on-site generation for energy-intensive processes, aiding growth by enhancing reliability and efficiency in manufacturing, minimizing downtime, and supporting energy-intensive operations with hybrid renewable solutions.

What are the Recent Developments?

- In December 2025, Pioneer Power Solutions, Inc. launched PRYMUS, a mobile power delivery platform evolved from e-Boost, targeting distributed MW-scale power needs for AI and data centers in industrial markets.

- In March 2025, the power and utilities sector formed the Open Power AI Consortium, involving energy companies, tech firms, and researchers to develop AI solutions for integrating distributed energy resources and managing grid loads.

- In June 2025, a leading Asian utility partnered to launch a blockchain-enabled decentralized energy trading platform, facilitating peer-to-peer exchanges and enhancing distributed generation adoption.

- In February 2025, Schneider Electric introduced EcoStruxure Microgrid Advisor updates using AI to optimize distributed operations, reducing costs by up to 30% for industrial clients.

- In October 2025, the US announced new incentives under the Inflation Reduction Act extension, boosting distributed solar and storage installations nationwide.

What is the Regional Analysis?

North America maintains a strong position in the Distributed Energy Generation Market, supported by advanced regulatory frameworks, tax incentives like the Investment Tax Credit, and high adoption of solar PV and storage systems in response to grid modernization needs and extreme weather events. The United States dominates this region, with its robust innovation ecosystem, widespread rooftop solar deployments in states like California and Texas, and corporate commitments to renewables, driving market growth through investments in microgrids and hybrid systems that enhance energy resilience and support the transition to low-carbon economies.

Asia-Pacific leads the Distributed Energy Generation Market as the largest and fastest-growing region, propelled by massive energy demand from population growth, industrialization, and government initiatives for renewable integration to combat pollution and achieve energy security. China dominates, with its extensive solar and wind deployments, national policies like the 14th Five-Year Plan emphasizing distributed renewables, and manufacturing prowess in PV modules, accelerating market expansion by enabling affordable, large-scale adoption in urban and rural areas for sustainable development.

Europe exhibits steady growth in the Distributed Energy Generation Market, driven by EU directives for carbon neutrality, feed-in tariffs, and community energy projects that promote decentralized renewables amid energy transition efforts. Germany dominates, leveraging its Energiewende policy for high solar and wind penetration, advanced grid infrastructure, and incentives for prosumers, fostering market advancement through innovative storage and smart grid technologies that ensure stability and reduce fossil fuel dependency.

Latin America is emerging in the Distributed Energy Generation Market, fueled by abundant solar and wind resources, rural electrification needs, and policies attracting foreign investments for renewable projects. Brazil dominates, with its hydropower heritage complemented by growing solar distributed systems, supportive auctions, and net metering regulations, propelling growth by addressing energy access in remote areas and supporting economic diversification through clean power.

The Middle East and Africa region is gaining traction in the Distributed Energy Generation Market, supported by solar potential, off-grid solutions for underserved areas, and diversification from oil dependency through renewable initiatives. Saudi Arabia dominates, with Vision 2030 driving massive solar projects and distributed systems, enabling market progress by integrating renewables into grids and providing reliable power for industrial and residential sectors in arid climates.

Who are the Key Market Players and Their Strategies?

Siemens AG invests heavily in digitalization and smart grid technologies, partnering with utilities for microgrid solutions and focusing on hybrid systems to enhance efficiency and expand in emerging markets.

General Electric (GE) emphasizes innovation in wind and gas turbines, pursuing acquisitions in renewables and AI-driven optimization to strengthen its portfolio in industrial applications.

Schneider Electric SE prioritizes sustainability through EcoStruxure platforms, collaborating on energy management software and targeting commercial sectors with integrated storage solutions.

Vestas Wind Systems A/S focuses on onshore and offshore wind turbines, investing in R&D for larger, more efficient models and forming alliances for distributed wind projects.

Bloom Energy Corporation specializes in fuel cell technology, expanding clean energy servers for data centers and pursuing partnerships for hydrogen integration.

Tesla, Inc. drives growth via solar and battery products, leveraging vertical integration and software for virtual power plants to capture residential and commercial markets.

Enel Green Power pursues global renewable projects, emphasizing solar and wind hybrids with storage, and investing in community-based distributed generation.

ABB Ltd. concentrates on electrification and automation, developing advanced inverters and grid solutions to support seamless renewable integration.

What are the Market Trends?

- Increasing integration of energy storage with renewables to address intermittency and enhance grid stability.

- Adoption of AI and digital twins for predictive maintenance and optimization of distributed systems.

- Growth in microgrids for resilient power in remote and urban areas amid climate challenges.

- Rise of peer-to-peer energy trading platforms enabled by blockchain technology.

- Focus on hydrogen fuel cells as a clean, continuous power source for industrial applications.

What Market Segments are Covered in the Report?

By Technology

- Micro-Turbines

- Combustion Turbines

- Micro-Hydropower

- Reciprocating Engines

- Fuel CellsWind Turbines

- Solar PV

By End-Use Industry

- Residential

- Commercial

- Industrial

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

The Distributed Energy Generation Market refers to the decentralized production of electricity from small-scale sources near consumption points, including renewables like solar PV and wind, supporting grid resilience and sustainability.

Key factors include renewable energy adoption, government incentives, technological advancements in storage, rising electricity demand, and grid modernization efforts.

The market is projected to grow from USD 433.11 billion in 2026 to USD 1,303.34 billion by 2035.

The anticipated CAGR is 13.05% from 2026 to 2035.

Asia-Pacific will contribute significantly, driven by rapid industrialization and renewable investments in China and India.

Major players include Siemens AG, General Electric, Schneider Electric SE, Vestas Wind Systems A/S, and Bloom Energy Corporation.

The report provides comprehensive analysis including market size, forecasts, segmentation, regional insights, competitive landscape, and emerging trends.

Stages include technology development, component manufacturing, system integration, installation, operation, and maintenance.

Trends show increasing preference for integrated storage, AI optimization, and microgrids, with consumers favoring sustainable, resilient solutions.

Stringent emissions regulations, renewable incentives, and climate goals promote adoption, while grid policies influence integration and expansion.