Digital Health Market Size, Share and Trends 2026 to 2035

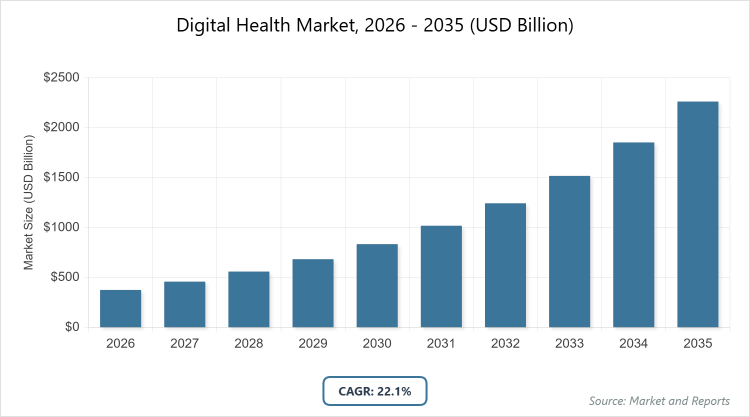

According to our latest research, the global digital health market is valued at approximately USD 375 billion in 2025 and is projected to reach USD 1,511 billion by 2035, growing at a CAGR of 22.1% from 2026 to 2035. The Digital Health Market is primarily driven by the rising prevalence of chronic diseases and an aging global population, which necessitate cost-effective remote monitoring, personalized care, and advanced AI-driven diagnostics.

What are the Key Insights into the Digital Health Market?

- The global digital health market is valued at approximately USD 375 billion in 2025 and is projected to reach USD 1,511 billion by 2035.

- The market is expected to grow at a compound annual growth rate (CAGR) of 22.1% from 2026 to 2035.

- Among components, the services segment dominates due to its essential role in implementation and maintenance.

- In technology types, telehealthcare is the leading subsegment, driven by remote care demands.

- By end-user, the healthcare providers segment holds the largest share, fueled by operational efficiency needs.

- North America is the dominated region, supported by advanced tech adoption and regulatory support.

What is the Digital Health Market?

Industry Overview

The digital health market refers to the broad spectrum of technologies and services that leverage digital tools to enhance healthcare delivery, management, and outcomes, including telemedicine, mobile health apps, wearable devices, electronic health records, and AI-based analytics that enable remote patient monitoring, personalized medicine, and efficient data sharing among stakeholders. It represents a fusion of healthcare and information technology aimed at improving accessibility, reducing costs, and promoting preventive care by connecting patients, providers, and payers through interconnected platforms that support real-time decision-making and chronic disease management. This market addresses key challenges in traditional healthcare systems by incorporating innovations like cloud computing, big data, and the Internet of Things to foster patient empowerment, operational efficiency, and equitable access to medical services across diverse demographics and geographies.

What Drives the Digital Health Market?

Growth Drivers

The digital health market is propelled by the surging incidence of chronic diseases and an expanding geriatric population that requires ongoing monitoring and virtual care solutions, enhanced by breakthroughs in AI and machine learning for accurate diagnostics and individualized treatment regimens, while widespread mobile device usage and improved connectivity enable seamless adoption of health apps and wearables worldwide. Government incentives, rising healthcare expenditures, and the enduring impact of the pandemic on remote care preferences further stimulate growth by integrating these technologies into routine practices, thereby optimizing resource utilization and health equity in varied settings.

Restraints

Prominent restraints in the digital health market encompass stringent regulatory requirements for data security and privacy that increase operational complexities and deter rapid deployment, coupled with interoperability deficits among platforms that fragment data flows and limit comprehensive care integration. Substantial initial investments for advanced infrastructure, alongside disparities in digital literacy and access in developing areas, also impede market penetration, exacerbating challenges in achieving uniform adoption across global healthcare ecosystems.

Opportunities

Opportunities in the digital health market are amplified by the evolution of generative AI and blockchain for secure, efficient data handling and therapeutic innovations, facilitating partnerships between tech innovators and healthcare organizations to advance mental health solutions and precision medicine. The rise of hybrid care models and mHealth expansions in emerging economies offer pathways for cost-effective, scalable interventions that mitigate access barriers, generating novel business models through data monetization and collaborative ecosystems.

Challenges

Challenges in the digital health market include standardizing data exchange protocols amid heterogeneous systems, which demands collaborative industry efforts and investments to ensure holistic patient insights and care continuity. Diverse international regulations complicate scalability, while addressing digital divides in underserved regions involves overcoming infrastructure limitations and ethical concerns in AI applications to maintain inclusivity and stakeholder confidence.

Digital Health Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Digital Health Market |

| Market Size 2025 | USD 375 Billion |

| Market Forecast 2035 | USD 1,511 Billion |

| Growth Rate | CAGR of 22.1% |

| Report Pages | 220 |

| Key Companies Covered | Teladoc Health, Koninklijke Philips N.V., Abbott Laboratories, Siemens Healthineers AG, Medtronic Plc, GE HealthCare Technologies Inc., Apple Inc., Google LLC, Cerner Corporation (Oracle), and McKesson Corporation |

| Segments Covered | By Component, By Technology, By End-User, By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Digital Health Market Segmented?

The digital health market is segmented by component, technology, end-user, and region.

By Component, The component segmentation in the digital health market is led by services, which dominate because they provide crucial integration, training, and ongoing support for complex systems like EHRs and telehealth, driving market growth by ensuring high adoption rates and minimizing disruptions in healthcare workflows that enhance overall system efficacy and user satisfaction. Software follows as the second most dominant, offering core functionalities for analytics and user interfaces, yet it ranks behind services as the latter’s consultative expertise is vital for customizing solutions to diverse needs, thereby accelerating market progression through improved scalability and compliance.

By Technology, Telehealthcare stands as the most dominant technology segment in the digital health market, owing to its facilitation of virtual consultations and remote monitoring that expand access and lower costs, propelling growth by addressing healthcare shortages and chronic care requirements in a post-pandemic era. mHealth is the second most dominant, utilizing mobile devices for health tracking and engagement, but it trails telehealthcare since the latter delivers more clinically robust interactions, contributing to market expansion via better patient adherence and resource optimization.

By End-User, Healthcare providers constitute the most dominant end-user segment in the digital health market, leveraging tools for enhanced workflows and data-informed decisions that drive growth by boosting efficiency in high-volume settings like hospitals. Patients and consumers are the second most dominant, adopting apps and wearables for personal health oversight, though they lag behind providers due to institutional budgets and mandates, fostering market development through preventive care emphases.

What are the Recent Developments in the Digital Health Market?

- In December 2025, the IQVIA Institute released its Digital Health Trends 2025 report, highlighting accelerated access and reimbursement pathways for digital therapeutics, with new CMS codes enabling Medicare coverage for digital mental health treatments, which is poised to boost adoption among older populations and expand market reach for mental health apps.

- In December 2025, EY US identified eight health trends for 2026, including AI-driven efficiencies and regulatory adaptations to federal funding cuts, influencing strategic planning for healthcare executives amid evolving policy landscapes.

- In December 2025, Forbes published 10 healthcare industry predictions for 2026, noting the continued rise of digital health IPOs and transaction volumes, alongside AI speed bumps and the mainstreaming of alternative care models like MAHA.

- In October 2025, OpenLoop’s CEO predicted key 2026 trends such as AI integration in virtual care, expansion of patient-centered models, and advancements in healthcare accessibility through digital platforms.

- In December 2025, J.P. Morgan outlined 2025 healthtech trends extending into 2026, emphasizing digital platforms for care access and AI improvements in workflows, signaling ongoing innovation in the sector.

- In December 2025, StartUs Insights’ Digital Health Market Report for 2026 detailed a 2.12% annual growth rate with 7560 startups, focusing on software-driven platforms and connected technologies shaping the industry.

- In November 2025, Mia-Care highlighted top 2026 trends like generative AI for clinical augmentation, interoperability implementations, and cybersecurity enhancements for trustworthy data handling.

- In December 2025, Signify Research shared 2026 predictions, forecasting a pivotal M&A year for EHRs and population-health vendors to integrate AI-enhanced platforms.

How Does the Digital Health Market Vary by Region?

- North America to dominate the market

North America leads the digital health market with the highest revenue share, underpinned by sophisticated infrastructure, substantial investments, and policies like CMS reimbursements that promote telehealth and AI adoption; the United States dominates as the key country, contributing predominantly through tech innovation hubs and widespread integration in healthcare systems, driving growth by managing chronic diseases and curbing costs in an advanced economy.

Europe maintains a strong position in the digital health market, supported by GDPR-compliant data frameworks and EU initiatives for cross-border health data spaces that encourage innovation and trust; Germany and the United Kingdom are dominating countries, with Germany leading via its robust industrial and IT sectors for device manufacturing, and the UK advancing through NHS-led AI and digital record systems, collectively enhancing market growth via preventive and interoperable solutions.

Asia Pacific emerges as the fastest-growing region in the digital health market, propelled by urbanization, mobile proliferation, and governmental digital health strategies to combat access inequalities; China and India dominate, with China at the forefront through large-scale AI hospital integrations and India via affordable mHealth for vast rural populations, together accelerating expansion by capitalizing on demographic scales for cost-effective, tech-enabled care.

Latin America shows progressive growth in the digital health market, aided by telehealth expansions to reach remote communities and collaborations with global players; Brazil dominates, harnessing its extensive healthcare network and digitalization efforts like unified health systems for EHR adoption, navigating infrastructure limitations to promote inclusive and economical healthcare advancements.

The Middle East & Africa region experiences emerging traction in the digital health market through mobile solutions addressing workforce and geographic barriers; the United Arab Emirates and Saudi Arabia lead, with the UAE pioneering smart health in urban developments and Saudi Arabia via Vision 2030’s AI and telemedicine investments, jointly advancing the market by resolving sectoral skill gaps despite regional connectivity challenges.

Who are the Key Market Players in the Digital Health Market and

What Are Their Strategies?

- Teladoc Health: Teladoc focuses on virtual care expansions, AI triage integrations, and acquisitions for chronic management to lead telemedicine with accessible, comprehensive platforms.

- Koninklijke Philips N.V.: Philips emphasizes connected devices, AI imaging, and remote monitoring partnerships to innovate in hospital and home care settings.

- Abbott Laboratories: Abbott pursues wearable innovations like continuous glucose monitors, data analytics collaborations, and chronic care expansions to dominate device segments.

- Siemens Healthineers AG: Siemens strategies include AI diagnostics, cloud IT solutions, and acquisitions for workflow optimizations in clinical environments.

- Medtronic Plc: Medtronic leverages connected implants, predictive AI, and diabetes partnerships to advance remote patient monitoring.

- GE HealthCare Technologies Inc.: GE focuses on AI radiology, digital twins, and data platform alliances for diagnostic enhancements.

- Apple Inc.: Apple integrates ecosystem health features, privacy-focused sharing, and provider collaborations for consumer tech leadership.

- Google LLC: Google develops wearables and cloud analytics, AI investments via DeepMind, and predictive tool partnerships for data scaling.

- Cerner Corporation (Oracle): Cerner optimizes EHRs with AI, Oracle mergers for security, and global interoperability expansions.

- McKesson Corporation: McKesson digitizes supply chains with AI forecasting, pharmacy integrations, and oncology partnerships for efficiency.

What are the Current Market Trends in the Digital Health Market?

- Integration of AI and machine learning for clinical augmentation and workflow automation, reducing burdens and improving accuracy.

- Expansion of telehealth and remote patient monitoring in hybrid care models to enhance accessibility post-pandemic.

- Rise in wearable and IoT devices for real-time data, with emphasis on interoperability and data spaces.

- Focus on cybersecurity and trustworthy AI amid regulatory pressures for data protection.

- Growth of generative AI in virtual assistants and personalized medicine for patient-centered approaches.

- Increased mergers and acquisitions among EHR and population-health vendors for AI-enhanced platforms.

- Shift toward consumer-directed models with direct-to-consumer digital health solutions.

- Adoption of blockchain for secure data exchange and fraud prevention in health systems.

- Emphasis on sustainability in digital infrastructure to address environmental impacts of data centers.

- Surge in reimbursement policies for digital therapeutics, particularly in mental health and chronic care.

What Market Segments are Covered in the Report? (Market Segments Covered in the Report)

By Component

- Hardware

- Software

- Services

By Technology

- Telehealthcare

- mHealth, Health Analytics

- Digital Health Systems

By End-User

- Healthcare Providers

- Payers

- Patients/Consumers

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Digital Health Market - Industry Analysis

Chapter 4. Global Digital Health Market- Competitive Landscape

Chapter 5. Global Digital Health Market - Component Analysis

Chapter 6. Global Digital Health Market - Technology Analysis

Chapter 7. Global Digital Health Market - End-User Analysis

Chapter 15. Digital Health Market - Regional Analysis

Chapter 16. Company Profiles

Frequently Asked Questions

Digital health encompasses the use of digital technologies, including telemedicine, wearables, AI, and mobile apps, to optimize healthcare delivery, patient engagement, and system efficiency across providers, payers, and consumers.

Key factors include rising chronic disease burdens, AI advancements for personalized care, government reimbursements for telehealth, wearable adoption surges, and data analytics enhancements, offset by privacy concerns and interoperability hurdles.

The digital health market is projected to grow from approximately USD 375 billion in 2026 to USD 1,511 billion by 2035, reflecting robust technological and demand-driven expansion.

The compound annual growth rate (CAGR) for the digital health market is expected to be 22.1% from 2026 to 2035.

North America will contribute notably, holding the largest share due to advanced infrastructure, funding, and policies, with the United States as the primary driver.

Major players include Teladoc Health, Koninklijke Philips N.V., Abbott Laboratories, Siemens Healthineers AG, Medtronic Plc, GE HealthCare Technologies Inc., Apple Inc., Google LLC, Cerner Corporation (Oracle), and McKesson Corporation, propelling growth via innovations and strategic alliances.

The global digital health market report provides detailed insights on size, forecasts, segments, drivers, restraints, opportunities, regions, players, developments, and strategies to support stakeholder decisions.

The value chain includes product development, software and hardware manufacturing, content creation, marketing and sales, distribution, and customer and patient services, ensuring integrated delivery.

Trends are advancing toward AI personalization, hybrid care, and cybersecurity, while preferences favor on-demand, privacy-secure apps and wearables for proactive management over traditional methods.

Regulatory factors like GDPR, HIPAA, and CMS codes enforce data security and reimbursements, increasing costs but building trust; environmental factors involve sustainable data centers to mitigate e-waste and energy impacts from devices.