Digital Education Publishing Market Size, Share and Trends 2026 to 2035

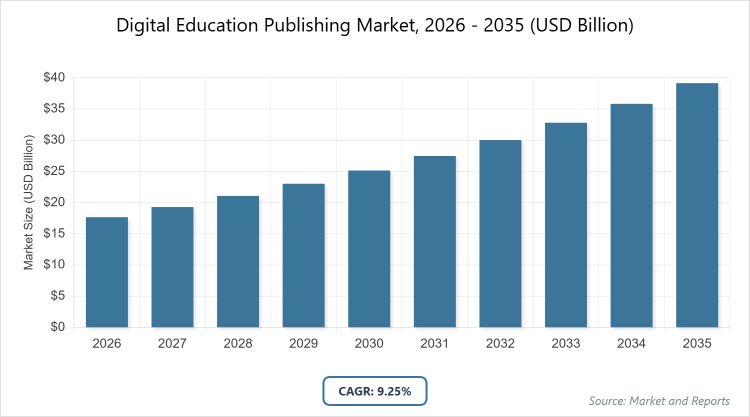

According to MarketnReports, the global Digital Education Publishing Market size was estimated at USD 17.65 Billion in 2025 and is expected to reach USD 42.76 Billion by 2035, growing at a CAGR of 9.25% from 2026 to 2035. Digital Education Publishing Market is driven by the integration of advanced technologies such as AI, AR, and VR to enhance interactive and personalized learning experiences.

What is the Industry Overview of the Digital Education Publishing Market?

The Digital Education Publishing Market encompasses the creation, distribution, and consumption of educational content in digital formats, replacing or supplementing traditional print materials with interactive, accessible, and adaptable resources designed for modern learning environments. This market includes digital textbooks, e-books, online courses, multimedia supplements, and assessment tools that leverage technology to deliver education across various platforms and devices. Market definition refers to the sector focused on publishing educational materials digitally, catering to students, educators, institutions, and corporate learners, emphasizing personalization, interactivity, and data-driven insights to improve learning outcomes and accessibility worldwide.

What are the Key Insights for the Digital Education Publishing Market?

- The global Digital Education Publishing Market was valued at USD 17.65 Billion in 2025 and is projected to reach USD 42.76 Billion by 2035.

- The market is expected to grow at a CAGR of 9.25% during the forecast period from 2026 to 2035.

- The market is driven by the increasing adoption of e-learning platforms, mobile learning solutions, and advanced technologies like AI and AR for personalized education.

- Textbooks dominate the Content Type segment with approximately 40% share due to their role in providing structured, curriculum-aligned content essential for standardized education.

- Web-based dominates the Platform segment with about 45% share because it offers robust accessibility across multiple devices and comprehensive content libraries.

- Students dominate the User Type segment with roughly 50% share owing to their reliance on diverse digital resources that cater to varied learning styles and enable self-paced study.

- Direct Sales dominate the Distribution Model segment with around 40% share as it fosters tailored relationships between publishers and institutions for customized solutions.

- Artificial Intelligence dominates the Technology Integration segment with approximately 35% share due to its capability in enabling personalized learning paths and analytics for improved educational outcomes.

- North America dominates the regional segment with 45% share because of high technology adoption rates, presence of key players, and supportive government initiatives in education digitization.

What are the Market Dynamics in the Digital Education Publishing Market?

Growth Drivers

The growth drivers of the Digital Education Publishing Market are primarily fueled by the rapid integration of cutting-edge technologies such as artificial intelligence, augmented reality, and virtual reality, which transform traditional learning into immersive and interactive experiences, allowing for personalized content delivery that adapts to individual learner needs and paces. This technological advancement not only enhances student engagement but also provides educators with real-time analytics to refine teaching methods, with the AI in education market alone projected to expand significantly, driving overall market momentum. Additionally, the surge in e-learning platform adoption, accelerated by global shifts toward remote and hybrid education models post-pandemic, has increased demand for digital content, as institutions seek cost-effective, scalable solutions to reach broader audiences. Mobile learning’s rise, expected to constitute over half of online learning by the mid-2020s, further propels growth by enabling on-the-go access via smartphones and apps, particularly in developing regions with high mobile penetration. Substantial investments in educational technology, surpassing hundreds of billions globally, underscore a commitment to innovation, while the emphasis on lifelong learning and professional upskilling creates sustained demand for flexible digital resources that support continuous education beyond formal schooling.

Restraints

Restraints in the Digital Education Publishing Market include the persistent digital divide, where unequal access to high-speed internet and devices in underdeveloped regions hinders widespread adoption, limiting market penetration and exacerbating educational inequalities. High initial development costs for creating sophisticated digital content, incorporating technologies like AR and VR, pose barriers for smaller publishers, as they require significant investments in software, talent, and infrastructure without guaranteed immediate returns. Content piracy and intellectual property concerns also restrain growth, as easy digital replication undermines revenue streams and discourages innovation in premium materials. Moreover, resistance to change from traditional educators and institutions accustomed to print-based methods slows transition, compounded by concerns over screen time’s impact on health and learning efficacy, leading to regulatory scrutiny and hesitant implementation in some markets.

Opportunities

Opportunities in the Digital Education Publishing Market abound with the expansion into emerging economies, where rising internet penetration and government initiatives for digital education create untapped potential for localized, affordable content tailored to regional curricula and languages. The development of AI-driven personalized learning platforms offers a chance to differentiate offerings, enabling adaptive systems that track progress and recommend resources, thereby attracting partnerships with tech giants and educational bodies. Subscription-based models present growth avenues by providing recurring revenue through flexible access to updated libraries, appealing to budget-conscious institutions and learners seeking value. Furthermore, collaborations between traditional publishers and edtech startups can foster innovative ecosystems, integrating gamification and immersive tools to capture the corporate training sector, which demands skill-specific, on-demand content for workforce development.

Challenges

Challenges facing the Digital Education Publishing Market involve market fragmentation, with numerous players offering disparate platforms and content standards, complicating interoperability and user experience, which requires industry-wide standardization efforts to streamline adoption. Ensuring data privacy and security in digital platforms is a critical hurdle, as handling sensitive learner information amid rising cyber threats demands robust compliance with regulations like GDPR, potentially increasing operational costs. The need for continuous content updates to keep pace with evolving curricula and technologies strains resources, while addressing diverse learning needs across global audiences, including accessibility for disabled users, adds complexity to design and deployment. Finally, measuring the true effectiveness of digital education compared to traditional methods remains challenging, as inconsistent metrics and varying study outcomes can erode stakeholder confidence and slow investment.

Digital Education Publishing Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Digital Education Publishing Market |

| Market Size 2025 | USD 17.65 Billion |

| Market Forecast 2035 | USD 42.76 Billion |

| Growth Rate | CAGR of 9.25% |

| Report Pages | 220 |

| Key Companies Covered |

Pearson, McGraw-Hill Education, Houghton Mifflin Harcourt, Cengage Learning, Wiley, Scholastic, Knewton, Instructure, Edmodo, and Others |

| Segments Covered | By Content Type, By User Type, By Distribution Model, By Technology Integration, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Digital Education Publishing Market?

The Digital Education Publishing Market is segmented by Content Type, Platform, User Type, Distribution Model, Technology Integration, and region. All the segments have been analyzed based on present and future trends and the market is estimated from 2026 to 2035.

Based on Content Type Segment, Textbooks emerge as the most dominant subsegment due to their foundational role in delivering structured, comprehensive knowledge aligned with academic curricula, making them indispensable for formal education systems worldwide, while Interactive Learning Tools rank as the second most dominant, offering multimedia and adaptive features that boost engagement and retention; Textbooks drive the market by ensuring reliable, standardized content that forms the backbone of digital transitions in schools and universities, whereas Interactive Learning Tools propel growth through innovation, catering to modern preferences for dynamic, gamified learning that improves outcomes and attracts tech-savvy users.

Based on Platform Segment, Web-based stands out as the most dominant subsegment for its versatility and broad accessibility across devices without requiring downloads, facilitating seamless integration into existing educational infrastructures, followed by Mobile Applications as the second most dominant, which provide portable, interactive experiences optimized for smartphones; Web-based platforms drive the market by supporting large-scale content delivery and collaboration, enabling institutions to scale operations efficiently, while Mobile Applications contribute to expansion by meeting the demand for flexible, anytime learning, particularly among younger demographics in mobile-first regions.

Based on User Type Segment, Students are the most dominant subsegment as they directly consume the bulk of digital resources for personal study and skill-building, reflecting the market’s learner-centric focus, with Educators as the second most dominant, utilizing tools to enhance instruction and assessment; Students drive the market through high-volume adoption of e-books and courses that democratize access to education, fostering self-directed learning, whereas Educators accelerate growth by leveraging digital analytics and resources to innovate teaching, thereby increasing overall platform stickiness and institutional investments.

Based on Distribution Model Segment, Direct Sales dominate as the primary subsegment by establishing strong, customized relationships with institutions for bulk licensing and tailored content, ensuring steady revenue, while Subscription Services are the second most dominant, offering ongoing access with updates for recurring value; Direct Sales drive the market by providing personalized solutions that build long-term partnerships and trust, supporting large-scale implementations, and Subscription Services fuel expansion through affordability and flexibility, appealing to dynamic educational needs and reducing upfront costs for users.

Based on Technology Integration Segment, Artificial Intelligence is the most dominant subsegment for its ability to personalize learning paths and provide actionable insights via data analytics, revolutionizing content delivery, followed by Augmented Reality as the second most dominant, which overlays interactive elements for immersive experiences; Artificial Intelligence drives the market by enabling adaptive, efficient education that scales to millions, improving retention and outcomes, while Augmented Reality contributes to growth by differentiating offerings with engaging, real-world applications that attract investment in next-gen tools.

What are the Recent Developments in the Digital Education Publishing Market?

- Pearson announced a strategic partnership with a leading AI technology firm in August to integrate advanced AI capabilities into its digital learning platforms, aiming to deliver highly personalized educational experiences that adapt in real-time to student performance and preferences, marking a significant step toward AI-driven innovation in the sector.

- McGraw-Hill Education launched a new suite of adaptive learning tools in September 2025, designed to offer immediate feedback to both students and educators, enhancing engagement and learning efficacy through data-informed adjustments, which underscores the company’s focus on leveraging technology for improved educational outcomes.

- Wiley expanded its digital content portfolio by acquiring a prominent online learning platform in October, allowing for the seamless integration of diverse learning modalities such as interactive simulations and multimedia resources, thereby strengthening its market position in providing comprehensive digital education solutions.

What is the Regional Analysis of the Digital Education Publishing Market?

North America to dominate the global market.

North America holds the largest share in the Digital Education Publishing Market, driven by advanced technological infrastructure, high internet penetration, and substantial investments in edtech, with the United States as the dominating country due to its concentration of key players like Pearson and McGraw-Hill Education, along with government policies promoting digital literacy; this region’s leadership facilitates rapid adoption of AI and AR-integrated content, enabling personalized learning at scale and supporting hybrid education models that enhance accessibility and outcomes across K-12 and higher education sectors.

Europe represents a significant portion of the market, characterized by strong digital transformation initiatives and EU-funded programs for educational innovation, with the United Kingdom leading as the dominating country through its robust publishing industry and tech-savvy institutions; Germany’s emphasis on vocational training and France’s focus on inclusive digital tools further bolster growth, as the region prioritizes data privacy and collaborative platforms to drive equitable access to quality digital content.

Asia-Pacific is experiencing the fastest growth, fueled by expanding internet access, rising smartphone usage, and government investments in digital education, with China as the dominating country owing to its massive online learning user base and initiatives like the “Internet Plus Education” plan, while India contributes through affordable mobile solutions; this region’s dynamism supports scalable, localized content that addresses diverse linguistic and cultural needs, accelerating market expansion in emerging economies.

South America shows emerging potential, supported by increasing digital adoption in urban areas and efforts to bridge educational gaps, with Brazil as the dominating country due to its large population and programs like the National Education Plan promoting e-learning; the region focuses on affordable subscription models and mobile apps to overcome infrastructure challenges, fostering gradual integration of interactive tools for improved literacy and skills development.

The Middle East and Africa exhibit nascent but promising growth, driven by investments in technology hubs and initiatives for accessible education, with the United Arab Emirates as the dominating country through visions like Dubai’s Smart Education strategy, alongside South Africa’s tech advancements; this area emphasizes cloud-based solutions to address connectivity issues, enabling region-specific content that supports lifelong learning and economic development.

Who are the Key Market Players in the Digital Education Publishing Market?

Pearson employs strategies focused on strategic partnerships with technology firms to integrate AI and adaptive learning into its platforms, emphasizing global expansion through localized content and acquisitions to enhance its digital ecosystem, thereby maintaining leadership in personalized education delivery.

McGraw-Hill Education prioritizes innovation in adaptive tools and real-time analytics, investing in R&D for interactive content while forming alliances with institutions for customized solutions, aiming to drive user engagement and retention in competitive markets.

Houghton Mifflin Harcourt adopts a content diversification approach, blending traditional publishing with digital enhancements like gamification, and pursues mergers to broaden its portfolio, targeting K-12 segments for sustained growth.

Cengage Learning focuses on subscription-based models and open educational resources to offer affordable access, leveraging data analytics for product refinement and expanding into corporate training to diversify revenue streams.

Wiley strategies include acquisitions of online platforms and emphasis on open access publishing, integrating multimedia for higher education, while collaborating with universities to co-create content that aligns with evolving curricula.

Scholastic concentrates on child-centric digital stories and interactive apps, partnering with schools for literacy programs and using data to personalize reading experiences, strengthening its position in early education.

Knewton specializes in AI-powered adaptive learning, offering platforms that analyze student data for tailored paths, and seeks integrations with major publishers to scale its technology across global markets.

Instructure builds on its Canvas LMS by enhancing cloud-based features and open-source collaborations, focusing on user-friendly interfaces to support hybrid learning environments in institutions worldwide.

Edmodo emphasizes community-driven platforms for educator collaboration, incorporating social features and mobile access, with strategies aimed at free-to-premium models to grow its user base in developing regions.

What are the Market Trends in the Digital Education Publishing Market?

- Shift toward interactive and personalized learning solutions, with rising demand for multimedia elements and adaptive technologies to boost student engagement and retention.

- Increased adoption of mobile learning, enabling on-the-go access and appealing to younger demographics in regions with high smartphone penetration.

- Emphasis on AI integration for data-driven education, providing analytics and customized content to improve learning outcomes.

- Growth in subscription and freemium models, offering flexible, cost-effective access to updated digital resources.

- Focus on sustainability in digital publishing, reducing reliance on print materials and promoting eco-friendly practices.

- Rise of collaborative platforms for knowledge sharing among educators and students, fostering community-based learning.

- Expansion into emerging markets with localized content to address cultural and linguistic diversity.

- Integration of AR and VR for immersive experiences, transforming traditional subjects into experiential learning.

What are the Market Segments and their Subsegments Covered in the Digital Education Publishing Market Report?

- Content Type

- Textbooks

- Supplementary Materials

- Interactive Learning Tools

- Assessment Resources

- Platform

- Web-based

- Mobile Applications

- Cloud-based Solutions

- User Type

- Students

- Educators

- Institutions

- Corporate Learners

- Distribution Model

- Direct Sales

- Subscription Services

- Freemium Model

- Technology Integration

- Artificial Intelligence

- Augmented Reality

- Virtual Reality

- Gamification

- By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Digital Education Publishing Market - Industry Analysis

Chapter 4. Global Digital Education Publishing Market- Competitive Landscape

Chapter 5. Global Digital Education Publishing Market - Content Type Analysis

Chapter 6. Global Digital Education Publishing Market - Platform Analysis

Chapter 7. Global Digital Education Publishing Market - User Type Analysis

Chapter 8. Global Digital Education Publishing Market - Distribution Model Analysis

Chapter 9. Digital Education Publishing Market - Regional Analysis

Chapter 10. Company Profiles

Frequently Asked Questions

The Digital Education Publishing Market involves the creation and distribution of educational content in digital formats, including e-books, interactive tools, and online resources for learning.

Key factors include technological advancements like AI and AR, rising e-learning adoption, mobile accessibility, edtech investments, and demand for personalized lifelong learning.

The market is estimated at USD 17.65 Billion in 2025 and projected to reach USD 42.76 Billion by 2035.

The CAGR is expected to be 9.25% during 2026-2035.

North America will contribute notably, holding approximately 45% share due to advanced infrastructure and key players.

Major players include Pearson, McGraw-Hill Education, Houghton Mifflin Harcourt, Cengage Learning, and Wiley.

The report provides in-depth analysis of market size, trends, segments, dynamics, regional insights, key players, and forecasts.

Stages include content creation, platform development, distribution, user adoption, and data analytics for refinement.

Trends are shifting toward interactive, mobile, and AI-personalized content, with preferences for flexible, on-demand learning experiences.

Factors include data privacy regulations like GDPR, accessibility standards, and sustainability pushes reducing print dependency.