Dental 3D Printer Market Size, Share and Trends 2026 to 2035

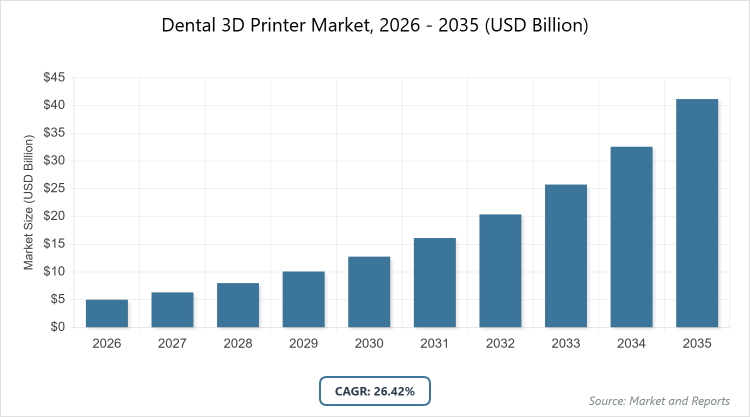

According to MarketnReports, the global Dental 3D Printer market size was estimated at USD 4.99 billion in 2025 and is expected to reach USD 51.96 billion by 2035, growing at a CAGR of 26.42% from 2026 to 2035. Dental 3D Printer Market is driven by the rapid adoption of digital dentistry and increasing demand for personalized dental solutions.

What are the Key Insights into Dental 3D Printer Market?

- The global dental 3D printer market size was valued at USD 4.99 billion in 2025 and is projected to reach USD 51.96 billion by 2035.

- The market is anticipated to grow at a CAGR of 26.42% during the forecast period from 2026 to 2035.

- The market is driven by technological advancements in 3D printing, rising demand for customized dental care, and the growing adoption of digital dentistry workflows.

- The vat photopolymerization segment dominated the technology segment with a significant share, driven by its ability to produce high-resolution and precise dental structures with fine details and complex geometries.

- The orthodontics segment dominated the application segment with 40% market share, owing to the increasing need for personalized aligners, braces, and retainers that enhance treatment efficiency and patient comfort.

- The dental laboratories segment dominated the end-use segment with 58% market share, as these facilities leverage scalable production capabilities and specialized expertise for high-volume, customized dental prosthetics.

- North America dominated the global market with 39% share, attributed to advanced healthcare infrastructure, high adoption of digital technologies, and a skilled workforce in the region.

What is the Industry Overview of Dental 3D Printer Market?

The dental 3D printer market encompasses the development, production, and utilization of additive manufacturing technologies specifically tailored for dental applications, enabling the creation of precise, customized dental prosthetics, models, and devices. Market definition refers to the ecosystem involving 3D printers, associated materials, and software used to fabricate items such as crowns, bridges, aligners, implants, and surgical guides through layer-by-layer construction from digital scans, revolutionizing traditional dental workflows by offering enhanced accuracy, reduced production times, and cost efficiencies for dental professionals and patients alike.

What are the Market Dynamics of Dental 3D Printer Market?

Growth Drivers

The primary growth drivers in the dental 3D printer market include continuous innovations in printing technologies, materials, and software that enable faster production of highly accurate and biocompatible dental devices, such as aligners and implants, meeting the rising patient demand for personalized treatments. Additionally, the aging global population and increased awareness of oral health are boosting the need for efficient dental restorations, while the integration of digital dentistry reduces production costs and time, making 3D printing an attractive option for clinics and labs seeking to streamline operations and improve patient outcomes.

Restraints

Key restraints involve the high initial costs of 3D printing equipment and materials, which can be prohibitive for smaller dental practices, alongside the complexity of software and regulatory compliance requirements that demand ongoing training and investments to ensure safety and quality standards are met. Compatibility issues between different software platforms can also lead to errors in design and production, further hindering widespread adoption in regions with limited technological infrastructure.

Opportunities

Opportunities arise from the development of advanced biocompatible materials like high-performance resins and ceramics that expand applications in long-lasting prosthetics and implants, coupled with the growing trend of in-clinic printing for same-day restorations that enhance patient satisfaction and operational efficiency. Emerging markets in Asia-Pacific present potential for expansion through increased investments in dental R&D and rising cosmetic dentistry demand, allowing companies to tap into underserved populations with affordable, customized solutions.

Challenges

Challenges include navigating stringent regulatory frameworks and evolving quality standards for 3D-printed dental products, which require substantial resources for compliance and can delay market entry for new innovations. Moreover, the need for specialized training to operate complex systems and address potential material limitations, such as durability in certain applications, poses barriers to full integration, particularly in resource-constrained settings where ongoing maintenance and updates are difficult to sustain.

Dental 3D Printer Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Dental 3D Printer Market |

| Market Size 2025 | USD 4.99 Billion |

| Market Forecast 2035 | USD 51.96 Billion |

| Growth Rate | CAGR of 26.42% |

| Report Pages | 220 |

| Key Companies Covered |

3D Systems, Inc., Stratasys Ltd., Formlabs Inc., Renishaw plc, Prodways Group, Dentsply Sirona, SprintRay Inc., Align Technology, and Others |

| Segments Covered | By Technology, By Application, By End-Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Dental 3D Printer Market?

The Dental 3D Printer market is segmented by technology, application, end-use, and region.

Based on Technology Segment, the vat photopolymerization segment is the most dominant, holding a leading market share due to its superior precision in creating intricate dental structures with high resolution and minimal material waste, which drives market growth by enabling rapid production of complex items like surgical guides and models. The polyjet technology segment is the second most dominant, valued for its multi-material capabilities that allow for realistic textures and colors in dental prosthetics, contributing to market expansion through enhanced aesthetic outcomes and versatility in applications such as crowns and bridges.

Based on Application Segment, the orthodontics segment is the most dominant with 40% share, as it facilitates the creation of customized aligners and retainers that improve treatment accuracy and patient compliance, propelling market growth by addressing the rising demand for non-invasive cosmetic corrections. The prosthodontics segment is the second most dominant, driven by its role in producing tailored veneers, crowns, and dentures with better fit and functionality, which supports overall market advancement through reduced production times and cost savings for extensive restorative procedures.

Based on End-Use Segment, the dental laboratories segment is the most dominant with 58% share, owing to its capacity for high-volume output and specialized customization of prosthetics like implants and bridges, fueling market growth by optimizing workflows and meeting large-scale demands from dental practices. The dental clinics segment is the second most dominant and fastest-growing, as it enables on-site production for quicker patient turnaround and personalized care, driving the market forward by integrating chairside solutions that enhance efficiency and reduce reliance on external labs.

What are the Recent Developments in Dental 3D Printer Market?

- In September 2024, Formlabs launched three new post-processing tools along with two innovative resin materials for SLA and SLS printing, including Clear Cast Resin and the certified BEGO VarseoSmile TriniQ Resin, expanding its material library to over 45 options and supporting broader applications in dental models and prosthetics.

- In May 2024, SprintRay announced a strategic partnership with Ivoclar to validate additional resins within its ecosystem, while also introducing the Pro 2 desktop 3D printer designed to accelerate dental care delivery through faster printing speeds and improved material compatibility.

- In July 2024, Stratasys unveiled the DentaJet XL, a high-speed 3D printer aimed at enhancing productivity in dental laboratories by reducing operational costs and enabling efficient production of multi-material dental appliances.

- Align Technology completed its 79 million euro acquisition of Cubicure, an Austrian polymer 3D printing firm, to bolster its innovation pipeline, leveraging the technology for scaling production of Invisalign molds and exploring direct printing of dental products.

What is the Regional Analysis of Dental 3D Printer Market?

North America to dominate the global market.

North America holds the dominant position in the dental 3D printer market with over 39% share, primarily led by the United States, where a skilled workforce, early adoption of advanced technologies, and robust healthcare infrastructure facilitate widespread use in producing implants, crowns, and orthodontic devices, supported by favorable reimbursement policies and high patient demand for personalized care.

Asia-Pacific is the fastest-growing region, projected at a CAGR of 27.11%, with China and Japan as key contributors due to increasing investments in R&D, rising awareness of cosmetic dentistry, expanding middle-class populations, and government initiatives promoting oral health, enabling greater access to affordable 3D-printed prosthetics and aligners.

Europe demonstrates strong growth through its advanced healthcare systems and emphasis on digital workflows, with Germany, France, and the United Kingdom dominating, driven by stringent regulatory standards for biocompatible materials, high demand for customized restorations among aging populations, and thriving dental tourism that boosts adoption of efficient printing technologies.

Latin America is emerging with significant potential, led by Brazil and Mexico, where demand for cost-effective, personalized dental solutions is rising alongside improvements in healthcare infrastructure, dental education programs, and private clinic expansions that integrate 3D printing for orthodontics, implants, and cosmetic procedures.

The Middle East and Africa offer growing opportunities, with the United Arab Emirates and Saudi Arabia as leading countries, fueled by expanding medical tourism, investments in modern dental clinics, government support for digital health initiatives, and increasing affordability of aesthetic treatments like crowns and aligners.

Who are the Key Market Players in Dental 3D Printer Market?

- 3D Systems, Inc. focuses on providing stereolithography-based printers and biocompatible materials for dental models, aligners, and surgical guides, employing strategies such as continuous R&D investments and partnerships to expand its portfolio and enhance precision in digital dentistry workflows.

- Stratasys Ltd. specializes in polymer-based systems like PolyJet printers for accurate prosthetics and dentures, with strategies including product launches like the DentaJet XL to improve lab efficiency, cost reduction, and market penetration in developed regions through strong distribution networks.

- Formlabs Inc. offers affordable resin-based SLA printers and a wide range of dental-grade resins for various applications, pursuing strategies of material innovation, such as launching new resins and post-processing tools, to make 3D printing accessible for smaller clinics and labs while building an extensive ecosystem.

- Renishaw plc emphasizes metal additive manufacturing for dental implants and frameworks, with strategies centered on laser-based technologies to ensure durability and biocompatibility, alongside collaborations with dental professionals to tailor solutions for complex restorative needs.

- Prodways Group provides DLP and MOVINGLight technologies with specialized resins for aligners and models, implementing strategies like technological advancements and targeted marketing to dental labs to boost production speed and scalability in competitive markets.

- Dentsply Sirona integrates 3D printing into comprehensive CAD/CAM workflows for restorations and prosthetics, using strategies such as acquisitions and software enhancements to create seamless digital ecosystems that support end-to-end dental solutions for clinics and laboratories.

- SprintRay Inc. delivers desktop printers, materials, and cloud software for digital dentistry, with strategies involving partnerships like with Ivoclar for resin validation and launches of advanced printers to enable faster, chairside production and broader material access.

- Align Technology leverages 3D printing for Invisalign production and direct device printing, employing acquisition strategies such as buying Cubicure to scale innovations and support its roadmap for personalized orthodontic treatments.

What are the Market Trends in Dental 3D Printer Market?

- Increasing integration of AI in 3D printing for automated design, predictive analytics, and treatment planning to enhance accuracy and reduce procedural errors.

- Growing shift toward chairside printing in dental clinics for same-day restorations, minimizing turnaround times and improving patient experiences.

- Rising demand for biocompatible and sustainable materials that mimic natural teeth aesthetics and durability, expanding applications in cosmetic dentistry.

- Expansion of educational programs and training through associations and online platforms to accelerate adoption among dental professionals.

- Surge in venture capital investments and collaborations between startups and established firms to drive innovation in compact, user-friendly printers.

- Emphasis on regulatory compliance and standardization to ensure safety and quality in 3D-printed dental products across global markets.

What Market Segments and their Subsegments are Covered in the Dental 3D Printer Report?

By Technology

-

- Vat Photopolymerization

- Polyjet Technology

- Fused Deposition Modelling

- Selective Laser Sintering

- Stereolithography

- Digital Light Processing

- Continuous Digital Light Manufacturing

- Others

By Application

-

- Orthodontics

- Prosthodontics

- Implantology

- Dentures

- Crowns and Bridges

- Surgical Guides

- Aligners

- Models

- Veneers

- Night Guards

- Others

By End-Use

-

- Dental Laboratories

- Dental Clinics

- Academic and Research Institutes

- Hospitals

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Dental 3D printers are additive manufacturing devices used to create precise, customized dental appliances such as prosthetics, models, aligners, and implants through layer-by-layer construction from digital designs.

Key factors include technological advancements in materials and software, rising demand for personalized dental care, adoption of digital dentistry, an aging population, and increasing awareness of oral health.

The market is projected to grow from USD 6.30 billion in 2026 to USD 51.96 billion by 2035.

The CAGR is expected to be 26.42% during 2026-2035.

North America will contribute notably, holding over 39% of the market share due to advanced infrastructure and high technology adoption.

Major players include 3D Systems, Inc., Stratasys Ltd., Formlabs Inc., Renishaw plc, Prodways Group, Dentsply Sirona, SprintRay Inc., and Align Technology.

The report provides in-depth analysis of market size, trends, segmentation, regional outlook, key players, drivers, restraints, opportunities, and forecasts from 2026 to 2035.

Stages include raw material sourcing, design and software development, printing and manufacturing, post-processing, quality control, distribution, and end-use application in dental settings.

Trends are shifting toward AI integration, sustainable materials, and chairside printing, while consumers prefer personalized, aesthetic, and quick-turnaround dental solutions.

Strict regulations for biocompatible materials and product safety, along with environmental concerns over material waste reduction and energy-efficient production, are influencing growth by promoting innovation and compliance.