Computer Vision in Healthcare Market Size, Share and Trends 2026 to 2035

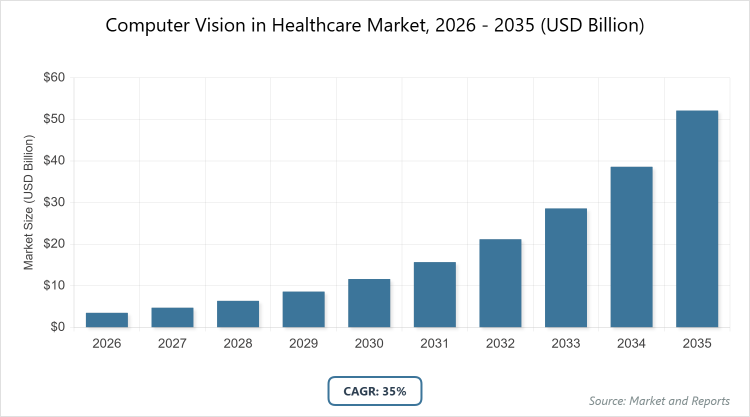

According to MarketnReports, the global Computer Vision in Healthcare market size was estimated at USD 3.5 billion in 2025 and is expected to reach USD 60 billion by 2035, growing at a CAGR of 35% from 2026 to 2035. Computer Vision in Healthcare Market is driven by the increasing adoption of AI for diagnostic imaging and disease detection.

What are the Computer Vision in Healthcare Key Insights?

- Market value in 2025: USD 3.5 billion; projected value in 2035: USD 60 billion.

- CAGR from 2026 to 2035: 35%.

- Market is driven by advancements in AI and machine learning algorithms, rising prevalence of chronic diseases, and increasing demand for automated diagnostic tools.

- Software segment dominates the component segment with 50% share due to its flexibility in integrating AI algorithms for image analysis and real-time processing, enabling scalable solutions across diverse healthcare applications.

- Medical imaging & diagnostics dominates the application segment with 40% share as it leverages computer vision for accurate interpretation of vast medical data volumes, improving diagnostic speed and reducing costs.

- Hospitals & clinics dominate the end-user segment with 55% share owing to high patient volumes and the need for efficient workflow management through automated imaging and monitoring systems.

- North America dominates with 37% share due to advanced healthcare infrastructure, high adoption of digital technologies, and supportive government policies promoting AI integration.

What is the Computer Vision in Healthcare Industry Overview?

The Computer Vision in Healthcare market encompasses technologies that enable machines to interpret and analyze visual data from medical images, videos, and other sources to support diagnostics, treatment, and operational efficiency in healthcare settings. This market integrates artificial intelligence and machine learning to process complex visual inputs, aiding in early disease detection, surgical precision, and patient monitoring. Market definition refers to the application of computer vision algorithms in healthcare for tasks such as image segmentation, object detection, and pattern recognition, transforming traditional medical practices into data-driven, automated processes that enhance accuracy and reduce human error.

What are the Computer Vision in Healthcare Market Dynamics?

Growth Drivers

The primary growth drivers for the Computer Vision in Healthcare market include rapid advancements in AI and machine learning, which enhance the accuracy of medical image analysis and enable real-time decision-making in diagnostics and surgeries. The increasing prevalence of chronic diseases, such as cancer and cardiovascular conditions, heightens the demand for early detection tools, where computer vision excels in identifying anomalies in imaging data more efficiently than traditional methods. Additionally, government initiatives and funding for AI adoption in healthcare, coupled with the rising need for automated systems to address healthcare workforce shortages, propel market expansion by improving operational efficiency and patient outcomes.

Restraints

Key restraints in the Computer Vision in Healthcare market stem from data privacy and security concerns, as handling sensitive medical images requires compliance with stringent regulations like HIPAA, which can complicate implementation and increase costs. High initial investment for infrastructure, including specialized hardware and software, poses a barrier for smaller healthcare facilities, limiting widespread adoption. Furthermore, the lack of standardized datasets for training AI models leads to variability in performance across different regions and demographics, potentially reducing trust in these technologies among healthcare professionals.

Opportunities

Opportunities in the Computer Vision in Healthcare market arise from the growing demand for personalized medicine, where computer vision can analyze patient-specific imaging data to tailor treatments and predict outcomes more precisely. The integration of edge computing allows for real-time processing in remote or resource-limited settings, expanding access to advanced diagnostics in underserved areas. Moreover, collaborations between tech companies and healthcare providers to develop hybrid AI solutions open avenues for innovation in areas like remote patient monitoring and drug discovery, fostering new revenue streams and market penetration.

Challenges

Challenges facing the Computer Vision in Healthcare market include the integration of these technologies with existing healthcare IT systems, which often requires significant upgrades and can disrupt workflows during transition. A shortage of skilled professionals trained in AI and computer vision hampers effective deployment and maintenance of these systems. Ethical issues, such as algorithmic bias in diverse patient populations, also present hurdles, necessitating ongoing research to ensure equitable and reliable applications across global healthcare scenarios.

Computer Vision in Healthcare Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Computer Vision in Healthcare Market |

| Market Size 2025 | USD 3.5 Billion |

| Market Forecast 2035 | USD 60 Billion |

| Growth Rate | CAGR of 35% |

| Report Pages | 220 |

| Key Companies Covered | NVIDIA Corporation, Intel Corporation, Microsoft Corporation, IBM Corporation, Google LLC, Siemens Healthineers AG, GE HealthCare, Koninklijke Philips N.V., Stryker, Fujitsu Limited, and Others |

| Segments Covered | By Component, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Computer Vision in Healthcare Market Segmentation?

The Computer Vision in Healthcare market is segmented by component, application, end-user, and region.

Based on Component Segment. The software segment leads due to its critical role in enabling AI-driven analysis and scalability. It dominates with a 50% share because of its adaptability in processing complex algorithms for tasks like image recognition, which drives efficiency in diagnostics and reduces reliance on manual interpretation. The hardware segment follows as the second most dominant, holding 30% share, as it provides the foundational processing power, such as GPUs and cameras, essential for capturing and handling high-resolution medical data, thereby supporting the overall market growth through enhanced performance and speed.

Based on Application Segment. Medical imaging & diagnostics is the most dominant application with 40% share, driven by its ability to automate the analysis of vast datasets from X-rays, MRIs, and CT scans, leading to faster and more accurate disease detection that propels market advancement. Surgeries rank as the second most dominant with 25% share, utilizing computer vision for real-time guidance and precision in procedures, minimizing errors and improving surgical outcomes, which contributes significantly to the market’s expansion.

Based on End-User Segment. Hospitals & clinics dominate the end-user segment with 55% share, as they handle high volumes of patients requiring immediate diagnostic and monitoring solutions, where computer vision streamlines workflows and enhances care quality, fueling market progress. Diagnostic centers are the second most dominant with 20% share, benefiting from specialized imaging needs that computer vision addresses through automated analysis, reducing turnaround times and costs, thus driving further adoption and growth in the sector.

What are the Recent Developments in Computer Vision in Healthcare?

- In March 2025, NVIDIA Corporation collaborated with GE HealthCare to develop autonomous diagnostic imaging systems using the Isaac for Healthcare platform, aiming to enhance real-time image processing and diagnostic accuracy.

- In April 2024, iCAD, Inc. partnered with RAD-AID to improve breast cancer detection using AI technology in underserved regions and low- and middle-income countries, focusing on expanding access to advanced imaging solutions.

- In March 2024, Microsoft and NVIDIA Corporation expanded their collaboration with integrations of NVIDIA’s generative AI and Omniverse technologies into Microsoft Azure and other services, supporting advancements in healthcare AI applications.

- In November 2024, Advanced Micro Devices, Inc. launched the Versal Premium Gen 2 FPGA, integrating Compute Express Link 3.1, to bolster AI capabilities in healthcare data processing and scalability.

What is the Computer Vision in Healthcare Regional Analysis?

North America to dominate the global market.

North America holds the dominant position in the Computer Vision in Healthcare market, driven by robust healthcare infrastructure, high adoption of AI technologies, and significant investments in research and development. The United States leads within the region, benefiting from favorable regulatory frameworks like FDA approvals for AI-enabled devices and a large patient base with chronic conditions requiring advanced diagnostics. This dominance is further supported by collaborations between tech giants and healthcare providers, enhancing innovation in medical imaging and patient monitoring.

Europe follows as a key region, with strong growth fueled by government initiatives promoting digital health and stringent data protection regulations that build trust in AI applications. Germany stands out as the dominating country, leveraging its advanced manufacturing and healthcare systems to integrate computer vision in precision medicine and surgical assistance, contributing to improved clinical outcomes and efficiency.

Asia Pacific is experiencing the fastest growth, attributed to rising healthcare expenditures, an aging population, and increasing prevalence of chronic diseases. China emerges as the dominating country in this region, driven by massive investments in AI infrastructure and partnerships with global tech firms, accelerating the adoption of computer vision for remote monitoring and large-scale diagnostic programs.

Latin America shows emerging potential, with growth supported by improving healthcare access and digital transformation efforts. Brazil leads as the dominating country, focusing on integrating computer vision in public health systems to address diagnostic shortages and enhance telemedicine capabilities in remote areas.

The Middle East and Africa region is gradually adopting these technologies, constrained by infrastructure challenges but boosted by international aid and investments in health tech. South Africa dominates here, utilizing computer vision to improve disease detection in underserved communities through mobile health solutions and partnerships with global organizations.

What are the Key Market Players and Strategies in Computer Vision in Healthcare?

- NVIDIA Corporation focuses on developing high-performance GPUs and AI platforms tailored for healthcare, such as the Clara suite, which supports medical imaging and genomics. Their strategy involves partnerships with healthcare providers and tech firms to integrate edge computing for real-time diagnostics, emphasizing scalability and precision to maintain market leadership.

- Intel Corporation emphasizes scalable hardware solutions like Xeon processors and Habana AI accelerators, optimized for healthcare workloads. Their approach includes collaborations for AI model training and deployment, prioritizing energy efficiency and data security to address integration challenges in diverse healthcare environments.

- Microsoft Corporation leverages Azure cloud services and AI tools for computer vision applications in healthcare, such as through the Microsoft Healthcare Bot. Their strategy centers on ecosystem building via open-source initiatives and regulatory compliance, aiming to enhance interoperability and drive adoption in patient monitoring and diagnostics.

- IBM Corporation utilizes Watson Health for AI-driven imaging analysis, focusing on oncology and cardiology. Their strategy involves data analytics integration and acquisitions to expand capabilities, emphasizing ethical AI and bias reduction to build trust and facilitate global market penetration.

- Google LLC advances through DeepMind Health and Google Cloud Healthcare API, applying machine learning to diagnostics and research. Their approach includes research collaborations and open datasets, prioritizing innovation in predictive analytics to improve outcomes in chronic disease management.

- Siemens Healthineers AG integrates computer vision into imaging systems like syngo.via, enhancing diagnostic workflows. Their strategy focuses on mergers and R&D investments, aiming for seamless integration with hospital systems to boost efficiency in radiology and surgery.

- GE HealthCare develops AI-enhanced ultrasound and MRI systems, such as the AIR Recon DL. Their strategy involves global partnerships and regulatory approvals, targeting cost reduction and accuracy in diagnostics to expand in emerging markets.

- Koninklijke Philips N.V. offers IntelliSpace AI Workflow Suite for imaging analysis. Their approach emphasizes connected care ecosystems and sustainability, driving growth through telehealth integrations and personalized medicine solutions.

- Stryker specializes in surgical visualization with computer vision in endoscopic systems. Their strategy includes acquisitions for robotics enhancement, focusing on minimally invasive procedures to improve surgical precision and patient recovery.

- Fujitsu Limited provides AI platforms for healthcare data analysis. Their strategy involves cross-industry collaborations, emphasizing privacy-compliant solutions to support drug discovery and remote monitoring in Asia Pacific markets.

What are the Computer Vision in Healthcare Market Trends?

- Integration of edge computing for real-time surgical intelligence and reduced latency in diagnostics.

- Adoption of generative AI for synthetic data creation and image reconstruction to address data scarcity.

- Proliferation of ambient intelligence for contactless patient monitoring and enhanced hospital management.

- Convergence with multimodal AI models combining vision with other data types for comprehensive analysis.

- Emphasis on ethical AI frameworks to mitigate biases in diverse patient populations.

- Expansion of telemedicine applications using computer vision for remote diagnostics and consultations.

- Increased focus on hyperspectral imaging for precise tissue analysis in oncology and wound care.

- Growth in wearable devices incorporating computer vision for continuous health tracking.

- Collaborations between startups and established firms to accelerate innovation in drug discovery.

- Regulatory advancements facilitating faster approvals for AI-enabled medical devices.

What are the Market Segments and their Subsegments Covered in the Computer Vision in Healthcare Report?

By Component

- Hardware

- Software

- Services

By Application

- Medical Imaging & Diagnostics

- Surgeries

- Clinical Trials

- Patient Management & Research

- Pathology & Laboratory Automation

- Hospital Management & Patient Monitoring

- Drug Discovery

- Remote Patient Monitoring

- Surgical Assistance

- Patient Identification

By End-User

- Hospitals & Clinics

- Diagnostic Centers

- Academic Research Institutes

- Healthcare Providers

- Ambulatory Surgical Centers

- Research Institutions

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Computer Vision in Healthcare Market - Industry Analysis

Chapter 4. Global Computer Vision in Healthcare Market- Competitive Landscape

Chapter 5. Global Computer Vision in Healthcare Market - Component Analysis

Chapter 6. Global Computer Vision in Healthcare Market - Application Analysis

Chapter 7. Global Computer Vision in Healthcare Market - End-User Analysis

Chapter 8. Computer Vision in Healthcare Market - Regional Analysis

Chapter 9. Company Profiles

Computer Vision in Healthcare refers to AI technologies that enable machines to interpret visual data from medical sources, such as images and videos, to assist in diagnostics, surgeries, and patient care. Key factors include advancements in AI algorithms, rising chronic disease prevalence, government funding for digital health, and increasing demand for automated diagnostic tools. The market is projected to grow from USD 3.5 billion in 2025 to USD 60 billion by 2035. The CAGR is expected to be 35% from 2026 to 2035. North America will contribute notably, holding approximately 37% share due to advanced infrastructure and high AI adoption. Major players include NVIDIA Corporation, Intel Corporation, Microsoft Corporation, IBM Corporation, and Google LLC. The report provides in-depth analysis of market size, trends, segments, key players, regional insights, and forecasts from 2026 to 2035. Stages include data acquisition through imaging devices, algorithm development and training, integration into healthcare systems, deployment in clinical settings, and ongoing maintenance and updates. Trends are shifting toward real-time AI integration and personalized diagnostics, with consumers preferring solutions that enhance accuracy, reduce costs, and ensure data privacy. Regulatory factors include FDA approvals for AI devices and data protection laws like GDPR, while environmental factors involve sustainable computing practices to minimize energy consumption in AI processing.Frequently Asked Questions