Coconut Water Market Size and Forecast 2026 to 2035

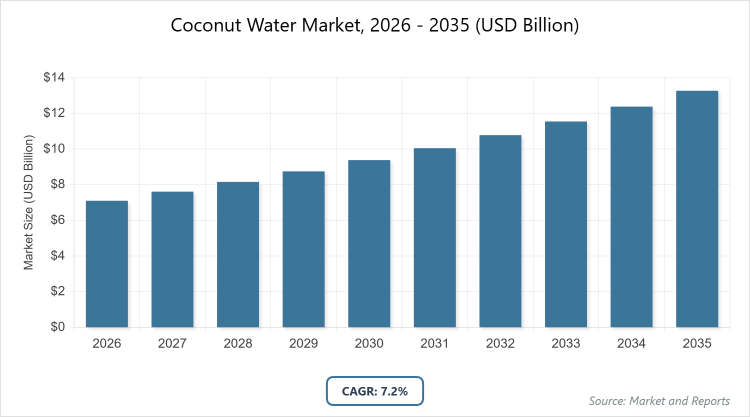

According to MarketnReports, the global Coconut Water market size was estimated at USD 7.1 billion in 2025 and is expected to reach USD 14.5 billion by 2035, growing at a CAGR of 7.2% from 2026 to 2035. Coconut Water Market is driven by the surging consumer shift toward natural, low-calorie hydration and plant-based functional beverages as healthy alternatives to sugary sodas and artificial sports drinks.

What are the Key Insights?

- Global coconut water market value in 2025: USD 7.1 billion.

- Projected global coconut water market value in 2035: USD 14.5 billion.

- CAGR for the global coconut water market from 2025 to 2035: 7.2%.

- Dominant subsegment in nature: Conventional with 92.6% revenue share.

- Dominant subsegment in flavor: Original/unflavored with 73% revenue share.

- Dominant subsegment in packaging: Tetra pack with over 50% revenue share.

- Dominant subsegment in distribution/sales channel: Supermarkets & hypermarkets with 48.0% revenue share.

- Dominant subsegment in application: Retail-pack hydration with 64% share.

- Dominant region: Asia Pacific with 33.1% revenue share.

What Is The Global Coconut Water Market?

The coconut water market encompasses the production, distribution, and consumption of a natural beverage extracted from young green coconuts, valued for its hydrating properties, rich electrolyte content including potassium, magnesium, and sodium, and low-calorie profile that positions it as a healthier alternative to sugary sodas and artificial sports drinks.

This market is part of the broader functional and plant-based beverage sector, appealing to health-conscious consumers, fitness enthusiasts, and those seeking natural hydration solutions amid rising wellness trends. It involves sourcing from coconut-producing regions, processing to retain nutritional integrity, and packaging in convenient formats for global retail, with a focus on clean-label attributes like organic certification and minimal processing to meet demands for transparency and sustainability in beverage choices.

What Are The Key Dynamics Of The Coconut Water Market?

Growth Drivers

The coconut water market is propelled by increasing consumer awareness of health and wellness, driving demand for natural, low-calorie beverages that offer superior hydration and electrolyte replenishment compared to traditional sugary drinks, as evidenced by scientific studies validating its efficacy in reducing fatigue and supporting post-workout recovery; this is further amplified by the fitness revolution among millennials and Gen Z, who prefer plant-based options, alongside innovations in flavored variants, functional infusions with vitamins, probiotics, and adaptogens, and the convenience of on-the-go packaging that aligns with urban lifestyles and e-commerce growth.

Restraints

Market growth faces hurdles from the higher pricing of organic and premium variants, which can limit accessibility for price-sensitive consumers in emerging economies, compounded by volatile raw material costs due to fluctuations in coconut yields influenced by weather patterns, fertilizer shortages, and export-led price shocks that have seen bulk prices rise significantly in recent years, alongside concerns over flavor degradation in packaged products and intense competition that squeezes profit margins for smaller players.

Opportunities

Opportunities abound in expanding into untapped geographic markets through e-commerce and direct-to-consumer channels, product diversification via infusions with fruits, plant proteins, and health-boosting additives to cater to niche demands like gut health and sports recovery, adoption of technological advancements such as blockchain for supply chain transparency and high-pressure processing for extended shelf life, collaborations with influencers and celebrities for targeted marketing, and leveraging data analytics to optimize inventory turnover and personalize offerings in high-growth segments like online retail and wellness-focused outlets.

Challenges

Challenges include supply chain vulnerabilities tied to coconut production in specific regions, leading to freight disruptions and cost escalations, maintaining product freshness and nutrient retention in packaged formats amid consumer skepticism, navigating regulatory pressures for sustainability and ethical sourcing, competing with a proliferation of flavored and functional alternatives that may dilute brand loyalty, and addressing margin pressures from dynamic pricing in retail channels while ensuring compliance with clean-label and organic certifications in diverse markets.

Coconut Water Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Coconut Water Market |

| Market Size 2025 | USD 7.1 Billion |

| Market Forecast 2035 | USD 14.5 Billion |

| Growth Rate | CAGR of 7.2% |

| Report Pages | 225 |

| Key Companies Covered |

PepsiCo, The Vita Coco Company Inc., The Coca-Cola Company, Harmless Harvest, Nestlé S.A., Goya Foods Inc., Malee Group PCL, and Wichy Plantation Company (Pvt) Ltd |

| Segments Covered | By Nature, By Flavor, By Packaging, By Distribution Channel, By Application, By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How Is The Coconut Water Market Segmented?

The Coconut Water market is segmented by nature, flavor, packaging, distribution channel, application, and region.

By Nature

The most dominant segment in nature is conventional coconut water, holding a substantial 92.6% revenue share due to its affordability and widespread availability through established supply chains in major producing countries, which lowers production costs and enables competitive pricing that appeals to a broad consumer base, thereby driving overall market expansion by making the product accessible to price-sensitive demographics in emerging markets and supporting high-volume sales in retail channels; the second most dominant is organic coconut water, with a 7.4% share, gaining traction from health-conscious consumers seeking pesticide-free and naturally sourced options, which commands premium pricing and fosters market growth through differentiation and alignment with wellness trends that encourage repeat purchases among urban millennials.

By Flavor

The most dominant segment in flavor is original/unflavored coconut water, capturing 73% of the market share owing to its authentic taste and perceived purity that resonates with consumers prioritizing natural hydration without added sugars or artificial flavors, positioning it as a core driver of market growth by serving as the entry point for new users and maintaining high loyalty rates in health-focused applications; the second most dominant is flavored coconut water, with 27% share, appealing to variety-seeking consumers through innovations like tropical fruit infusions that expand market reach into younger demographics and functional beverage categories, thereby boosting overall demand by enhancing palatability and encouraging trial in competitive retail environments.

By Packaging

The most dominant segment in packaging is tetra pack, accounting for 52.7% revenue share because of its ability to preserve nutrients, flavor, and freshness while being lightweight, recyclable, and cost-effective for transportation, which dominates by enabling widespread distribution and appealing to eco-conscious consumers, thus driving market growth through improved shelf life and convenience in high-volume channels; the second most dominant is cans, expected to grow rapidly due to their portability, recyclability, and protection from light and air, which helps expand the market by targeting on-the-go consumers and reducing shipping costs, fostering innovation in premium and sustainable offerings.

By Distribution/Sales Channel

The most dominant segment in distribution/sales channel is supermarkets & hypermarkets, with 48.0% revenue share attributed to their extensive reach, variety of options, competitive pricing, and impulse-buying opportunities that make them a primary access point for consumers, driving market growth by facilitating bulk purchases and brand visibility in everyday shopping; the second most dominant is direct channels (including gyms and food-service), holding 37.6% share, which excels through targeted contracts and personalized sales in wellness-oriented venues, propelling the market forward by capturing premium spend in niche applications like sports recovery and enhancing repeat cycles via subscriptions.

By Application

The most dominant segment in application is retail-pack hydration, comprising 64% share as it directly addresses consumer needs for convenient, ready-to-drink natural beverages in daily routines and fitness activities, dominating through high demand in RTD formats that drive volume sales and market penetration in health trends; the second most dominant is food applications (such as bakery and dairy), with smaller but growing shares, leveraging coconut water’s versatility as an ingredient to innovate in clean-label products, contributing to market expansion by diversifying usage beyond beverages and tapping into broader food industry trends.

What are the Recent Developments In Coconut Water Industry?

- In April 2023, ITC’s B Natural introduced packaged tender coconut water across India, capitalizing on rising hydration trends and consumer interest in natural beverages, which expanded market accessibility and aligned with wellness demands through convenient retail availability.

- In June 2022, Vita Coco launched Vita Coco Coconut Juice in new tropical flavors like Original with Pulp and Mango, aiming to attract diverse consumers while preserving core nutritional benefits, thereby enhancing product variety and market competitiveness.

What Is The Regional Analysis Of The Coconut Water Market?

North America to dominate the Coconut Water market

North America, led by the United States as the dominating country with an 18% global share, exhibits robust growth driven by health-conscious lifestyles, widespread retail infrastructure including chains like Walmart and Trader Joe’s, and high demand for organic and flavored variants influenced by social media and fitness trends, with the market projected to expand significantly through e-commerce penetration reaching 20% of volume and innovations in D2C subscriptions that shorten reorder cycles, while Canada and Mexico contribute through cross-border trade and growing awareness of natural hydration benefits.

Europe, with the United Kingdom dominating through its 11.7% CAGR and strong retail channels like supermarkets and health stores, is propelled by preferences for low-calorie, plant-based drinks amid sugar-tax regulations and clean-label demands, featuring rapid online sales growth at 16% and organic certifications boosting shelf turnover, while Germany and France follow closely with bio-certification emphasis, local bottling to reduce emissions, and partnerships in cafés and gyms that enhance market accessibility and sustainability focus.

Asia Pacific, dominated by Thailand and Indonesia due to extensive coconut production and cultural affinity for the beverage, holds the largest 33.1% revenue share, benefiting from low production costs, tourism-driven demand, and digitization improving inventory turnover, with countries like the Philippines and Vietnam supporting through export-oriented supply chains and innovations in sustainable packaging that hedge against price volatility, fostering regional leadership in volume and affordability.

Central & South America, led by Brazil as the key country, leverages local coconut resources and growing export capabilities to contribute to the market, with emphasis on natural product positioning in health trends and retail expansion, though facing challenges from supply fluctuations, while supporting global growth through affordable sourcing for international brands.

Middle East & Africa, with South Africa emerging as a dominant player, shows potential through increasing urbanization and demand for functional beverages, aided by retail modernization and health awareness, though limited by infrastructural constraints, positioning the region for gradual expansion via imports and local processing initiatives.

Who Are The Leading Coconut Water Market Players And Their Strategic Initiatives?

- PepsiCo employs strategies such as acquiring stakes in brands like O.N.E. Coconut Water, leveraging extensive distribution networks for functional variants, and forming partnerships with processors in the Philippines and Indonesia to ensure supply chain reliability, while focusing on cross-category bundling with low-calorie products to capture premium market segments.

- The Vita Coco Company, Inc. emphasizes sustainability through high-quality, environmentally friendly sourcing, diversifies with flavored and protein-infused offerings, and utilizes influencer collaborations and digital marketing to target eco-conscious and fitness-oriented consumers, enhancing brand loyalty via online retail expansion.

- The Coca-Cola Company repositions brands like ZICO with added-electrolyte SKUs, intensifies D2C and quick-commerce efforts, and invests in e-commerce bundling to broaden accessibility, while prioritizing functional extensions to align with health trends and competitive positioning.

- Harmless Harvest focuses on sustainable practices and ethical sourcing to appeal to premium consumers, incorporating clean labels and organic certifications, and expands through collaborations with retailers and influencers to drive transparency and trust in the market.

- Nestlé S.A. expands into hydration under brands like Pure Life, targeting regional markets with plant-based innovations and leveraging global distribution for premium chilled products, while emphasizing private-label strategies to undercut competition.

- Goya Foods, Inc. penetrates ethnic and value-tier markets with shelf-stable options, utilizing robust retail presence in the U.S. to offer affordable products, and adopts dynamic pricing to maintain competitiveness in diverse channels.

- Malee Group PCL concentrates on sustainable sourcing in APAC, innovates with plant-based extensions, and builds regional partnerships to enhance export capabilities, focusing on traceability for premium positioning.

- Wichy Plantation Company (Pvt) Ltd specializes in organic concentrates for export to Europe and Japan, employing fair-trade practices and eco-friendly packaging to differentiate in high-value markets, while optimizing supply chains for cost efficiency.

What Are The Key Trends In The Coconut Water Market?

- Increasing focus on functional blends incorporating electrolytes, adaptogens, probiotics, and plant proteins for enhanced recovery, gut health, and performance benefits.

- Adoption of sustainable packaging solutions like recyclable Tetra Pak, aluminum cans, and reusable pods to meet eco-conscious consumer demands and regulatory requirements.

- Rise of digital traceability tools such as QR codes and blockchain for supply chain transparency, building trust in sourcing and freshness.

- Growth in subscription models and D2C channels, shortening repeat-purchase cycles and capturing premium spend in urban and fitness segments.

- Premiumization through clean labels, organic certifications, and limited-edition flavors targeted via social media and micro-influencer campaigns.

- Shift toward shelf efficiency with dynamic pricing, cold-shelf allocation, and faster SKU turnover in retail formats.

- Integration of scientific validation for hydration efficacy, positioning coconut water as equivalent to sports drinks in wellness and athletic applications.

What Market Segments are Covered in the Coconut Water Report?

By Nature

- Conventional

- Organic

By Flavor

- Original/Unflavored

- Flavored

By Packaging

- Tetra Pack

- Cans

- Plastic Bottle

- Pouches

- Glass

By Distribution/Sales Channel

- Supermarkets & Hypermarkets

- Online

- Convenience Stores

- Direct (e.g. Gyms, Food-Service)

- Indirect (Modern Trade, Grocery, Discount Chains)

By Application

- Retail-Pack Hydration

- Food (Bakery, Dairy, Cereals, Sauces)

- Beverages (Alcoholic Mixes, Tea/Coffee)

- Personal Care & Cosmetics

- Nutraceutical

- Animal Feed

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Coconut water is a clear, natural liquid extracted from young green coconuts, known for its hydrating properties due to high electrolyte content like potassium and magnesium, serving as a low-calorie, plant-based alternative to sugary beverages and sports drinks, often consumed for health benefits such as fatigue reduction and post-exercise recovery.

Key factors include rising health consciousness driving demand for natural hydration, innovations in functional blends with probiotics and adaptogens, expansion of e-commerce and D2C channels, sustainable packaging adoption, supply chain transparency via blockchain, and regional production advantages in Asia Pacific, tempered by raw material price volatility and competitive pressures.

The market is projected to grow from approximately USD 7.61 billion in 2025 to USD 14.5 billion by 2035, reflecting steady expansion driven by consumer trends and product innovations.

The CAGR is expected to be 7.2%, supported by increasing demand for functional beverages and market penetration in emerging regions.

Asia Pacific will contribute notably, holding the largest share due to abundant coconut production in countries like Thailand and Indonesia, low costs, and high local consumption.

Major players include PepsiCo, The Vita Coco Company, Inc., The Coca-Cola Company, Harmless Harvest, Nestlé S.A., Goya Foods, Inc., Malee Group PCL, and Wichy Plantation Company (Pvt) Ltd, who drive growth through innovations, sustainable sourcing, and expanded distribution.

The report provides comprehensive insights into market size, growth forecasts, segmentation analysis, dynamics including drivers and challenges, regional breakdowns, key player strategies, trends, and value chain details, offering actionable data for stakeholders.

The value chain includes raw material sourcing from coconut farms, processing and extraction to retain nutrients, packaging in formats like Tetra Pak for preservation, distribution through wholesalers and retailers, and end-consumer marketing via digital and influencer channels, with emphasis on traceability and sustainability checkpoints.

Trends are evolving toward functional infusions, sustainable packaging, digital traceability, and premiumization, while consumer preferences shift to clean-label, organic options, on-the-go convenience, and scientifically backed hydration benefits, influenced by wellness and eco-awareness.

Regulatory factors include sugar taxes promoting low-calorie alternatives and organic certification standards, while environmental factors involve sustainable sourcing mandates, recyclable packaging requirements, and climate impacts on coconut yields, influencing growth through compliance costs and innovation incentives.