CNC Machine Market Size, Share and Trends 2026 to 2035

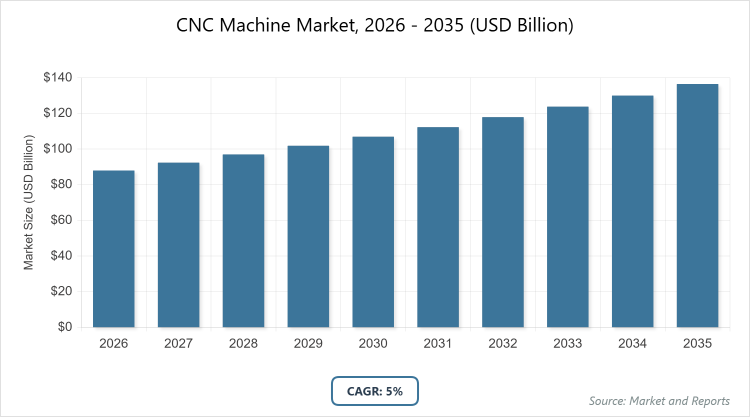

According to MarketnReports, the global CNC Machine market size was estimated at USD 88 billion in 2025 and is expected to reach USD 143 billion by 2035, growing at a CAGR of 5% from 2026 to 2035. The CNC Machine Market is driven by increasing industrial automation, adoption of Industry 4.0 technologies, and rising demand for precision manufacturing in the automotive, aerospace, and electronics sectors.

What are the Key Insights into CNC Machine?

- The global CNC Machine market was valued at USD 88 billion in 2025 and is projected to reach USD 143 billion by 2035.

- The market is expected to grow at a CAGR of 5% during the forecast period from 2026 to 2035.

- The market is driven by surging automation adoption, Industry 4.0 integration, precision requirements in key sectors, and advancements in multi-axis and smart machining.

- In the product type segment, milling machines dominate with a 35% share due to their versatility in complex geometries and material handling across automotive and aerospace applications.

- In the application segment, metal cutting dominates with a 45% share as it supports core precision removal processes essential for high-volume, high-quality component production.

- In the end-user segment, automotive dominates with a 30% share driven by extensive needs for consistent, scalable parts in traditional and EV manufacturing.

- Asia Pacific dominates the regional market with a 40% share, propelled by massive manufacturing hubs in China, government-backed smart factory initiatives, and cost advantages in high-volume production.

What is the Industry Overview of CNC Machine?

The CNC Machine market encompasses computer numerical control systems that automate precise machining operations through programmed software, enabling the production of complex parts with high accuracy, repeatability, and efficiency across diverse materials. Market definition includes a broad array of equipment such as lathes, mills, grinders, lasers, and multi-axis centers that interpret digital instructions to control tools and machinery, minimizing manual intervention, reducing errors, and supporting scalable manufacturing in industries requiring tight tolerances and customization.

What are the Market Dynamics of CNC Machine?

Growth Drivers

Growth in the CNC Machine market is primarily fueled by widespread industrial automation trends that boost productivity, cut labor costs, and ensure consistent quality in mass production environments. The push toward Industry 4.0, incorporating IoT, AI for predictive maintenance, and connected smart factories, accelerates demand for advanced CNC systems capable of real-time optimization. Expanding sectors like electric vehicles, aerospace, and renewable energy require intricate, lightweight components with tight tolerances, while reshoring initiatives in developed markets drive investments in domestic high-precision capabilities to enhance supply chain resilience and reduce lead times.

Restraints

High upfront costs for sophisticated multi-axis and hybrid CNC machines limit adoption, especially among SMEs in developing regions where budget constraints favor manual or basic alternatives. Shortages of skilled operators and programmers for CNC setup, maintenance, and software management create operational bottlenecks. Cybersecurity vulnerabilities in networked CNC systems raise risks of production halts, while supply chain fluctuations for key components like controllers and spindles lead to delays and increased costs. Regulatory compliance in high-stakes industries such as aerospace adds layers of certification and testing expenses.

Opportunities

Emerging opportunities lie in hybrid additive-subtractive CNC systems that combine 3D printing with traditional machining for innovative, lightweight designs in aerospace and medical fields. Government incentives in emerging markets for manufacturing upgrades and EV/electronics growth open new avenues for market penetration. Aftermarket retrofitting of older machines with modern IoT controls and AI features offers recurring revenue, while partnerships between CNC providers and software firms speed up Industry 4.0 transitions. Demand for energy-efficient, sustainable machining solutions aligns with global green manufacturing goals.

Challenges

Fierce price competition from low-cost Asian suppliers pressures margins for premium brands, necessitating continuous innovation. Rapid technological evolution risks obsolescence, demanding heavy ongoing R&D spending. Talent shortages in digital machining skills slow adoption in many areas, and geopolitical issues disrupt critical supply chains for semiconductors and precision parts. Stricter environmental regulations on energy use and emissions force redesigns of machines and processes, increasing development complexity.

CNC Machine Market: Report Scope

| Report Attributes | Report Details |

| Report Name | CNC Machine Market |

| Market Size 2025 | USD 88 Billion |

| Market Forecast 2035 | USD 143 Billion |

| Growth Rate | CAGR of 5% |

| Report Pages | 220 |

| Key Companies Covered | Yamazaki Mazak Corporation, DMG Mori Co., Ltd., Haas Automation, Inc., FANUC Corporation, Okuma Corporation, JTEKT Corporation, Makino, Siemens AG, and Others |

| Segments Covered | By Product Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of CNC Machine?

The CNC Machine market is segmented by product type, application, end-user, and region.

By Product Type. Milling machines are the most dominant subsegment, securing around 35% market share, thanks to their broad capability in multi-operation tasks like contouring and complex part creation across various materials. This dominance propels overall market growth by addressing needs in diverse industries for efficient, flexible machining that reduces setup times and enhances productivity. Machining centers are the second most dominant, with about 25% share, providing integrated multi-process capabilities in a single setup, driving expansion through high-automation suitability for medium-to-high-mix production in automotive and precision sectors.

By Application. Metal cutting is the most dominant subsegment, holding approximately 45% share, as it forms the foundation for accurate material removal in demanding alloys and components vital for performance-critical applications. This leads market advancement by enabling scalable, high-quality output in core manufacturing processes. Precision engineering ranks second most dominant, with roughly 20% share, emphasizing micron-level accuracy for intricate parts in electronics and medical devices, fueling growth through rising needs for customization and reliability in advanced technologies.

By End-User. Automotive stands as the most dominant subsegment, accounting for about 30% share, supported by requirements for precise, repeatable parts in engines, transmissions, and emerging EV components. This dominance accelerates market progress via large-scale investments and seamless integration into production lines. Aerospace & defense is the second most dominant, with around 20% share, due to rigorous demands for complex geometries in turbine and structural elements, contributing to growth through premium, high-value contracts and adoption of advanced multi-axis technologies.

What are the Recent Developments in CNC Machine?

- In December 2024, Yamazaki Mazak opened a new European facility dedicated to multi-tasking CNC machines, improving regional supply and shortening delivery times for key clients in automotive and aerospace.

- In September 2024, Haas Automation revealed plans for expanded U.S. production in Nevada, incorporating smart factory features to ramp up vertical machining center output in response to reshoring demands.

- In July 2024, DMG Mori released an innovative hybrid CNC platform merging additive manufacturing with subtractive processes, aimed at aerospace lightweight component fabrication.

- In March 2025, Okuma Corporation debuted an AI-powered CNC controller featuring real-time adaptive machining, boosting efficiency and minimizing tool wear in precision applications.

- In January 2025, FANUC formed a collaboration with NVIDIA to embed edge AI into CNC systems, supporting predictive maintenance and optimized toolpath generation for industrial operations.

What is the Regional Analysis of CNC Machine?

- Asia Pacific to dominate the global market.

Asia Pacific holds the largest share at around 40%, with China as the dominating country due to its unparalleled manufacturing scale, massive investments in smart factories under initiatives like Made in China 2025, and dominance in automotive, electronics, and machinery production. The region’s growth is fueled by low-cost production advantages, rapid industrialization in India and Southeast Asia, strong supply chains, and increasing adoption of advanced multi-axis CNC for EV and semiconductor components, positioning it as the epicenter of global CNC demand and innovation. Government subsidies, tax incentives, and large-scale infrastructure projects continue to attract foreign CNC manufacturers to establish local production facilities, further strengthening domestic capabilities.

North America follows closely, driven by technological leadership and reshoring efforts, where the United States dominates through advanced aerospace, defense, and automotive sectors supported by companies like Haas and robust R&D ecosystems. Growth stems from incentives for domestic manufacturing, high-precision requirements, and integration of AI/IoT in CNC operations, though tempered by higher labor and energy costs. Federal and state-level grants, tax credits, and the CHIPS Act are stimulating investments in next-generation CNC facilities focused on semiconductors and defense applications. Strong university-industry collaborations foster continuous innovation in CNC software, controls, and hybrid machining technologies.

Europe exhibits strong performance with emphasis on quality and sustainability, led by Germany through its engineering prowess, automotive giants, and firms like DMG Mori and Siemens. The region’s expansion benefits from Industry 4.0 policies, stringent precision standards in aerospace and machinery, and a focus on energy-efficient CNC solutions amid green manufacturing transitions. EU funding programs such as Horizon Europe and the Green Deal are channeling significant resources into research on low-emission machining processes and circular economy-compatible CNC equipment. Germany’s dual education system and apprenticeship programs produce highly skilled technicians who excel in operating and maintaining complex multi-axis systems.

Latin America shows steady but moderate advancement, dominated by Brazil’s industrial base in automotive and agricultural machinery, supported by growing investments in modernization,n though limited by economic fluctuations and infrastructure gaps. Countries like Mexico benefit from nearshoring trends as U.S. companies relocate production closer to home, boosting demand for reliable CNC equipment in automotive and electronics assembly plants. Government industrial development plans in Brazil and Argentina are offering financing schemes and import duty reductions to encourage local adoption of modern CNC technology.

The Middle East and Africa remain emerging, with the United Arab Emirates and South Africa leading through investments in oil & gas equipment, aerospace diversification, and basic manufacturing upgrades, constrained by lower industrialization levels but showing potential via infrastructure projects and technology transfers. Saudi Arabia’s Vision 2030 and the UAE’s industrial diversification strategies are funding new manufacturing zones equipped with state-of-the-art CNC capabilities to support non-oil sectors. South Africa’s established mining and automotive industries are gradually upgrading legacy equipment with modern CNC lathes and machining centers to improve component quality and reduce downtime.

What are the Key Market Players in CNC Machine?

- Yamazaki Mazak Corporation. Yamazaki Mazak focuses on multi-tasking and 5-axis CNC solutions with a strong emphasis on smart manufacturing integration, leveraging global facilities and partnerships to serve the automotive and aerospace sectors effectively.

- DMG Mori Co., Ltd. DMG Mori excels in hybrid additive-subtractive machines and digital twins, investing heavily in automation and sustainability to maintain leadership in precision engineering for high-value industries.

- Haas Automation, Inc. Haas Automation prioritizes affordable, reliable vertical and horizontal machining centers with user-friendly controls, targeting SMEs and job shops through extensive U.S. production and service networks.

- FANUC Corporation. FANUC specializes in CNC controllers and robotics integration, offering high-reliability systems with AI enhancements for predictive capabilities across diverse manufacturing applications.

- Okuma Corporation. Okuma emphasizes durable, high-precision lathes and machining centers with advanced thermal compensation, focusing on energy efficiency and long-term performance in demanding environments.

- JTEKT Corporation. JTEKT delivers robust grinding and turning solutions, leveraging automotive expertise for precision components while expanding into EV-related machining technologies.

- Makino. Makino targets high-speed milling and EDM for aerospace and die/mold industries, prioritizing micron-level accuracy and reduced cycle times through innovative spindle designs.

- Siemens AG. Siemens provides comprehensive CNC software and hardware ecosystems, integrating Sinumerik controls with digital services for seamless Industry 4.0 connectivity.

What are the Market Trends in CNC Machine?

- Increasing adoption of 5-axis and multi-axis machines for complex part production.

- Integration of AI and machine learning for adaptive machining and predictive maintenance.

- Rise of hybrid CNC systems combining additive and subtractive processes.

- Growing emphasis on sustainable, energy-efficient CNC designs.

- Expansion of IoT-enabled smart factories for real-time monitoring.

- Shift toward software-centric solutions with cloud-based controls.

- Demand for compact, desktop CNC for prototyping and education.

What Market Segments and Subsegments are Covered in the CNC Machine Report?

By Product Type

- Lathe Machines

- Milling Machines

- Laser Machines

- Grinding Machines

- Drilling Machines

- Welding Machines

- Machining Centers

- Routing Machines

- EDM Machines

- Multi-Axis Machines

- Others

By Application

- Metal Cutting

- Metal Forming

- Precision Engineering

- Automotive Parts Manufacturing

- Aerospace Component Production

- Electronics Fabrication

- General Machinery

- Others

By End-User

- Automotive

- Aerospace & Defense

- Industrial Machinery

- Construction Equipment

- Power & Energy

- Electronics

- Healthcare

- Metals & Mining

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

CNC Machines are computer-controlled tools that automate precise machining processes like cutting, drilling, and milling based on programmed instructions, ensuring high accuracy and repeatability in manufacturing.

Key factors include accelerated automation, Industry 4.0 adoption, demand for precision in EV/aerospace, AI integration, and government support for smart manufacturing in emerging economies.

The market is projected to grow from USD 88 billion in 2025 to USD 143 billion by 2035.

The CAGR is expected to be 5%.

Asia Pacific will contribute notably, holding around 40% share due to dominant manufacturing hubs in China and rapid industrialization.

Major players include Yamazaki Mazak Corporation, DMG Mori, Haas Automation, FANUC Corporation, Okuma Corporation, JTEKT Corporation, Makino, and Siemens AG.

The report delivers in-depth analysis of market size, trends, segmentation, regional insights, competitive landscape, and forecasts.

Stages encompass raw material sourcing (electronics, metals), component manufacturing (spindles, controllers), machine assembly, software development, distribution, installation, and aftermarket services.

Trends shift toward multi-axis, AI-integrated, and sustainable machines, with preferences for smart connectivity, energy efficiency, and hybrid capabilities.

Environmental regulations promote energy-efficient designs and reduced emissions, while safety standards and data security rules for connected systems influence adoption and compliance costs.