Brake Disc Market Size, Share and Trends 2026 to 2035

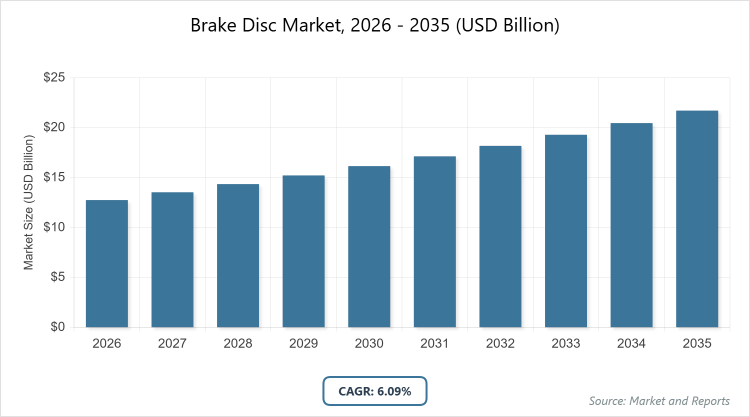

According to MarketnReports, the global Brake Disc market size was estimated at USD 12.75 billion in 2025 and is expected to reach USD 23.04 billion by 2035, growing at a CAGR of 6.09% from 2026 to 2035. Brake Disc Market is driven by increasing vehicle production, stringent safety regulations, and rising adoption of electric vehicles.

What is the overview of the Brake Disc industry?

The Brake Disc market involves the production and distribution of braking components that utilize friction to slow or stop vehicles by converting kinetic energy into heat. This market includes various materials and designs tailored for different vehicle types, ensuring safety and performance in automotive applications. Market definition encompasses the rotors or discs used in disc brake systems, which are integral to modern vehicles for effective stopping power, heat dissipation, and durability, supporting advancements in automotive safety and efficiency across passenger, commercial, and electric vehicles.

What are the key insights into the Brake Disc market?

- The global Brake Disc market was valued at USD 12.75 billion in 2025 and is projected to reach USD 23.04 billion by 2035.

- The market is expected to grow at a CAGR of 6.09% during the forecast period from 2026 to 2035.

- The market is driven by increasing vehicle production, stringent safety regulations, advancements in braking technologies, and rising adoption of electric and hybrid vehicles.

- In the material segment, Cast Iron dominates with a 54% share due to its cost-effectiveness, durability, and excellent heat dissipation properties.

- In the vehicle type segment, Passenger Cars holds the largest share at approximately 60% because of high global sales volumes and mandatory safety standards requiring advanced braking systems.

- In the sales channel segment, OEM dominates with around 76% share owing to integration in new vehicle manufacturing and partnerships with automakers.

- Asia Pacific dominates the global market with a 40% share, driven by massive automotive manufacturing hubs in China and India, high vehicle production, and growing exports.

What are the market dynamics in the Brake Disc industry?

Growth Drivers

The Brake Disc market is propelled by the surge in global vehicle production, particularly in emerging economies, where rising disposable incomes and urbanization drive demand for personal and commercial transportation. Stringent government regulations mandating advanced safety features, such as anti-lock braking systems (ABS) and electronic stability control (ESC), necessitate high-performance disc brakes. The rapid adoption of electric vehicles (EVs) requires specialized discs compatible with regenerative braking, further accelerating growth. Technological innovations, including lightweight materials and corrosion-resistant coatings, enhance product efficiency and appeal to eco-conscious consumers.

Restraints

High manufacturing costs for advanced materials like carbon ceramic limit adoption in budget vehicles, restraining market penetration in price-sensitive regions. Volatility in raw material prices, such as iron and steel, impacts profitability and supply chain stability. Intense competition from alternative braking technologies and counterfeit products erodes market share for established players. Regulatory variations across countries complicate compliance and increase operational expenses.

Opportunities

Opportunities abound in the development of lightweight and eco-friendly brake discs to meet the demands of fuel-efficient and electric vehicles. Expansion into aftermarket segments through e-commerce and customized solutions can tap into aging vehicle fleets. Collaborations with EV manufacturers for integrated braking systems present growth avenues. Emerging markets in Latin America and Africa offer untapped potential with improving infrastructure and rising vehicle ownership.

Challenges

Challenges include addressing thermal management in high-performance applications to prevent brake fade under extreme conditions. Supply chain disruptions from geopolitical tensions affect material availability. Ensuring compatibility with autonomous driving technologies requires ongoing R&D investment. Environmental concerns over brake dust emissions push for sustainable innovations, adding complexity to product development.

Brake Disc Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Brake Disc Market |

| Market Size 2025 | USD 12.75 Billion |

| Market Forecast 2035 | USD 23.04 Billion |

| Growth Rate | CAGR of 6.09% |

| Report Pages | 220 |

| Key Companies Covered |

Brembo S.p.A., Robert Bosch GmbH, Continental AG, Akebono Brake Industry Co., Ltd., ZF Friedrichshafen AG, Aisin Seiki Co., Ltd., Mando Corporation, Nissin Kogyo Co., Ltd., Federal-Mogul Holdings LLC, Knorr-Bremse AG, and Others |

| Segments Covered | By Material, By Vehicle Type, By Sales Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Brake Disc market segmented?

The Brake Disc market is segmented by material, vehicle type, sales channel, and region.

Based on Material Segment, Cast Iron is the most dominant subsegment, followed by Carbon Ceramic. Cast Iron’s dominance arises from its affordability, robustness, and superior thermal conductivity, which drives the market by enabling mass production for a wide range of vehicles and ensuring reliable performance in everyday driving conditions. Carbon Ceramic ranks second due to its lightweight nature and resistance to heat fade, contributing to market growth by catering to high-end and performance vehicles where reduced weight improves fuel efficiency and handling.

Based on Vehicle Type Segment, Passenger Cars is the most dominant, followed by Light Commercial Vehicles. Passenger Cars lead because of their vast global fleet and regulatory emphasis on safety, propelling market expansion through high demand for standardized disc brakes that enhance vehicle control and reduce accident risks. Light Commercial Vehicles are second as they require durable brakes for frequent stops in urban delivery, supporting growth by addressing the e-commerce boom and logistics needs.

Based on Sales Channel Segment, OEM is the most dominant, followed by Aftermarket. OEM dominates due to direct integration in vehicle assembly lines, driving the market by ensuring quality compliance and fostering long-term supplier relationships with automakers. Aftermarket is second, providing replacement options for vehicle maintenance, which boosts growth through extended vehicle lifespans and consumer preferences for upgraded performance parts.

What are the recent developments in the Brake Disc market?

- In March 2025, GSF Car Parts expanded its Brembo braking product lineup from 400 to 1,700 product lines, enhancing its position in the automotive aftermarket by leveraging Brembo’s reputation for high-quality components.

- In March 2025, TRP announced the launch of its new hydraulic disc brakes, EVO PRO and EVO X, aimed at improving performance in various cycling and automotive applications.

- In May 2025, Ford Motor Company unveiled an upgraded blended braking system for its 2025 Mustang Mach-E, seamlessly merging regenerative and friction braking for enhanced efficiency in electric vehicles.

- In January 2025, ZF North America introduced a next-generation disc brake platform tailored for electric and hybrid vehicles, focusing on improved responsiveness and integration with advanced systems.

- In February 2025, Brembo North America launched its Sensify smart braking platform, combining hydraulic braking with AI-enabled digital control for customized brake force application.

How does regional analysis impact the Brake Disc market?

- Asia Pacific to dominate the global market

Asia Pacific commands the largest share in the Brake Disc market, fueled by explosive automotive production, rapid urbanization, and increasing vehicle exports. China dominates within the region as the world’s largest vehicle manufacturer, with massive investments in EV infrastructure and stringent emission standards driving demand for advanced discs. India contributes significantly through growing domestic sales and government initiatives for road safety, while Japan and South Korea excel in technological innovations and high-quality exports.

North America maintains a strong position, supported by robust regulatory frameworks for vehicle safety and high adoption of premium vehicles. The United States leads with extensive R&D in autonomous and electric vehicles, where advanced brake systems are crucial, bolstered by NHTSA mandates for emergency braking. Canada follows with increasing focus on sustainable mobility and cold-weather performance testing.

Europe exhibits steady growth, driven by stringent EU safety regulations and a shift toward electrification. Germany dominates due to its automotive giants like BMW and Volkswagen, emphasizing high-performance braking for luxury and sports cars. The UK and France contribute through innovations in lightweight materials and collaborative R&D in green technologies.

Latin America shows emerging potential, with improving economic conditions and rising vehicle ownership. Brazil leads with growing automotive assembly plants and demand for affordable braking solutions, while Mexico benefits from NAFTA-related exports and investments in manufacturing.

The Middle East and Africa face gradual expansion, constrained by infrastructure but boosted by oil-rich economies investing in luxury vehicles. South Africa dominates with better automotive facilities, and Saudi Arabia advances through Vision 2030’s focus on diversification and modern transportation.

Who are the key market players in the Brake Disc industry and their strategies?

Brembo S.p.A. emphasizes innovation and expansion, launching advanced products like the Sensify platform and DYATOM discs while partnering with automakers for high-performance applications to strengthen its premium market position.

Robert Bosch GmbH focuses on integrating smart technologies, developing AI-enabled braking systems and expanding EV-compatible discs to enhance safety and efficiency across global markets.

Continental AG pursues sustainability through lightweight materials and regenerative braking solutions, investing in R&D for autonomous vehicles to capture emerging opportunities.

Akebono Brake Industry Co., Ltd. prioritizes aftermarket growth, introducing new pad lines for specific models and leveraging cost-effective manufacturing for broad accessibility.

ZF Friedrichshafen AG advances through acquisitions and tech integrations, launching platforms for EVs and collaborating on air disc brakes for commercial vehicles.

Aisin Seiki Co., Ltd. invests in material advancements, focusing on ceramic composites for reduced weight and improved durability in passenger cars.

Mando Corporation expands globally via OEM partnerships, developing high-friction discs for hybrid vehicles to meet regulatory demands.

Nissin Kogyo Co., Ltd. specializes in motorcycle and automotive brakes, innovating with drilled and slotted designs for enhanced heat dissipation.

Federal-Mogul Holdings LLC targets aftermarket with diverse product ranges, emphasizing eco-friendly, low-dust formulations to appeal to environmentally conscious consumers.

Knorr-Bremse AG focuses on commercial vehicles, introducing advanced systems for heavy-duty applications to improve fleet safety and efficiency.

What are the market trends in the Brake Disc industry?

- Rising adoption of carbon ceramic discs for high-performance and electric vehicles due to superior heat resistance and lightweight properties.

- Integration of advanced driver-assistance systems (ADAS) requiring precise and responsive braking technologies.

- Shift toward eco-friendly materials to reduce brake dust emissions and comply with environmental regulations.

- Growth in aftermarket sales driven by vehicle aging and consumer demand for upgrades.

- Development of regenerative-compatible discs for EVs to optimize energy recovery.

- Emphasis on corrosion-resistant coatings for enhanced durability in diverse climates.

- Increasing use of 3D printing for customized and rapid prototyping of discs.

- Focus on noise reduction technologies to improve driving comfort.

What are the market segments and their subsegments covered in the Brake Disc report?

By Material

-

- Cast Iron

- Carbon Ceramic

- Stainless Steel

- Aluminum

- Composite

- Ceramic Coated

- Vented Cast Iron

- Drilled Cast Iron

- Slotted Cast Iron

- High Carbon Steel

- Others

By Vehicle Type

-

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Two-Wheelers

- SUVs

- Hatchbacks/Sedans

- Electric Vehicles

- Hybrid Vehicles

- Luxury Vehicles

- Sports Cars

- Others

By Sales Channel

-

- OEM

- Aftermarket

- Online Sales

- Retail Stores

- Distributors

- Wholesalers

- Direct Sales

- E-commerce Platforms

- Automotive Parts Suppliers

- Service Centers

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Brake Disc Market - Industry Analysis

Chapter 4. Global Brake Disc Market- Competitive Landscape

Chapter 5. Global Brake Disc Market - Material Analysis

Chapter 6. Global Brake Disc Market - Vehicle Type Analysis

Chapter 7. Global Brake Disc Market - Sales Channel Analysis

Chapter 8. Brake Disc Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Brake Disc refers to the rotating component in a disc brake system that, when clamped by calipers, generates friction to slow or stop a vehicle.

Key factors include rising vehicle production, stringent safety regulations, technological advancements in materials, and increasing adoption of electric vehicles.

The market is projected to grow from USD 12.75 billion in 2025 to USD 23.04 billion by 2035.

The market is expected to grow at a CAGR of 6.09% from 2026 to 2035.

Asia Pacific will contribute notably, holding the largest share due to high vehicle production and manufacturing hubs.

Major players include Brembo S.p.A., Robert Bosch GmbH, Continental AG, Akebono Brake Industry Co., Ltd., and ZF Friedrichshafen AG.

The report provides comprehensive analysis including market size, trends, segments, regional insights, key players, and forecasts.

Stages include raw material sourcing, manufacturing of discs, assembly into brake systems, distribution to OEMs and aftermarket, and end-use in vehicles.

Trends show a preference for lightweight, eco-friendly discs with low emissions, alongside demand for performance-enhancing features in EVs and premium vehicles.

Stringent safety standards like ABS mandates and environmental regulations on brake dust and materials drive innovation and compliance costs.