Boron Carbide Market Size, Share and Trends 2026 to 2035

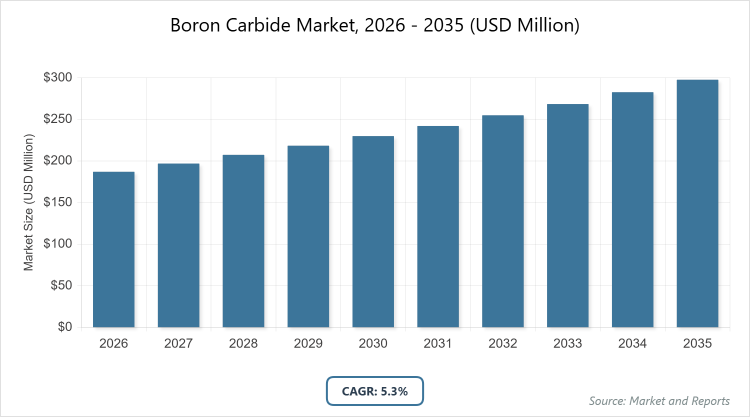

The global Boron Carbide Market size was estimated at USD 187 Million in 2025 and is expected to reach USD 298.4 Million by 2035, growing at a CAGR of 5.3% from 2026 to 2035. The Boron Carbide market is primarily driven by the increasing global demand for lightweight, high-hardness materials in defense armor systems and neutron-absorbing components for the expanding nuclear power sector.

Boron Carbide Market- Key Insights

- The global Boron Carbide Market is projected to reach approximately USD 298.4 million by 2035, growing from an estimated USD 187 million in 2026.

- The market is anticipated to exhibit a CAGR of 5.3% during the forecast period from 2026 to 2035.

- The abrasive grade dominates the grade segmentation, accounting for over 67% market share, due to its widespread use in industrial grinding and polishing applications.

- Powder form leads the type segmentation with around 60% share, valued for its versatility in abrasives, nuclear shielding, and manufacturing processes.

- Industrial applications, particularly in mining and metallurgy, hold the largest share at about 28%, driven by demand for wear-resistant tools and coatings.

- Asia-Pacific emerges as the dominant region, contributing nearly 46% of the global market, fueled by rapid industrialization and nuclear expansions.

Industry Overview

The Boron Carbide Market encompasses a highly specialized sector focused on the production, distribution, and application of boron carbide (B4C), a synthetic ceramic material renowned for its exceptional hardness, ranking third after diamond and cubic boron nitride. This market serves industries requiring materials with superior wear resistance, low density, high melting point, and neutron absorption capabilities, enabling its use in abrasive tools for grinding and polishing, protective armor for defense purposes, shielding components in nuclear reactors to control radiation, and refractory linings in high-temperature industrial processes.

The market thrives on the material’s chemical inertness and thermal stability, which make it indispensable in precision engineering, where it facilitates efficient machining of hard substances like ceramics and metals, while also supporting advancements in lightweight composites for aerospace and automotive sectors. Overall, the Boron Carbide Market represents a niche yet critical segment of the advanced materials industry, bridging traditional manufacturing with cutting-edge technologies in energy, security, and high-performance applications.

What are the Market Dynamics?

Growth Drivers

The growth of the Boron Carbide Market is primarily propelled by escalating demand in the defense sector for lightweight body armor, vehicle protection, and helmets, where its superior hardness and low density enhance soldier safety and mobility without compromising performance; additionally, the expansion of nuclear power generation worldwide, especially in emerging economies, drives adoption for neutron-absorbing control rods and shielding materials to ensure reactor safety and efficiency; industrial applications further fuel growth through its use in abrasives for grinding, lapping, and polishing in manufacturing processes, supported by rapid industrialization in Asia-Pacific regions; moreover, innovations in aerospace and automotive industries leverage its wear-resistant properties for components like brake pads and nozzles, aligning with trends toward fuel efficiency and durability; finally, emerging uses in renewable energy systems, such as solar panel production and advanced batteries, along with 3D printing for customized parts, contribute to sustained market expansion by opening new avenues for high-purity boron carbide in sustainable technologies.

Restraints

The Boron Carbide Market faces significant restraints due to its high production costs stemming from energy-intensive manufacturing processes like carbothermic reduction in electric arc furnaces, which require temperatures exceeding 2000°C and lead to elevated pricing that limits adoption in cost-sensitive industries such as automotive and mining; volatility in raw material prices, particularly for boric acid and carbon sources, exacerbates this issue, often influenced by geopolitical tensions and supply chain disruptions; the availability of cheaper substitutes like silicon carbide or aluminum oxide for non-specialized abrasive applications further hampers growth by diverting demand in mass-market sectors; additionally, the material’s inherent brittleness and challenges in machining or sintering to full density without additives increase processing complexities and costs; stringent environmental and safety regulations, including compliance with OSHA and REACH standards for handling dust hazards and waste disposal, impose additional burdens on manufacturers, potentially slowing expansion in regulated regions like Europe and North America.

Opportunities

Opportunities in the Boron Carbide Market are abundant, particularly in emerging regions like Asia-Pacific and the Middle East, where rapid industrialization and infrastructure development create demand for high-performance abrasives and refractory materials in sectors such as oil and gas drilling and construction; the shift toward sustainable energy solutions opens doors for boron carbide in next-generation nuclear reactors, green hydrogen production, and energy storage devices, leveraging its thermal stability and neutron absorption; advancements in additive manufacturing and 3D printing present prospects for producing complex, lightweight components like medical implants and aerospace parts, reducing waste and enabling customization; furthermore, increasing focus on civil security and law enforcement boosts demand for lightweight armor beyond military uses; collaborations for eco-friendly production methods, such as automated processes to minimize environmental impact, along with R&D in nanotechnology for enhanced material properties, position the market for growth by addressing cost barriers and expanding into high-tech applications like electronics and semiconductors.

Challenges

The Boron Carbide Market encounters notable challenges, including supply chain vulnerabilities arising from concentrated raw material sourcing in regions like Turkey and the United States, which are susceptible to geopolitical risks and disruptions as seen during global events like the COVID-19 pandemic; the material’s brittleness and difficulty in achieving full density during sintering without additives complicate fabrication into complex shapes, limiting its versatility in advanced applications; competition from alternative ceramics like silicon carbide, which offer similar properties at lower costs for certain uses, poses a threat to market share in industrial sectors; environmental and regulatory pressures demand investments in safer handling and waste management, increasing operational costs for producers; moreover, the niche nature of the market restricts economies of scale, making it hard for smaller players to compete with established firms in innovation and pricing, while fluctuating demand from cyclical industries like defense and nuclear adds uncertainty to long-term planning.

Boron Carbide Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Boron Carbide Market |

| Market Size 2025 | USD 187 million |

| Market Forecast 2035 | USD 298.4 Million |

| Growth Rate | CAGR of 5.3% |

| Report Pages | 215 |

| Key Companies Covered |

3M Company, Saint-Gobain S.A., Washington Mills North Grafton, Inc., Höganäs AB, Mudanjiang Qianjin Boron Carbide Co., Ltd., Henan Ruiheng New Material Co., Limited, UK Abrasives, Inc., and CoorsTek Inc. |

| Segments Covered | By Grade, By Type, By Application, By End-Use Industry, By Region |

| Regions Covered | Asia Pacific, North America, Europe, Latin America, The Middle East and Africa |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Boron Carbide Market?

Segmentation by Grade

The abrasive grade stands as the most dominant segment in the Boron Carbide Market by grade, capturing over 67% share, primarily because of its exceptional hardness and wear resistance that make it ideal for grinding, lapping, polishing, and ultrasonic drilling in industries like mining, metallurgy, and precision engineering, driving the market by enabling efficient processing of hard materials such as ceramics and metals while reducing tool wear and improving surface quality; this dominance stems from cost-effectiveness compared to specialized grades and broad applicability in high-volume industrial operations, which collectively propel overall market growth through enhanced productivity and lower maintenance costs. The nuclear and defense grade ranks as the second most dominant, with around 30% share, owing to its high neutron absorption and lightweight properties essential for reactor control rods, shielding, and body armor, contributing to market expansion by supporting safety in nuclear energy and protection in military applications, where its ability to withstand extreme conditions without adding significant weight drives demand in high-stakes sectors like energy and security.

Segmentation by Type

In the type segmentation, powder emerges as the most dominant subsegment, holding approximately 60% market share, as its fine particle size and high purity allow for versatile use in abrasives for surface preparation, sintering into components for nuclear shielding, and blending into composites for defense armor, dominating due to ease of handling, customization in grain sizes, and cost-efficient production that accelerates market growth by facilitating innovations in additive manufacturing and high-performance coatings across industrial and high-tech applications. Grains follow as the second most dominant, with about 25% share, valued for their role in abrasive blasting, water jet cutting, and refractory materials where larger particle sizes provide superior impact resistance and durability, helping drive the market through enhanced efficiency in heavy-duty industrial processes like drilling and cutting, which reduce operational downtime and extend equipment life in sectors such as mining and construction.

Segmentation by Application

The industrial application dominates the application segmentation with around 50% share, excelling in grinding, lapping, polishing, and cutting tools for metals and ceramics, as its unmatched hardness minimizes wear and ensures precision in manufacturing, making it dominant by lowering production costs and improving product quality in high-volume sectors like automotive and electronics, thereby driving market growth through increased adoption in automated and sustainable manufacturing practices. The nuclear application is the second most dominant, comprising about 25% share, due to boron carbide’s neutron-absorbing capabilities in control rods and shielding for reactors, which enhance safety and efficiency in power generation, propelling the market by aligning with global shifts toward clean energy and reactor modernizations that demand reliable, high-performance materials to prevent radiation leaks and extend operational lifespans.

Segmentation by End-Use Industry

Industrial manufacturing leads the end-use industry segmentation with over 40% share, utilized for tooling, wear-resistant parts, and refractory linings in processes like metalworking and chemical handling, dominating because of its thermal stability and corrosion resistance that boost operational efficiency and reduce downtime in factories, driving the market by supporting industrialization in emerging economies and enabling cost savings through longer-lasting components. Aerospace and defense ranks second with approximately 30% share, employed in lightweight armor, vehicle protection, and high-temperature components, contributing to market growth by meeting demands for fuel-efficient aircraft and advanced military gear where its low density and impact resistance improve performance and safety in rigorous environments.

What are the Recent Developments in the Boron Carbide Market?

- In February 2022, Samsung announced a strategic shift toward using boron carbide over silicon carbide in the production of focus rings for semiconductor manufacturing, aiming to leverage its superior hardness and thermal properties to enhance precision and durability in wafer processing, which could expand market applications in the electronics sector by improving yield rates and reducing equipment wear.

- In September 2023, Saint-Gobain Boron Nitride formed a partnership with Haydale Group to develop functionalized powders, focusing on enhancing the properties of boron-based materials for advanced applications in abrasives and coatings, potentially driving innovation in wear-resistant solutions and opening new opportunities in industrial and defense sectors through improved material performance and customization.

What is the Regional Analysis of the Boron Carbide Market?

Asia-Pacific Region

The Asia-Pacific region dominates the Boron Carbide Market, accounting for nearly 46% of global share, driven by rapid industrialization, expanding nuclear power programs, and surging demand in defense and manufacturing sectors; China emerges as the dominating country with the highest consumption and production, fueled by its massive manufacturing base for abrasives, government investments in nuclear reactors for energy security, and military modernization efforts that prioritize lightweight armor, enabling the region to lead through cost-effective supply chains, technological advancements in precision engineering, and infrastructure projects that boost applications in mining, automotive, and electronics, while India’s growing nuclear and defense initiatives further support regional expansion by increasing demand for high-purity materials in control rods and protective gear.

North America Region

North America holds a significant position in the Boron Carbide Market, with around 25% share, characterized by advanced R&D in defense and nuclear technologies, alongside strong aerospace and semiconductor industries; the United States stands as the dominating country, leading due to substantial defense budgets for body armor and vehicle protection, nuclear safety enhancements in power plants, and innovations in lightweight composites for space exploration by entities like NASA and SpaceX, driving the region through high-tech applications that emphasize material purity and performance, while collaborations in sustainable manufacturing reduce costs and environmental impact, positioning North America as a hub for premium-grade boron carbide in specialized sectors.

Europe Region

Europe captures about 20% of the Boron Carbide Market, focusing on high-purity applications in nuclear safety, automotive, and refractory materials amid stringent environmental regulations; Germany is the dominating country, excelling through its precision engineering and automotive industries that utilize boron carbide for cutting tools and wear-resistant parts, supported by nuclear programs in France and the UK that demand neutron-absorbing components for reactor efficiency, propelling the region via investments in green technologies and R&D for eco-friendly production, which align with EU sustainability goals and enhance competitiveness in high-value sectors like aerospace and electronics.

Latin America Region

Latin America represents a smaller but growing share of around 5% in the Boron Carbide Market, primarily driven by mining and industrial activities that require abrasives for mineral processing and drilling; Brazil dominates the region, leveraging its vast mining sector for wear-resistant tools and refractory applications in steel production, while infrastructure development and emerging nuclear interests in countries like Argentina boost demand, fostering growth through import dependencies transitioning to local partnerships that improve supply chains and reduce costs in resource-intensive industries.

Middle East & Africa Region

The Middle East & Africa holds approximately 4% of the Boron Carbide Market, with niche growth in oil and gas drilling and emerging defense needs; Saudi Arabia leads as the dominating country, utilizing boron carbide in abrasive nozzles for petroleum extraction and military armor amid diversification efforts, while South Africa’s mining industry supports refractory uses, driving the region through investments in industrial diversification and partnerships for high-performance materials that address harsh environmental conditions and enhance operational efficiency in energy and security sectors.

Who are the Key Market Players and What are Their Strategies in the Boron Carbide Market?

3M Company

3M Company employs strategies centered on R&D innovation to develop high-purity boron carbide with precise boron-to-carbon ratios for advanced ceramics and sapphire cutting, while expanding its global distribution network to penetrate defense and nuclear markets, fostering growth through collaborations in lightweight armor and sustainable manufacturing.

Saint-Gobain S.A.

Saint-Gobain S.A. focuses on partnerships, such as with Haydale Group for functionalized powders, to enhance material properties for abrasives and coatings, alongside capacity expansions in high-tech sectors like electronics and nuclear, driving competitiveness via eco-friendly production and customized solutions for industrial clients.

Washington Mills North Grafton, Inc.

Washington Mills prioritizes quality control in abrasive grains and engineered materials, targeting regional markets in North America with cost-effective supply for industrial manufacturing, while investing in process efficiencies to maintain reliability in defense and refractory applications.

Höganäs AB

Höganäs AB leverages powder metallurgy expertise to innovate in lightweight composites for aerospace and automotive, pursuing strategic alliances to expand into emerging markets and emphasizing automation to reduce production costs and meet regulatory standards.

Mudanjiang Qianjin Boron Carbide Co., Ltd.

Mudanjiang Qianjin emphasizes large-scale production for cost-competitive abrasives and nuclear materials, focusing on Asia-Pacific exports and quality enhancements to capture share in defense and industrial sectors through localized supply chains.

Henan Ruiheng New Material Co., Limited

Henan Ruiheng adopts cost-effective manufacturing for a broad product range, targeting niche applications in refractories and armor via R&D in particle size customization, while building partnerships to strengthen supply in growing Asian markets.

UK Abrasives, Inc.

UK Abrasives concentrates on specialized abrasive products for precision engineering, employing customization strategies for industrial clients and investing in R&D to develop high-performance variants for electronics and medical applications.

CoorsTek Inc.

CoorsTek Inc. pursues advanced ceramic innovations for nuclear and defense uses, with strategies involving acquisitions and technology upgrades to improve durability, while expanding into sustainable energy sectors through global collaborations.

What are the Market Trends in the Boron Carbide Market?

- Increasing adoption of lightweight composites in aerospace and automotive for improved fuel efficiency and reduced emissions, leveraging boron carbide’s low density and high strength.

- Rising integration in additive manufacturing and 3D printing for producing complex components like armor plates and medical implants, enabling customization and waste reduction.

- Growing emphasis on sustainable production methods, including automation and eco-friendly processes to minimize environmental impact and comply with regulations.

- Expansion in nuclear applications with advancements in neutron-absorbing materials for next-generation reactors and renewable energy systems.

- Shift toward high-purity boron carbide in electronics and semiconductors for polishing and thermoelectric devices, driven by precision demands.

- Heightened focus on wear-resistant coatings for industrial equipment in oil, gas, and mining to extend lifespan and lower maintenance costs.

- Emerging uses in nanotechnology and advanced batteries, supporting innovations in energy storage and high-tech sectors.

What Market Segments are Covered in the Boron Carbide Market Report?

By Grade

- Abrasive Grade

- Nuclear & Defense Grade

By Type

- Powder

- Paste

- Grains

By Application

- Industrial

- Nuclear

- Defense

By End-Use Industry

- Mining and Metallurgy

- Aerospace and Defense

- Automotive

- Industrial Manufacturing

- Nuclear Power

- Electronics and Semiconductors

- Medical

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Boron Carbide Market - Industry Analysis

Chapter 4. Global Boron Carbide Market- Competitive Landscape

Chapter 5. Global Boron Carbide Market - Grade Analysis

Chapter 6. Global Boron Carbide Market - Type Analysis

Chapter 7. Global Boron Carbide Market - Application Analysis

Chapter 8. Global Boron Carbide Market - End-Use Industry Analysis

Chapter 9. Boron Carbide Market - Regional Analysis

Chapter 10. Company Profiles

Frequently Asked Questions

The Boron Carbide Market refers to the global industry involved in the production, supply, and utilization of boron carbide (B4C), a super-hard ceramic material used primarily in abrasives, nuclear shielding, defense armor, and industrial tools due to its exceptional hardness, low density, and neutron absorption properties.

Key factors influencing growth include rising demand in defense for lightweight armor, expansion of nuclear power plants, industrial adoption for abrasives and refractory materials, advancements in aerospace and automotive sectors for wear-resistant components, and emerging applications in 3D printing and renewable energy, offset by challenges like high production costs and raw material volatility.

The Boron Carbide Market is projected to reach approximately USD 298.4 million by 2035, starting from an estimated USD 187 million in 2026, reflecting steady expansion driven by diverse industrial and high-tech applications.

The CAGR of the Boron Carbide Market during 2026-2035 is anticipated to be 5.3%, supported by increasing demand across defense, nuclear, and industrial sectors.

Asia-Pacific will contribute notably to the Boron Carbide Market value, accounting for nearly 46% share, driven by rapid industrialization in China and India, nuclear expansions, and defense modernizations.

Major players driving growth include 3M Company, Saint-Gobain S.A., Washington Mills North Grafton, Inc., Höganäs AB, Mudanjiang Qianjin Boron Carbide Co., Ltd., Henan Ruiheng New Material Co., Limited, UK Abrasives, Inc., and CoorsTek Inc., through innovations in production and applications.

The global Boron Carbide Market report can be expected to provide comprehensive insights into market size, CAGR, segmentation, drivers, restraints, opportunities, regional analysis, key players, trends, and forecasts, offering strategic guidance for stakeholders.

The value chain includes raw material sourcing (boric acid and carbon), manufacturing via carbothermic reduction or arc furnace processes, product refinement for purity and particle size, distribution through suppliers, and end-use integration in industries like defense, nuclear, and manufacturing, with after-sales support for customized applications.

Market trends are evolving toward sustainable production and lightweight materials, while consumer preferences shift to high-purity, customizable products for advanced applications in 3D printing, renewables, and precision engineering, emphasizing eco-friendliness and performance efficiency.

Regulatory factors like OSHA and REACH standards for dust handling and waste disposal, along with environmental pressures for low-emission production, affect growth by increasing compliance costs but also driving innovations in sustainable methods and safer materials.