body control module market Size, Share and Trends 2026 to 2035

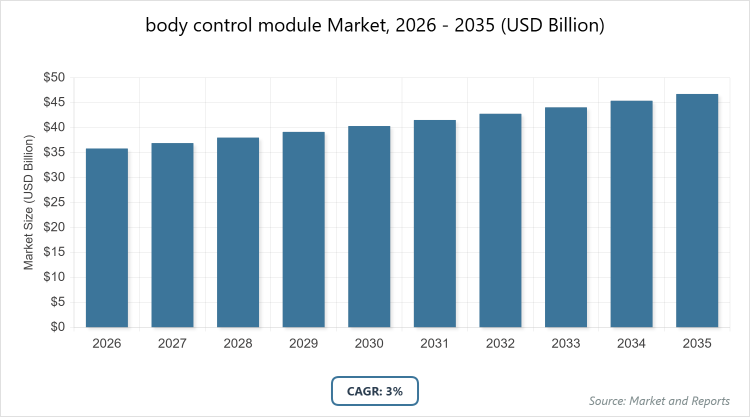

According to MarketnReports, the global body control module market size was estimated at USD 35.84 billion in 2025 and is expected to reach USD 48.15 billion by 2035, growing at a CAGR of 3% from 2026 to 2035. body control module market is driven by increasing demand for advanced automotive electronics, vehicle electrification, and enhanced safety features.What are the key insights into the body control module market?

- The global body control module market was valued at USD 35.84 billion in 2025 and is projected to reach USD 48.15 billion by 2035.

- The market is expected to grow at a CAGR of 3% during the forecast period from 2026 to 2035.

- The market is driven by rising adoption of electric vehicles, advanced driver assistance systems, and demand for enhanced vehicle comfort and safety features.

- In the component segment, hardware dominates with approximately 70% market share due to its essential role in providing the physical infrastructure for control functions, enabling reliable integration of sensors and actuators.

- In the functionality segment, low-end BCMs hold about 62% share because they offer cost-effective solutions for basic vehicle operations, appealing to mass-market vehicles in emerging economies.

- In the vehicle type segment, passenger cars lead with around 64% share, driven by high consumer demand for personal mobility and incorporation of smart features in sedans and SUVs.

- In the communication protocol segment, CAN protocol commands roughly 60% share owing to its proven reliability, low cost, and widespread use in automotive networking for real-time data transmission.

- Asia-Pacific dominates the regional market with approximately 35% share, attributed to massive automotive production volumes in countries like China and India, supported by government incentives for electrification and local manufacturing.

What is the industry overview of the body control module market?

The body control module (BCM) market encompasses the development, production, and distribution of electronic control units that manage various non-engine related functions in vehicles, such as lighting, windows, doors, climate control, security systems, and infotainment interfaces. Market definition refers to BCM as a centralized electronic module that integrates multiple body functions to improve vehicle efficiency, reduce wiring complexity, and enable advanced features like over-the-air updates and connectivity. This market serves the automotive industry, focusing on enhancing user comfort, safety, and vehicle intelligence through hardware and software innovations, while adapting to the shift toward electric and autonomous vehicles.

What are the market dynamics of the body control module market?

Growth Drivers

The growth drivers of the body control module market are primarily fueled by the rapid electrification of vehicles and the integration of advanced driver assistance systems (ADAS). As automakers transition to electric and hybrid models, BCMs play a crucial role in managing low-voltage systems, battery optimization, and seamless connectivity, which enhances energy efficiency and reduces emissions. Additionally, consumer preferences for smart features like adaptive lighting, keyless entry, and infotainment have spurred innovation in BCM designs, leading to increased adoption across passenger and commercial vehicles. Government regulations mandating safety standards, such as those from UNECE, further accelerate market expansion by necessitating advanced BCM functionalities for compliance.

Restraints

Restraints in the body control module market include persistent semiconductor supply chain disruptions and escalating cybersecurity concerns. Volatility in chip availability, exacerbated by global events, has led to production delays and increased costs for manufacturers, hindering scalability. Moreover, the complexity of programming BCMs to meet stringent regulations like UNECE-R155/R156 adds significant development expenses, particularly for smaller OEMs. Transitioning from traditional protocols like CAN/LIN to more advanced Ethernet systems also poses redesign risks, potentially slowing innovation and market penetration in cost-sensitive regions.

Opportunities

Opportunities in the body control module market arise from the proliferation of software-defined vehicles (SDVs) and zonal architectures, which consolidate multiple electronic control units into efficient modules. This shift opens avenues for aftermarket upgrades driven by right-to-repair legislation, allowing consumers to extend vehicle lifespans with customizable BCM solutions. Emerging markets in Latin America and the Middle East & Africa present growth potential through rising automotive production and investments in smart infrastructure, while partnerships with semiconductor firms like NXP enable the development of secure, high-performance BCMs tailored for autonomous driving applications.

Challenges

Challenges facing the body control module market involve intense competition among tier-1 suppliers and the need for continuous R&D to address evolving emission standards. OEMs face pressure to balance cost reductions with investments in advanced technologies, often resulting in inability to pass on expenses to consumers amid market saturation. Liability for product recalls due to failures in critical safety functions adds financial risks, while adapting to regional variations in regulatory frameworks complicates global standardization efforts.

body control module market: Report Scope

| Report Attributes | Report Details |

| Report Name | body control module market |

| Market Size 2025 | USD 35.84 Billion |

| Market Forecast 2035 | USD 48.15 Billion |

| Growth Rate | CAGR of 3% |

| Report Pages | 220 |

| Key Companies Covered |

Continental AG, Robert Bosch GmbH, Denso Corporation, Aptiv PLC, HELLA GmbH & Co. KGaA, and Others. |

| Segments Covered | By Component, By Functionality, By Vehicle Type, By Communication Protocol, and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the body control module market segmented?

The body control module market is segmented by component, functionality, vehicle type, communication protocol, and region.By Component Segment, the hardware subsegment is the most dominant, holding about 70% market share, followed by software as the second most dominant with around 30%. Hardware's dominance stems from its foundational role in integrating physical components like relays and sensors, which are indispensable for reliable vehicle operations; this drives the market by enabling cost-effective mass production and compatibility with legacy systems, while software complements it by offering upgradable features through over-the-air updates, fostering innovation in connected vehicles.

By Functionality Segment, low-end BCMs are the most dominant with approximately 62% share, while high-end BCMs are the second most dominant at about 38%. Low-end BCMs lead due to their affordability and suitability for entry-level vehicles in high-volume markets, driving overall market growth by catering to price-sensitive consumers in emerging economies; high-end variants contribute by incorporating advanced features like ADAS integration, which propels premium segment expansion and technological advancements.

By Vehicle Type Segment, passenger cars dominate with around 64% share, followed by light commercial vehicles as the second most dominant at roughly 25%. Passenger cars' leadership is driven by surging demand for personal transportation equipped with comfort and safety enhancements, boosting market growth through widespread adoption in urban areas; light commercial vehicles support this by addressing logistics needs with efficient BCMs that optimize fleet management and reduce operational costs.

By Communication Protocol Segment, CAN is the most dominant with about 60% share, while LIN holds the second position at approximately 30%. CAN's prevalence is due to its robust, low-cost communication for real-time applications, driving market efficiency by standardizing data exchange in most vehicles; LIN aids growth in supplementary roles for simpler subsystems, enabling modular designs that lower wiring complexity and enhance vehicle intelligence.

What are the recent developments in the body control module market?

- In May 2025, HIRAIN's body control module made its European debut, assisting Foton Piaggio's NP6 light truck in complying with stringent cybersecurity regulations and advancing to mass production, marking a significant expansion for Chinese suppliers into Western markets.

- In January 2025, Marelli launched new BCM solutions in India focused on power distribution and lighting, enhancing local manufacturing capabilities and addressing the growing demand for affordable automotive electronics in emerging regions.

- In September 2024, NOVOSENSE Microelectronics introduced high-side switches for automotive BCMs, designed to handle resistive, inductive, and capacitive loads, improving reliability in zone control units and supporting the shift toward zonal architectures.

- In July 2019, Denso Corporation and Toyota Motor Corporation formed a joint venture for next-generation in-vehicle semiconductors, aiming to accelerate R&D for advanced BCM components and strengthen supply chain resilience.

What is the regional analysis of the body control module market?

Asia Pacific to dominate the global market.Asia Pacific leads the body control module market, driven by massive automotive production and rapid electrification in countries like China, which dominates the region due to its 40% new-energy vehicle sales targets, government subsidies, and established supply chains; this fosters innovation in BCM technologies, with India contributing through expanding manufacturing hubs and rising consumer demand for feature-rich vehicles.

North America exhibits strong growth, propelled by advanced safety regulations and high adoption of hybrid vehicles, with the United States as the dominating country owing to its focus on ADAS and connected technologies, supported by investments from OEMs like General Motors and Tesla, enhancing BCM integration for premium features.

Europe maintains a significant share through stringent emission and cybersecurity standards, led by Germany as the dominating country with its automotive giants like Bosch and Continental driving R&D in zonal architectures and electric mobility, promoting sustainable BCM advancements across the region.

Latin America shows promising expansion from increasing vehicle production and regulatory pushes for emission controls, with Brazil dominating due to its rebounding manufacturing sector and investments in EV infrastructure, enabling greater BCM adoption in commercial fleets.

The Middle East and Africa offer niche opportunities amid rising smart-city initiatives, dominated by the United Arab Emirates through its focus on luxury imports and electrification policies, while South Africa supports growth via premium vehicle demand and regional trade agreements.

Who are the key market players in the body control module market?

Continental AG focuses on innovation through investments in zonal architectures and cybersecurity, partnering with semiconductor firms to develop integrated BCM solutions that enhance vehicle connectivity and reduce wiring complexity, positioning it as a leader in premium automotive electronics.

Robert Bosch GmbH employs strategies centered on R&D for software-defined vehicles and over-the-air updates, leveraging its global supply chain to offer cost-effective BCMs for mass-market and electric vehicles, driving market share through sustainability-focused innovations.

Denso Corporation prioritizes joint ventures, such as with Toyota for semiconductor development, to advance BCM functionalities in ADAS and power management, emphasizing efficiency and reliability to capture growth in Asia-Pacific and emerging markets.

Aptiv PLC adopts a strategy of acquisitions and technology integration, specializing in high-end BCMs for autonomous driving, which strengthens its position by providing scalable solutions for connected and electric vehicle platforms worldwide.

HELLA GmbH & Co. KGaA concentrates on lighting and security modules within BCMs, utilizing partnerships for adaptive ambient systems and aftermarket upgrades, to expand in Europe and North America by addressing regulatory compliance and consumer comfort demands.

What are the market trends in the body control module market?

- Shift toward zonal architectures consolidating ECUs for improved efficiency and reduced vehicle weight.

- Rising investments in software-defined vehicles enabling over-the-air updates and customizable features.

- Increasing adoption of 48V low-voltage systems in EVs for battery optimization and power distribution.

- Growing demand for adaptive ambient lighting in premium segments enhancing user experience.

- Emphasis on cybersecurity compliance with regulations like UNECE-R155/R156 to protect connected systems.

- Expansion of aftermarket BCM upgrades driven by right-to-repair legislation and extended vehicle lifespans.

What market segments and their subsegments are covered in the body control module market report?

By Component

- Hardware

- Software

By Functionality

- High-End

- Low-End

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

By Communication Protocol

- CAN

- LIN

- FlexRay

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

The body control module market involves electronic units managing vehicle body functions like lighting, security, and climate control, serving the automotive sector with hardware and software solutions.

Key factors include vehicle electrification, ADAS adoption, regulatory safety standards, and advancements in connectivity technologies.

The market is projected to grow from USD 35.84 billion in 2026 to USD 48.15 billion by 2035.

The CAGR is expected to be 3%.

Asia Pacific will contribute notably, driven by high automotive production in China and India.

Major players include Continental AG, Robert Bosch GmbH, Denso Corporation, Aptiv PLC, and HELLA GmbH & Co. KGaA.

The report provides in-depth analysis of market size, trends, segments, regional insights, key players, and forecasts.

Stages include raw material sourcing, component manufacturing, assembly, distribution, and aftermarket services.

Trends are shifting toward zonal architectures and SDVs, with consumers preferring enhanced safety, connectivity, and customizable features.

Factors include UNECE cybersecurity regulations, emission standards promoting electrification, and government incentives for green vehicles.