Blood and Fluid Warmer Market Size, Share, and Trends 2026 to 2035

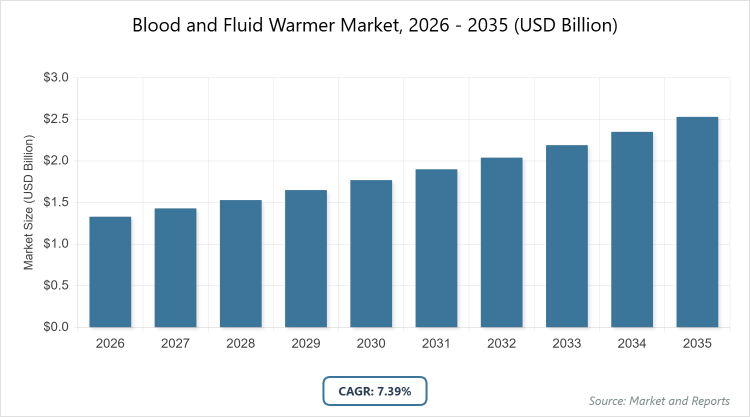

According to MarketnReports, the global Blood and Fluid Warmer market size was estimated at USD 1.33 billion in 2025 and is expected to reach USD 2.51 billion by 2035, growing at a CAGR of 7.39% from 2026 to 2035. The Blood and Fluid Warmer Market is driven by increasing surgical procedures, rising hypothermia cases, and advancements in portable warming technologies.

What are the Key Insights into the Blood and Fluid Warmer Market?

- The global Blood and Fluid Warmer market was valued at USD 1.33 billion in 2025 and is projected to reach USD 2.51 billion by 2035.

- The market is expected to grow at a CAGR of 7.39% during the forecast period from 2026 to 2035.

- The market is driven by rising surgical volumes, increasing hypothermia incidence in elderly and trauma patients, and technological advancements in portable and efficient warming systems.

- In the type segment, inline warmers dominate with approximately 44% market share due to their seamless integration with IV lines and rapid warming capabilities in high-volume clinical use.

- In the application segment, surgery dominates with around 31% share because of the critical need to prevent perioperative hypothermia during prolonged procedures.

- In the end-user segment, hospitals hold the largest share at about 60% owing to high procedure volumes and advanced infrastructure for acute care.

- North America dominates the regional market with roughly a 35-40% share, driven by advanced healthcare systems, high surgical rates, and strong regulatory support for patient safety.

What is the Blood and Fluid Warmer Industry Overview?

The Blood and Fluid Warmer market encompasses medical devices designed to heat intravenous fluids, blood, and blood products to body temperature before administration, preventing hypothermia and related complications during surgeries, trauma care, and transfusions. Blood and fluid warmers are defined as specialized warming systems, often using conductive or convective heating methods, that ensure safe and efficient temperature management of infusates to maintain patient normothermia, improving outcomes in clinical settings like operating rooms, emergency departments, and intensive care units, while complying with regulatory standards for medical device safety and efficacy.

What are the Blood and Fluid Warmer Market Dynamics?

Growth Drivers

The Blood and Fluid Warmer market is propelled by the growing number of surgical procedures worldwide, particularly in aging populations susceptible to hypothermia, where warmers prevent complications like coagulopathy and infection, improving recovery rates. Advancements in portable, battery-operated devices enable use in ambulances and field settings, expanding applications in trauma and emergency care. Regulatory mandates for normothermia maintenance in perioperative guidelines, coupled with rising awareness of hypothermia risks in newborns and chronic patients, drive adoption. Additionally, investments in healthcare infrastructure in emerging markets and integration with infusion systems enhance efficiency, fostering market expansion.

Restraints

Restraints include high costs of advanced warming devices and disposables, limiting accessibility in low-resource settings and smaller clinics. Technical issues like overheating risks or compatibility with certain fluids require stringent quality controls, increasing manufacturing burdens. Reimbursement limitations for warmers in routine procedures and variability in clinical protocols hinder widespread use. Moreover, supply chain disruptions for components like heating elements affect availability and pricing stability.

Opportunities

Opportunities emerge from the rise in elective surgeries and trauma cases in developing regions, where affordable, compact warmers can penetrate untapped markets through local manufacturing. Innovations in wireless, AI-monitored systems for precise temperature control open avenues in homecare and ambulatory settings. Partnerships for bundled infusion-warming solutions and government funding for emergency medical upgrades present growth potential. Furthermore, focus on neonatal and geriatric care drives demand for specialized, user-friendly devices.

Challenges

Challenges involve ensuring device accuracy across varying fluid viscosities and flow rates, necessitating ongoing R&D to avoid hemolysis or thermal injury. Shortage of trained personnel for operation and maintenance in remote areas leads to underutilization. Evolving regulatory standards for safety and efficacy require frequent recertifications, raising compliance costs. Additionally, competition from alternative warming methods like convective blankets intensifies pressure on innovation.

Blood and Fluid Warmer Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Blood and Fluid Warmer Market |

| Market Size 2025 | USD 1.33 Billion |

| Market Forecast 2035 | USD 2.51 Billion |

| Growth Rate | CAGR of 7.39% |

| Report Pages | 220 |

| Key Companies Covered | 3M, Smiths Medical, Stryker, GE Healthcare, Belmont Medical, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Blood and Fluid Warmer Market Segmentation?

The Blood and Fluid Warmer market is segmented by type, application, end-user, and region.

By type, inline warmers emerge as the most dominant subsegment, holding over 44% share, due to their efficient, continuous warming during infusions without disrupting flow, which drives the market by reducing hypothermia risks in high-volume surgeries; the second most dominant is portable warmers, which support market growth through mobility for emergency and field use, enabling rapid response in trauma scenarios.

By application, surgery stands as the most dominant, accounting for about 31% share, as it requires precise normothermia to prevent complications in prolonged operations, propelling overall market expansion; acute care follows as the second dominant, aiding market drive by addressing immediate needs in trauma and critical patients.

By end-user, hospitals dominate with around 60% share, driven by high procedure volumes and integrated systems for patient care, which accelerates market growth; ambulatory surgical centers are the second dominant, contributing to market advancement through outpatient procedure efficiency.

What are the Recent Developments in the Blood and Fluid Warmer Market?

- In September 2025, TSC Life received FDA clearance for its Fluido AirGuard System, a moderate to high flow blood and fluid warmer, enhancing safety in clinical settings.

- In April 2023, Baxter International Inc. launched a new patient warming system as part of its surgical innovations, including the Baxter Patient Warming System for blood and fluid management.

- In March 2025, the FDA cleared the Giotto Monza automated blood component separator, supporting temperature-controlled processing in blood warming applications.

- In January 2025, Stryker announced enhancements to its warming technologies amid broader surgical portfolio expansions.

- In June 2025, new guidelines from AORN emphasized normothermia, boosting demand for advanced warmers in perioperative care.

What is the Regional Analysis of the Blood and Fluid Warmer Market?

- North America is expected to dominate the global market.

North America leads the Blood and Fluid Warmer market, holding approximately 35-40% of the global share, driven by advanced healthcare systems with high surgical volumes in both elective and emergency procedures, stringent patient safety regulations from bodies like the FDA and CMS that mandate hypothermia prevention protocols, strong reimbursement policies for warming devices in perioperative and acute care settings, and increasing adoption in trauma centers, neonatal ICUs, and ambulatory facilities amid rising chronic disease prevalence. The United States dominates within the region as the key innovator and consumer, supported by rapid FDA approvals for cutting-edge technologies like portable inline warmers, high trauma and elective surgery rates fueled by an aging population and lifestyle diseases, presence of major players such as 3M and Stryker with extensive distribution networks, and substantial R&D investments focused on integration with smart infusion systems and AI monitoring.

Europe follows with a share of around 25-30%, fueled by GDPR and MDR-compliant innovations ensuring device safety and data privacy, increasing geriatric population driving demand for surgeries and acute care, and EU-wide guidelines promoting normothermia maintenance in operating rooms and ICUs to reduce postoperative complications. Germany is the dominant country, leveraging its world-class medtech industry with companies like B. Braun and high adoption rates in hospitals for diverse applications, including cardiovascular and orthopedic surgeries, supported by national health insurance covering advanced warming technologies. The United Kingdom and France add substantially, with the UK advancing through NHS initiatives for trauma and elective procedure enhancements using portable warmers, and France prioritizing public health funding for neonatal and emergency warming in high-volume hospitals.

Asia-Pacific emerges as the fastest-growing region with about 20-25% share, propelled by surging healthcare investments from governments and private sectors, rapid expansion of hospital infrastructure in urbanizing areas, increasing surgical tourism attracting international patients, rising prevalence of chronic diseases and trauma cases, and growing awareness of hypothermia prevention in diverse climates. China dominates, capitalizing on its massive healthcare reforms under the Healthy China 2030 plan, exponential growth in hospital networks and surgical procedures, and local manufacturing of cost-effective, inline, and portable warmers to meet demands in ORs, ICUs, and neonatal units. India and Japan contribute notably, with India driven by private hospital chains and government schemes like Ayushman Bharat expanding access to affordable warming devices for trauma and obstetrics, while Japan emphasizes high-tech integrations in geriatric and precision surgery applications supported by MHLW approvals.

Latin America shows emerging potential with a 5-10% share, through gradual improvements in healthcare access via public-private partnerships, rising surgical volumes in urban centers for elective and emergency care, growing recognition of warming devices in preventing hypothermia-related morbidity, and investments in hospital upgrades despite economic variability and resource constraints. Brazil leads, with its public health system SUS incorporating warmers for high-risk procedures in trauma, obstetrics, and cardiovascular surgeries, supported by ANVISA regulations ensuring device safety and international collaborations for affordable imports. Mexico benefits from its booming medical tourism industry and proximity to US standards, facilitatingthe adoption of advanced portable warmers in ambulatory and rental settings.

The Middle East and Africa hold a 5-10% share, driven by expanding medical tourism in affluent hubs, infrastructure projects modernizing hospitals, rising trauma and surgical cases from conflicts and urbanization, and government efforts to improve emergency and neonatal care, but limited by uneven resource distribution, infrastructure gaps, and economic challenges. Saudi Arabia emerges as a leader through Vision 2030 initiatives, funding massive hospital expansions and adopting high-end inline warmers for surgical and acute applications in state-of-the-art facilities. South Africa contributes via its private healthcare sector and university hospitals, utilizing warmers for orthopedic, trauma, and pediatric care, supported by research into local hypothermia risks.

What are the Key Market Players in Blood and Fluid Warmer?

- 3M focuses on innovative conductive warming technologies, expanding through R&D in portable devices and partnerships for surgical integration to enhance patient safety.

- Smiths Medical pursues advanced inline warmers, emphasizing user-friendly designs and global distribution to meet acute care demands.

- Stryker adopts acquisitions for broader portfolios, investing in battery-powered systems for emergency use and sustainability.

- GE Healthcare concentrates on integrated monitoring-warming solutions, leveraging digital features for precise control in hospitals.

- Belmont Medical specializes in high-flow warmers, targeting trauma and military applications with rugged, rapid-heating technologies.

What are the Blood and Fluid Warmer Market Trends?

- Increasing adoption of portable, battery-operated warmers for ambulatory and field use.

- Integration with infusion pumps and monitoring systems for automated control.

- Growth in disposable, hygienic components to prevent cross-contamination.

- Focus on energy-efficient, eco-friendly designs to meet sustainability goals.

- Rising demand in neonatal and geriatric care for specialized warming.

- Expansion of rental models for cost-effective access in emerging markets.

- Advancements in AI for real-time temperature adjustment and alerts.

What are the Market Segments and Subsegments Covered in Blood and Fluid Warmer Report?

By Type

- Portable Warmers

- Inline Warmers

- Countertop Warmers

- Others

By Application

- Surgery

- Acute Care

- Newborn Care

- Homecare

- Others

By End-User

- Hospitals

- Clinics

- Ambulatory Surgical Centers

- Blood Banks

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Blood and fluid warmers are medical devices that heat IV fluids and blood to body temperature to prevent hypothermia during transfusions and surgeries.

Factors include rising surgical procedures, hypothermia awareness, technological advancements, and increasing trauma cases.

The market is projected to grow from USD 1.42 billion in 2026 to USD 2.51 billion by 2035.

The CAGR is expected to be 7.39% from 2026 to 2035.

North America will contribute notably, driven by advanced healthcare and high surgery rates.

Major players include 3M, Smiths Medical, Stryker, GE Healthcare, and Belmont Medical.

The report offers detailed analysis of size, trends, segmentation, regions, players, and forecasts.

Stages include raw material sourcing, manufacturing, distribution, hospital integration, and after-sales service.

Trends favor portable, integrated devices, with preferences for safety, efficiency, and disposables.

FDA/CE approvals for safety and eco-regulations promoting energy-efficient models influence growth.