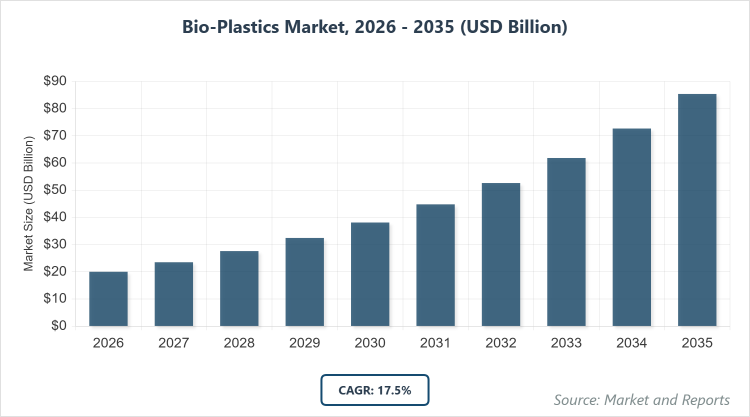

According to MarketnReports, the global Bio-Plastics Market size was estimated at USD 20 billion in 2025 and is expected to reach USD 100 billion by 2035, growing at a CAGR of 17.5% from 2026 to 2035. Bio-Plastics Market is driven by increasing environmental regulations and demand for sustainable alternatives to conventional plastics. The Bio-Plastics Market involves the production and utilization of plastics derived from renewable biological sources such as corn starch, sugarcane, and other biomass, offering biodegradable or bio-based alternatives to traditional petroleum-based plastics to reduce environmental impact and dependence on fossil fuels. This market encompasses a range of materials that can be compostable, recyclable, or durable, applied across industries to address plastic pollution and promote circular economy principles. The market definition centers on eco-friendly polymers that maintain performance characteristics while minimizing carbon footprints, driven by regulatory pressures, consumer preferences for green products, and advancements in biotechnology to enhance scalability and cost-effectiveness in global supply chains. The Bio-Plastics Market is fueled by escalating global awareness of plastic pollution and climate change, prompting governments to enforce bans on single-use plastics and incentivize bio-based alternatives through subsidies and tax benefits. Technological breakthroughs in fermentation and polymerization processes have lowered production costs, enabling scalability, while corporate sustainability goals and consumer shifts toward eco-friendly products in packaging and consumer goods sectors amplify demand, supported by investments in renewable feedstocks like agricultural residues. High production costs compared to conventional plastics, stemming from expensive raw materials and limited economies of scale, hinder widespread adoption, particularly in price-sensitive emerging markets. Supply chain vulnerabilities for biomass feedstocks, influenced by agricultural fluctuations and competition with food production, along with performance limitations in durability and heat resistance for certain applications, restrict market expansion despite environmental advantages. Opportunities emerge from expanding applications in high-growth sectors like automotive and electronics, where lightweight, bio-based composites can reduce emissions, coupled with R&D in advanced bio-polymers for medical uses. Collaborative ventures between agribusiness and chemical firms for localized feedstock sourcing, alongside policy-driven transitions in Europe and Asia, present avenues for market penetration and innovation in fully compostable materials to capture untapped sustainable packaging demands. Challenges include inconsistent global standards for biodegradability and composting infrastructure, leading to consumer confusion and greenwashing concerns, while feedstock scarcity amid climate variability poses supply risks. Balancing performance with cost in competitive markets, navigating intellectual property in bio-tech advancements, and addressing end-of-life management in regions without adequate recycling facilities remain key hurdles for sustained growth. BASF SE, NatureWorks LLC, Braskem, Novamont S.p.A., Total Corbion PLA , and Others The Bio-Plastics Market is segmented by Product Type, Application, End-User, and region. By Product Type Segment, Polylactic Acid (PLA) represent the most dominant segment while Polyhydroxyalkanoates (PHA) stand as the second most dominant. Polylactic Acid (PLA) leads due to its excellent biodegradability, transparency, and compatibility with existing plastic processing equipment, driving market growth by enabling seamless substitution in high-volume applications like packaging and disposables, thus accelerating adoption and reducing reliance on fossil-based plastics. By Application Segment, Packaging is the most dominant segment followed by Automotive as the second most dominant. Packaging dominates because of the urgent need for sustainable solutions in food and consumer goods to comply with anti-plastic regulations, propelling market expansion through large-scale demand that encourages innovation and cost reductions in bio-material production. By End-User Segment, Packaging Industry is the most dominant while Automotive Manufacturers constitute the second most dominant. Packaging Industry prevails as it consumes the bulk of bio-plastics for eco-friendly wrappers and containers, supporting market growth by aligning with global sustainability mandates and fostering supply chain integrations for scalable, affordable alternatives. Asia Pacific to dominate the global market Asia Pacific leads the Bio-Plastics Market, primarily driven by China with its massive manufacturing base, government subsidies for green technologies, and export-oriented production in packaging and textiles, bolstered by rapid urbanization and investments in renewable feedstocks. Europe exhibits robust growth, led by Germany and the Netherlands, where stringent EU regulations on single-use plastics and circular economy initiatives promote bio-plastic adoption in automotive and consumer goods, emphasizing innovation and sustainability certifications. North America shows steady expansion, dominated by the United States through corporate commitments to net-zero emissions and advancements in PLA technologies, supported by agricultural resources and R&D in bio-based alternatives for packaging. Latin America demonstrates emerging potential, with Brazil at the forefront via sugarcane-derived bio-PE production and agribusiness integrations, addressing export demands while tackling domestic plastic waste challenges. The Middle East and Africa are gradually developing, led by the UAE and South Africa through diversification into sustainable materials and partnerships for technology transfer, constrained by feedstock availability but aided by international investments. BASF SE focuses on expanding bio-based polymer portfolios through R&D in PBAT and partnerships for sustainable feedstocks, aiming to enhance performance in packaging applications. NatureWorks LLC prioritizes PLA production scaling with renewable energy sources, leveraging global supply chains to target food packaging and 3D printing markets. Braskem emphasizes bio-PE from sugarcane, investing in carbon-neutral facilities and collaborations for automotive composites to drive circular economy initiatives. Novamont S.p.A. adopts Mater-Bi technology for biodegradable films, focusing on agricultural mulch and composting integrations to meet EU regulatory standards. Total Corbion PLA pursues joint ventures for Luminy PLA expansions, targeting Asia Pacific growth with emphasis on high-heat resistant grades for consumer goods. By Product Type By Application By End-User By RegionBio-Plastics Market Size, Share and Trends 2026 to 2035

What are the Key Insights into the Bio-Plastics Market?

What is the Industry Overview of the Bio-Plastics Market?

What are the Market Dynamics of the Bio-Plastics Market?

Growth Drivers

Restraints

Opportunities

Challenges

Bio-Plastics Market: Report Scope

Report Attributes

Report Details

Report Name

Bio-Plastics Market

Market Size 2025

USD 20 Billion

Market Forecast 2035

USD 100 Billion

Growth Rate

CAGR of 17.5%

Report Pages

220

Key Companies Covered

Segments Covered

By Product Type, By Application, By End-User, and By Region

Regions Covered

North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA)

Base Year

2025

Historical Year

2020 - 2024

Forecast Year

2026 - 2035

Customization Scope

Avail customized purchase options to meet your exact research needs.

What is the Market Segmentation of the Bio-Plastics Market?

What are the Recent Developments in the Bio-Plastics Market?

What is the Regional Analysis of the Bio-Plastics Market?

Who are the Key Market Players in the Bio-Plastics Market?

What are the Market Trends in the Bio-Plastics Market?

What Market Segments and their Subsegments are Covered in the Report?

Frequently Asked Questions

The Bio-Plastics Market comprises renewable, bio-based polymers used as sustainable alternatives to traditional plastics, focusing on biodegradability and reduced environmental impact across various industries.

Key factors include regulatory bans on conventional plastics, advancements in bio-material technologies, rising consumer demand for eco-friendly products, and investments in renewable feedstocks.

The market is projected to grow from approximately USD 20 billion in 2026 to USD 100 billion by 2035.

The CAGR is expected to be 17.5% during the forecast period.

Asia Pacific will contribute notably, driven by high production capacities and government support in China and India.

Major players include BASF SE, NatureWorks LLC, Braskem, Novamont S.p.A., and Total Corbion PLA.

The report offers in-depth analysis of market size, segmentation, dynamics, trends, regional insights, competitive strategies, and future forecasts.

Stages include feedstock sourcing, polymer synthesis, compounding and processing, product manufacturing, distribution, and end-of-life management like composting or recycling.

Trends emphasize biodegradable innovations and circular economy models, while consumers prefer certified sustainable products in packaging and daily goods.

Factors include plastic bans, carbon taxes, and sustainability certifications, alongside environmental pushes for reduced fossil fuel dependency and waste minimization.