Ball Bearing Market Size, Share and Trends 2026 to 2035

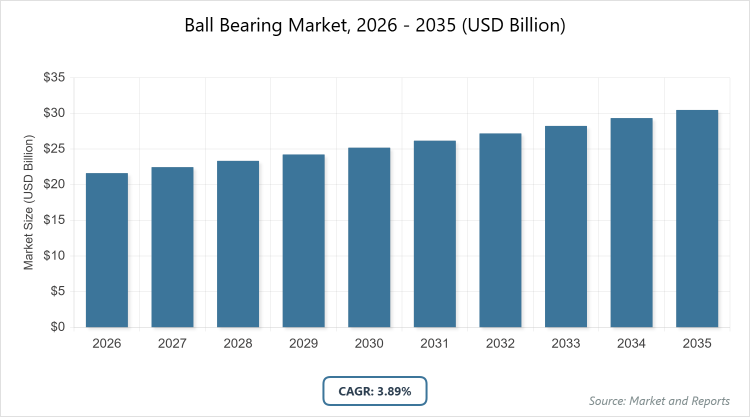

According to MarketnReports, the global Ball Bearing market size was estimated at USD 21.63 billion in 2025 and is expected to reach USD 31.69 billion by 2035, growing at a CAGR of 3.89% from 2026 to 2035. Ball Bearing Market is driven by increasing demand from automotive and industrial sectors amid technological advancements.

What is the Overview of Ball Bearing Market?

The ball bearing market encompasses the production, distribution, and application of precision-engineered components designed to reduce friction between moving parts in machinery, enabling smooth rotation and load support in various industrial and consumer applications. This market includes diverse types such as deep groove, angular contact, and thrust bearings, manufactured from materials like steel, ceramic, or hybrids to meet specific performance requirements in terms of speed, load capacity, and environmental resistance. Market definition refers to the industry focused on antifriction bearings that facilitate efficient mechanical operations across sectors like automotive, aerospace, and manufacturing, addressing needs for durability, precision, and energy efficiency while supporting global industrialization and innovation in machinery design to minimize wear and enhance operational longevity.

What are the Key Insights into Ball Bearing Market?

- The global ball bearing market was valued at USD 21.63 billion in 2025 and is projected to reach USD 31.69 billion by 2035.

- The market is expected to grow at a CAGR of 3.89% during the forecast period from 2026 to 2035.

- The market is driven by rising automation in manufacturing and expansion in electric vehicle production.

- In the type segment, deep groove ball bearings dominate with a 45% share.

- This dominance is due to their versatility, high-speed capability, and cost-effectiveness, driving market growth by enabling widespread use in everyday machinery and reducing maintenance needs.

- In the application segment, automotive dominates with a 40% share.

- This is attributed to increasing vehicle production and demand for efficient components, fueling expansion through innovations in lightweight designs for fuel efficiency.

- In the end-use industry segment, automotive dominates with a 35% share.

- This stems from the sector’s reliance on precision bearings for engines and transmissions, propelling the market by supporting electrification trends.

- Asia Pacific dominates the global market with a 42% share.

- This is owing to rapid industrialization, manufacturing hubs, and investments in infrastructure in China.

What are the Market Dynamics in Ball Bearing?

Growth Drivers

Growth drivers in the ball bearing market are fueled by the surge in automotive production, particularly electric vehicles, which require high-precision bearings for efficient power transmission and reduced energy loss, attracting investments from manufacturers aiming to meet stringent emission standards. Advancements in material technologies, such as ceramic and hybrid bearings, enhance durability and performance in harsh environments, appealing to aerospace and industrial sectors seeking reliability. The rise of automation and robotics in manufacturing increases demand for low-friction components, while global infrastructure projects boost usage in construction equipment. Additionally, sustainability initiatives promote lightweight bearings that improve fuel efficiency, driving overall market expansion through innovation and application diversification.

Restraints

Restraints in the ball bearing market include volatile raw material prices, particularly for steel and alloys, which elevate production costs and impact profitability for manufacturers in competitive pricing environments. Intense competition from low-cost imports, especially from Asia, pressures established players to maintain quality while reducing margins. Supply chain disruptions, exacerbated by geopolitical tensions, delay deliveries and increase lead times. Moreover, the shift toward maintenance-free alternatives like magnetic bearings in niche applications limits traditional ball bearing demand, hindering growth in advanced sectors.

Opportunities

Opportunities in the ball bearing market emerge from the growing adoption of renewable energy systems, such as wind turbines, where specialized bearings for high loads and low maintenance open avenues for customized solutions in emerging green technologies. Expansion in emerging economies with infrastructure booms presents potential for affordable, durable bearings tailored to local industries. Innovations in smart bearings with sensors for predictive maintenance attract IoT-integrated sectors, enabling data-driven efficiencies. Strategic alliances with EV manufacturers for lightweight, high-performance bearings further enhance opportunities for market penetration and premium pricing.

Challenges

Challenges in the ball bearing market involve stringent quality standards and certifications required for aerospace and medical applications, necessitating continuous R&D investments that strain smaller manufacturers. Counterfeit products erode market trust and revenue, particularly in unregulated regions, compromising safety. Rapid technological shifts toward alternative bearing types demand adaptation, risking obsolescence for traditional producers. Additionally, environmental regulations on material disposal add compliance costs, while labor shortages in skilled manufacturing affect production scalability.

Ball Bearing Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Ball Bearing Market |

| Market Size 2025 | USD 21.63 Billion |

| Market Forecast 2035 | USD 31.69 Billion |

| Growth Rate | CAGR of 3.89% |

| Report Pages | 220 |

| Key Companies Covered | SKF, NTN Corporation, Timken, Schaeffler Group, JTEKT, and Others |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

The Ball Bearing market is segmented by type, application, end-use industry, and region.

Based on Type Segment, the most dominant subsegment is deep groove ball bearings, while the second most dominant is angular contact ball bearings. Deep groove ball bearings lead due to their ability to handle radial and axial loads with minimal friction, driving market growth by supporting versatile applications in motors and appliances that enhance efficiency and longevity; angular contact ball bearings rank second as they excel in high-speed, precision scenarios, contributing to expansion through use in machine tools and automotive hubs for improved performance under combined loads.

Based on Application Segment, the most dominant subsegment is automotive, while the second most dominant is industrial machinery. Automotive dominates owing to the need for reliable components in vehicles for smooth operation and fuel efficiency, propelling market growth via demand from EV transitions that require advanced bearings for electric motors; industrial machinery follows as the second dominant, driven by automation needs, enhancing the market through durable solutions that reduce downtime in production lines.

Based on End-Use Industry Segment, the most dominant subsegment is automotive, while the second most dominant is aerospace & defense. Automotive leads because of high-volume production and innovation in vehicle design requiring precision bearings, fueling market growth by addressing electrification and lightweighting trends; aerospace & defense ranks second with requirements for high-reliability components in extreme conditions, advancing the market through specialized materials that ensure safety and performance.

What are Recent Developments in Ball Bearing Market?

- In 2025, SKF launched a new series of hybrid deep groove ball bearings for electric motors, combining steel rings with ceramic balls to reduce friction and extend service life.

- In late 2024, NTN Corporation acquired a precision bearing startup to enhance its portfolio in robotics applications, focusing on high-speed angular contact designs.

- In 2025, Timken introduced sensor-equipped thrust ball bearings for predictive maintenance in wind turbines, improving reliability in renewable energy.

- In 2024, Schaeffler Group partnered with an EV manufacturer for custom self-aligning ball bearings, optimizing performance in electric drivetrains.

What is the Regional Analysis for Ball Bearing Market?

- Asia Pacific to dominate the global market.

Asia Pacific dominates the ball bearing market, driven by extensive manufacturing activities, automotive production booms, and infrastructure investments that demand high-volume, cost-effective bearings for efficiency. The region’s growth is supported by skilled labor and supply chain advantages. China dominates within Asia Pacific, propelled by its role as a global manufacturing powerhouse with companies like NTN expanding facilities to meet domestic and export needs in electronics and vehicles, alongside government subsidies for industrial upgrades; India contributes through automotive growth, Japan focuses on precision technologies, but challenges include trade tariffs affecting exports.

North America holds a significant share in the ball bearing market, characterized by advanced R&D and strong aerospace sectors requiring high-precision components. Investments in EVs and automation drive innovation. The United States dominates the region, supported by firms like Timken leading in hybrid bearings for defense and automotive, with robust supply chains; Canada benefits from mining applications, Mexico leverages manufacturing relocations, though high labor costs restrain competitiveness.

Europe exhibits steady growth in the ball bearing market, emphasizing sustainability and quality standards that promote eco-friendly materials. Mature automotive and machinery industries fuel demand. Germany leads as the dominating country, bolstered by its engineering heritage and companies like Schaeffler innovating in EV bearings; the UK and France follow with aerospace focus, while Eastern Europe offers low-cost production, despite regulatory complexities.

Latin America shows emerging potential in the ball bearing market, influenced by automotive and mining sectors. Improving trade agreements facilitate imports. Brazil dominates as the key country, with its vehicle industry adopting advanced bearings; Mexico benefits from NAFTA ties, Argentina focuses on agriculture, though economic instability challenges investments.

The Middle East and Africa (MEA) region is nascent in the ball bearing market, driven by oil & gas and construction projects. Investments in diversification boost usage. South Africa dominates within MEA, supported by mining operations requiring durable bearings; the UAE invests in infrastructure, Saudi Arabia through Vision 2030, but geopolitical issues hinder growth.

Who are the Key Market Players in Ball Bearing?

SKF focuses on hybrid innovations and sustainability, expanding through R&D for EV applications to capture green markets.

NTN Corporation employs acquisitions for precision enhancements, targeting robotics with high-speed designs for efficiency.

Timken pursues sensor integrations for predictive maintenance, leveraging partnerships in renewables for reliability.

Schaeffler Group adopts EV customizations, investing in lightweight materials to meet automotive demands.

JTEKT concentrates on angular contact advancements, collaborating for machine tool optimizations.

NSK Ltd. emphasizes ceramic hybrids, utilizing global networks for aerospace precision.

What are the Market Trends in Ball Bearing?

– Shift toward ceramic and hybrid materials for enhanced durability and reduced weight.

- Integration of sensors for IoT-enabled predictive maintenance.

- Growth in EV-specific bearings for electric motors.

- Rise in sustainable manufacturing with recycled materials.

- Expansion of precision bearings in robotics and automation.

- Focus on low-friction designs for energy efficiency.

- Surge in miniature bearings for electronics.

- Adoption of 3D printing for custom prototypes.

What Market Segments and Subsegments are Covered in the Ball Bearing Report?

By Type

-

- Deep Groove Ball Bearings

- Angular Contact Ball Bearings

- Self-Aligning Ball Bearings

- Thrust Ball Bearings

- Miniature Ball Bearings

- Ceramic Ball Bearings

- Stainless Steel Ball Bearings

- Plastic Ball Bearings

- Hybrid Ball Bearings

- Precision Ball Bearings

- Others

By Application

-

- Automotive

- Aerospace

- Industrial Machinery

- Electrical

- Medical

- Robotics

- Agriculture

- Construction

- Mining

- Marine

- Others

By End-Use Industry

-

- Automotive

- Aerospace & Defense

- Heavy Machinery

- Consumer Electronics

- Healthcare

- Energy & Power

- Agriculture

- Construction

- Mining

- Marine

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Ball bearings are mechanical components that reduce friction between rotating parts, enabling smooth motion in machinery.

Key factors include automotive electrification, industrial automation, material innovations, and infrastructure investments.

The Ball Bearing market is projected to grow from approximately USD 21.63 billion in 2025 to USD 31.69 billion by 2035.

The Ball Bearing market is expected to register a CAGR of 3.89% during the forecast period from 2026 to 2035.

Asia Pacific will contribute notably, holding around 42% of the market share due to industrialization and manufacturing.

Major players include SKF, NTN Corporation, Timken, Schaeffler Group, JTEKT, and NSK Ltd., driving growth through innovations and expansions.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, and forecasts.

The value chain includes raw material sourcing, manufacturing, assembly, distribution, and end-user integration.

Trends are evolving toward smart and sustainable bearings, with preferences shifting to durable, efficient components for modern applications.

Regulatory factors include quality standards like ISO, while environmental factors involve restrictions on materials pushing for eco-friendly alternatives.