Aviation Test Equipment Market Size, Share and Trends 2026 to 2035

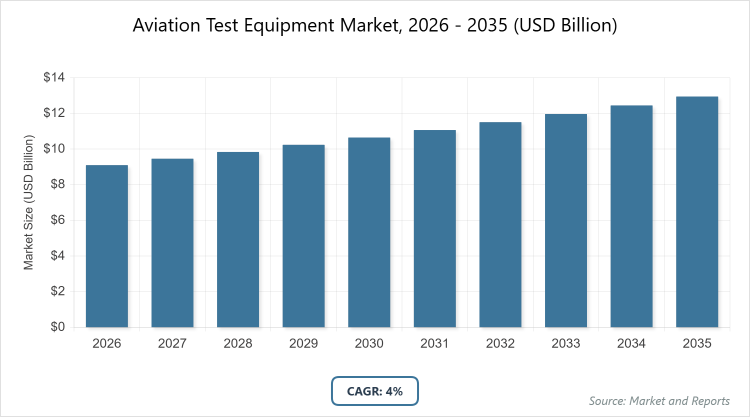

According to MarketnReports, the global Aviation Test Equipment market size was estimated at USD 9.1 billion in 2025 and is expected to reach USD 13.4 billion by 2035, growing at a CAGR of 4% from 2026 to 2035. Aviation Test Equipment Market is driven by increasing demand for advanced aircraft systems and stringent safety regulations.

What are the Key Insights of Aviation Test Equipment Market?

- The global aviation test equipment market size was valued at USD 9.1 billion in 2025 and is projected to reach USD 13.4 billion by 2035.

- The market is anticipated to grow at a CAGR of 4% during the forecast period from 2026 to 2035.

- The aviation test equipment market is driven by rising air traffic, fleet expansions, stringent regulatory requirements for safety, and advancements in aircraft technologies such as unmanned aerial vehicles and electric propulsion systems.

- In the product type segment, electrical test equipment dominates with a 40% share due to the increasing complexity of avionics and electronic systems in modern aircraft, which require precise diagnostics to ensure operational integrity and compliance with standards.

- In the application segment, commercial aircraft holds the leading position with 65% market share because of the surging global passenger and cargo demand, necessitating frequent testing to maintain fleet efficiency and minimize downtime.

- In the end-user segment, the commercial sector commands 60% of the market as airlines and MRO providers invest heavily in test equipment to support large-scale operations and adhere to international aviation safety protocols.

- North America dominates the global aviation test equipment market with a 42% share, attributed to its well-established aerospace infrastructure, presence of major manufacturers like Boeing and Honeywell, and strict FAA regulations driving continuous innovation and adoption.

What is the Aviation Test Equipment Industry Overview?

The aviation test equipment market encompasses a wide range of specialized tools and systems designed to ensure the safety, reliability, and performance of aircraft components and systems throughout their lifecycle. Market definition includes devices used for testing electrical, hydraulic, pneumatic, power, and other critical aviation systems, covering everything from ground-based diagnostics to in-flight monitoring solutions that support maintenance, repair, and overhaul activities in both commercial and military sectors.

What are the Aviation Test Equipment Market Dynamics?

Growth Drivers The primary growth drivers in the aviation test equipment market include the expansion of global air fleets and the enforcement of rigorous safety standards by regulatory bodies such as the FAA and EASA, which mandate regular testing and certification of aircraft systems. Additionally, the rise in maintenance, repair, and overhaul (MRO) activities for aging aircraft fleets further propels demand, as operators seek advanced equipment to enhance efficiency and reduce operational costs through predictive diagnostics.

Restraints

High initial costs associated with acquiring sophisticated aviation test equipment pose a significant restraint, particularly for smaller MRO facilities and operators in developing regions. Moreover, the shortage of skilled technicians trained in handling complex digital and automated testing systems can hinder market growth, leading to delays in implementation and increased training expenses.

Opportunities

Emerging opportunities lie in the integration of artificial intelligence and IoT in test equipment, enabling real-time data analytics and remote monitoring, which can open new avenues for market players in the growing unmanned aerial vehicle (UAV) and electric aircraft sectors. Expanding aviation infrastructure in Asia-Pacific and Latin America also presents untapped potential for customized, cost-effective testing solutions tailored to regional needs.

Challenges

Supply chain disruptions, including shortages of electronic components and raw materials, present ongoing challenges that can delay production and delivery of test equipment. Furthermore, evolving cybersecurity threats to connected aviation systems require continuous updates to testing protocols, adding complexity and cost to compliance efforts.

Aviation Test Equipment Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Aviation Test Equipment Market |

| Market Size 2025 | USD 9.1 Billion |

| Market Forecast 2035 | USD 13.4 Billion |

| Growth Rate | CAGR of 4% |

| Report Pages | 240 |

| Key Companies Covered |

Honeywell International Inc., Boeing, Airbus, Collins Aerospace, Teradyne Inc., Moog Inc., General Electric Company, Lockheed Martin Corporation, 3M Company, Rolls-Royce Holdings Plc, and Others |

| Segments Covered | By Product Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Aviation Test Equipment Market Segmentation?

The Aviation Test Equipment market is segmented by product type, application, end-user, and region.

Based on Product Type Segment, electrical test equipment emerges as the most dominant, followed by hydraulic test equipment as the second most dominant. Electrical test equipment leads due to the proliferation of advanced avionics and electronic controls in next-generation aircraft, driving the market by enabling precise fault detection and system validation that minimizes downtime and enhances safety; hydraulic test equipment ranks second as it is essential for ensuring the reliability of flight control and landing gear systems, contributing to overall market growth through its role in high-pressure simulations that support fleet modernization efforts.

Based on Application Segment, commercial aircraft is the most dominant, with military aircraft as the second most dominant. Commercial aircraft dominates owing to the exponential rise in global air travel and cargo transport, propelling the market by necessitating robust testing for large fleets to comply with safety norms and optimize operational efficiency; military aircraft follows as it benefits from increased defense budgets and modernization programs, aiding market expansion through specialized testing for combat-ready systems that improve mission success rates.

Based on End-User Segment, commercial is the most dominant, followed by defense/military as the second most dominant. The commercial end-user leads because of the vast network of airlines and MRO services requiring frequent equipment checks to handle passenger growth, fueling the market by promoting investments in scalable testing solutions; defense/military is second due to ongoing geopolitical tensions driving procurement of advanced test gear for aircraft readiness, which supports market dynamics by fostering innovation in rugged, high-performance tools.

What are the Recent Developments in Aviation Test Equipment?

- In December 2024, VIAVI Solutions signed a definitive agreement to acquire Inertial Labs, enhancing its portfolio in aerospace and defense testing with advanced navigation and positioning technologies.

- In October 2025, the U.S. Department of Defense awarded a contract to Consolidated Contractors Company for supplying pressure test adapters from Nav-Aids, aimed at supporting U.S. Army maintenance for Black Hawk helicopters.

- In September 2025, a USD 980 billion deal was awarded to 33 companies by the U.S. Air Force for supplying automation test systems to support development, procurement, and sustainment initiatives.

- In September 2024, GE Aerospace opened its Services Technology Acceleration Center near Cincinnati, focusing on advancing engine inspection, repair, and overhaul technologies.

What is the Aviation Test Equipment Regional Analysis?

North America to dominate the global market.

North America holds the largest share, driven by its advanced aerospace ecosystem and major players like Boeing and Honeywell, with the United States as the dominating country due to substantial investments in R&D, stringent FAA regulations, and a high concentration of MRO facilities that ensure continuous demand for cutting-edge test equipment.

Europe follows as a key region, supported by strong aviation manufacturing hubs and collaborations through entities like Airbus, where Germany and the United Kingdom dominate owing to their focus on technological innovation, defense modernization, and compliance with EASA standards that promote efficient aircraft testing infrastructures.

Asia Pacific is the fastest-growing region, fueled by expanding commercial fleets and government initiatives in aviation, with China and India as dominating countries because of rapid urbanization, increasing air traffic, and investments in indigenous aircraft programs that necessitate enhanced testing capabilities for safety and performance.

Latin America shows steady growth, driven by rising air travel and fleet upgrades, with Brazil dominating through its established aerospace industry led by Embraer, emphasizing MRO expansions and regulatory alignments that boost the adoption of reliable test equipment.

The Middle East and Africa exhibit emerging potential, supported by aviation hub developments and military procurements, where the United Arab Emirates dominates due to its strategic investments in defense and commercial aviation, fostering demand for sophisticated testing solutions amid fleet diversification efforts.

Who are the Key Aviation Test Equipment Market Players?

- Honeywell International Inc. focuses on continuous innovation through R&D investments in AI-integrated testing solutions and strategic partnerships to expand its global footprint in avionics and engine diagnostics.

- Boeing emphasizes collaborations with suppliers and acquisitions to enhance its in-house testing capabilities, prioritizing predictive maintenance tools to support its commercial and defense aircraft portfolios.

- Airbus pursues sustainability-driven strategies, including joint ventures for electric aircraft testing equipment and digital transformation initiatives to improve efficiency in MRO operations.

- Collins Aerospace (RTX Corporation) adopts a merger and acquisition approach to integrate advanced sensor technologies, coupled with a focus on modular test systems for unmanned and manned aircraft applications.

- Teradyne Inc. leverages technological advancements in automated test equipment, forming alliances with aerospace OEMs to develop high-precision solutions for electronics and systems validation.

- Moog Inc. concentrates on product diversification through new launches like motion systems and international expansions to cater to simulation and control testing needs in defense sectors.

- General Electric Company invests in facility expansions, such as technology acceleration centers, and partnerships for engine testing innovations to drive reliability in aviation propulsion systems.

- Lockheed Martin Corporation prioritizes government contracts and R&D in cybersecurity-enhanced test equipment to support military aircraft readiness and complex system integrations.

- 3M Company focuses on material science advancements and supply chain optimizations to provide durable, high-performance testing components for various aviation applications.

- Rolls-Royce Holdings Plc employs data analytics strategies and collaborative R&D for engine health monitoring tools, aiming to reduce downtime through predictive testing methodologies.

What are the Aviation Test Equipment Market Trends?

- Integration of AI and machine learning for predictive maintenance and real-time diagnostics in test equipment.

- Rising adoption of portable and handheld devices for on-field testing to enhance operational flexibility.

- Growing focus on testing solutions for electric and hybrid aircraft amid the shift toward sustainable aviation.

- Increased use of digital twins and simulation technologies to reduce physical testing costs and time.

- Emphasis on cybersecurity features in test equipment to protect connected aviation systems from threats.

- Expansion of unmanned aerial vehicle testing capabilities due to proliferating drone applications in commercial and defense.

- Advancements in wireless and remote testing systems for improved accessibility in remote locations.

What are the Aviation Test Equipment Market Segments and their Subsegments Covered in the Report?

By Product Type

-

Electrical Test Equipment

-

Hydraulic Test Equipment

-

Power Test Equipment

-

Pneumatic Test Equipment

-

Avionics Test Equipment

-

Engine Test Equipment

-

Radar Test Equipment

-

Battery Test Equipment

-

Fuel System Test Equipment

-

Structural Test Equipment

-

Others

By Application

-

- Commercial Aircraft

- Military Aircraft

- Unmanned Aerial Vehicles

- Helicopters

- Business Jets

- Cargo Aircraft

- Passenger Aircraft

- Fighter Jets

- Transport Aircraft

- Surveillance Aircraft

- Others

By End-User

-

- Commercial

- Defense/Military

- MRO Services

- OEMs

- Airports

- Research Institutions

- Training Centers

- Government Agencies

- Private Operators

- Airlines

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Aviation test equipment refers to specialized tools and systems used to evaluate, diagnose, and validate the performance, safety, and functionality of aircraft components, including electrical, hydraulic, and avionics systems.

Key factors include expanding global air fleets, stringent safety regulations, technological advancements in aircraft like UAVs and electric models, and rising MRO activities driven by aging aircraft.

The market is projected to grow from approximately USD 9.5 billion in 2026 to USD 13.4 billion by 2035.

The CAGR is expected to be 4% over the forecast period.

North America will contribute notably, holding around 42% of the market value due to its advanced aerospace infrastructure and regulatory environment.

Major players include Honeywell International Inc., Boeing, Airbus, Collins Aerospace, Teradyne Inc., Moog Inc., General Electric Company, Lockheed Martin Corporation, 3M Company, and Rolls-Royce Holdings Plc.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, and forecasts from 2026 to 2035.

The value chain includes raw material procurement, manufacturing of test equipment, distribution and sales, end-user application in MRO and operations, and after-sales support services.

Trends are shifting toward AI-integrated and portable equipment, with preferences favoring sustainable, cost-effective solutions for electric aircraft and remote diagnostics.

Stringent FAA and EASA regulations on safety and emissions, along with environmental pushes for greener aviation, are driving demand for advanced, eco-friendly testing solutions.