Aviation Analytics Market Size, Share and Trends 2026 to 2035

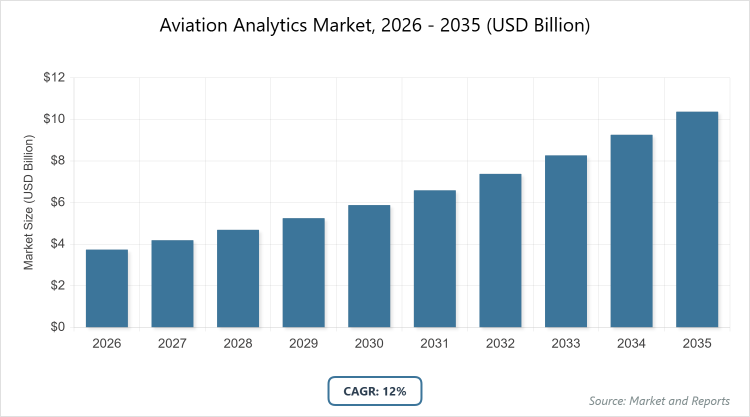

According to MarketnReports, the global Aviation Analytics market size was estimated at USD 3.74 billion in 2025 and is expected to reach USD 11.6 billion by 2035, growing at a CAGR of 12% from 2026 to 2035. Aviation Analytics Market is driven by increasing adoption of predictive maintenance and fuel optimization to enhance operational efficiency.

What are the Key Insights into Aviation Analytics Market?

- The global aviation analytics market was valued at USD 3.74 billion in 2025 and is projected to reach USD 11.6 billion by 2035.

- The market is expected to grow at a CAGR of 12% during the forecast period from 2026 to 2035.

- The market is driven by adoption of predictive maintenance to cut aircraft on ground losses and fuel-burn optimization amid rising costs.

- Airlines dominated the end-user segment with 54% share.

- Airlines dominate due to heavy investments in revenue-management engines and ancillary-pricing algorithms that directly impact profitability.

- Fuel management dominated the application segment with 30% share.

- Fuel management dominates as it leverages machine-learning to reduce fuel spend by 1-4.3%, addressing one of the largest operational costs in aviation.

- Predictive analytics dominated the analytics type segment with 45% share.

- Predictive analytics dominates owing to accumulated flight data enabling failure pattern identification and proven ROI in maintenance.

- Cloud dominated the deployment segment with 67% share.

- Cloud dominates because it provides scalable infrastructure for real-time processing and AI-driven initiatives.

- Software dominated the component segment with 58% share.

- Software dominates as it includes essential dashboards, AI engines, and decision-support tools integral to analytics implementation.

- Finance dominated the business function segment with 32% share.

- Finance dominates due to prioritization of fare personalization and cost oversight in volatile market conditions.

- North America dominated the regional segment with 35% share.

- North America dominates supported by early data connectivity, major OEM presence, and regulatory guidance on AI and safety.

What is the Industry Overview of Aviation Analytics Market?

The aviation analytics market encompasses software and services that enable airlines, airports, and related entities to collect, process, and analyze data from flights, fleets, passengers, finances, and operations to boost efficiency, safety, and revenue generation. It includes various analytics approaches from descriptive to prescriptive, deployed either on-premise or via cloud, focusing on commercial, cargo, and regional aviation sectors. Market definition refers to the ecosystem of licensed analytics tools and paid services excluding hardware, generic business intelligence platforms, or standalone consulting, aimed at transforming vast aviation data into actionable insights for decision-making.

What are the Market Dynamics of Aviation Analytics Market?

Growth Drivers The primary growth drivers in the aviation analytics market include the rising adoption of predictive maintenance solutions that minimize aircraft downtime, which can cost up to USD 100,000 per hour, by analyzing sensor data to foresee component failures and schedule repairs proactively. Additionally, fuel-burn optimization is propelled by escalating sustainable aviation fuel costs and environmental regulations, enabling airlines to achieve 1-4.3% savings through machine-learning models that consider over 650 flight parameters. Big data from next-generation aircraft sensors further drives growth by facilitating monetization opportunities, while safety mandates like flight data monitoring analytics enhance compliance and risk mitigation across operations.

Restraints

Key restraints encompass legacy IT systems creating data silos that hinder interoperability and comprehensive analysis, particularly in established carriers where integration challenges slow adoption. A shortage of specialized data scientists with aviation domain knowledge limits advanced implementations, especially in emerging regions. Cybersecurity risks associated with cloud-based flight data streaming pose threats, requiring robust protections that increase costs. Passenger privacy regulations, such as GDPR, restrict behavioral analytics, limiting the scope of customer-centric applications and slowing personalization efforts.

Opportunities

Opportunities abound in emerging areas like eVTOL fleet analytics for urban air mobility, airport curb-to-gate synchronization to improve passenger flow, and unified data fabrics bundling multiple use cases for holistic insights. Open architectures and outcome-based pricing models allow for flexible, cost-effective solutions, attracting smaller operators. Expansion into cross-operation control towers offers potential for real-time collaboration between airlines and airports, while AI advancements enable new services like dynamic routing based on real-time sustainable fuel performance data.

Challenges

Challenges include bridging the skills gap for AI talent with aviation expertise, necessitating targeted training programs. Change management in legacy environments resists rapid adoption, requiring cultural shifts within organizations. Increasing cyber-threats demand hybrid architectures balancing cloud benefits with on-premise security, complicating deployments. Regulatory variations, such as FAA electronic system security rules, add compliance burdens that vary by region and can delay global rollouts.

Aviation Analytics Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Aviation Analytics Market |

| Market Size 2025 | USD 3.74 Billion |

| Market Forecast 2035 | USD 11.6 Billion |

| Growth Rate | CAGR of 12% |

| Report Pages | 220 |

| Key Companies Covered |

Boeing, Safran, GE Aerospace, SITA, Amadeus, Honeywell, IBM, SAP, Oracle, and Others |

| Segments Covered | By Analytics Type, By Application, By End-User, By Deployment, By Component, By Business Function, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Aviation Analytics Market?

The Aviation Analytics market is segmented by analytics type, application, end-user, and region.

Based on Analytics Type Segment. Predictive analytics stands as the most dominant subsegment, holding a 45% share, followed by prescriptive analytics as the second most dominant with significant growth potential. Predictive analytics dominates due to its ability to leverage historical flight data for failure predictions, reducing maintenance costs and downtime, which drives the market by enabling proactive strategies that enhance fleet reliability and operational efficiency; prescriptive analytics, while second, supports decision optimization during disruptions, cutting recovery costs by up to 15% and contributing to overall market growth through actionable recommendations.

Based on Application Segment. Fuel management emerges as the most dominant subsegment with a 30% share, while maintenance analytics is the second most dominant. Fuel management dominates because it addresses high fuel expenses through advanced modeling, achieving substantial savings that directly boost profitability and sustainability efforts, driving the market by aligning with cost-reduction priorities; maintenance analytics, as second, facilitates condition-based servicing over scheduled intervals, minimizing inventory needs and labor, thereby propelling market expansion via improved asset utilization.

Based on End-User Segment. Airlines represent the most dominant subsegment with a 54% share, followed by airports as the second most dominant. Airlines dominate owing to their focus on integrated revenue and pricing tools that optimize earnings in competitive landscapes, driving the market through large-scale data applications; airports, growing fastest, utilize analytics for passenger flow and capacity management, contributing to market growth by enhancing infrastructure efficiency amid rising traffic.

What are the Recent Developments in Aviation Analytics Market?

- In April 2025, Boeing divested parts of its Digital Aviation Solutions business, including Jeppesen, ForeFlight, and AerData, to Thoma Bravo for USD 10.55 billion, allowing focus on core airframe programs while maintaining supply of maintenance analytics via long-term contracts.

- In December 2024, IDEMIA and SITA introduced the Augmented Luggage Identification Experience, using biometrics to reduce baggage mishandling rates through enhanced tracking analytics.

- In December 2024, Lufthansa Technik integrated AI into MRO workflows for improved parts forecasting and repair-slot allocation, boosting efficiency in maintenance operations.

- In September 2024, Safran acquired AI firm Preligens for EUR 220 million to strengthen analytics in autonomous systems, expanding capabilities in predictive and prescriptive tools.

Which Region to Dominate the Aviation Analytics Market?

North America to dominate the global market.

North America holds the dominant position with a 35% share, driven by advanced passenger data connectivity, the presence of major aerospace OEMs like Boeing and GE, and supportive FAA regulations on AI and cybersecurity; the United States stands as the dominating country, exemplified by airlines such as United and Alaska implementing predictive maintenance and route AI for operational gains amid high fleet volumes.

The Middle East exhibits the fastest growth, fueled by fleet expansions under initiatives like Vision 2030 and airport investments; Saudi Arabia dominates regionally, with carriers like Emirates and Qatar Airways adopting network-planning analytics, supported by seat capacity growth from 70 million in 2000 to 257 million in 2024.

Asia-Pacific shows multifaceted expansion, with rising domestic networks in China and India; China dominates, leveraging analytics for traffic management in rapidly urbanizing areas, while Japan and South Korea focus on integrating data from aging and new aircraft fleets.

Europe emphasizes regulatory-driven safety and sustainability analytics; Germany dominates, with Lufthansa Technik’s AI integrations highlighting MRO advancements, aided by GDPR-compliant data handling.

Latin America and Africa accelerate from lower bases, with currency challenges offset by targeted adoptions; Brazil dominates in Latin America via LATAM’s pricing intelligence, while Ethiopia leads in Africa through Ethiopian Airlines’ cloud-based maintenance logs.

Who are the Key Market Players in Aviation Analytics Market?

- Boeing focuses on divesting non-core analytics assets to prioritize manufacturing while securing long-term contracts for safety and maintenance insights, leveraging its engine digital twins for competitive edge.

- Safran pursues acquisitions like Preligens to bolster AI-driven autonomous analytics, expanding prescriptive capabilities in fleet management and positioning for eVTOL opportunities.

- GE Aerospace emphasizes platforms like FlightPulse and Safety Insight, using engine data for predictive insights that enhance fuel efficiency and safety, with strategies centered on proprietary algorithms and ecosystem lock-ins.

- SITA capitalizes on airline IT integrations to feed operational data into models, partnering for biometric solutions like luggage tracking to reduce mishandlings and drive real-time analytics adoption.

- Amadeus targets revenue and customer analytics through data monetization and open architectures, employing outcome-based pricing to attract diverse operators and foster unified data fabrics.

- Honeywell develops end-to-end suites for finance and operations, integrating IoT for real-time processing and hybrid architectures to address cyber risks.

- IBM provides cloud-based AI pipelines, focusing on skills training collaborations to overcome talent gaps and regulatory compliance tools for global scalability.

- SAP offers integrated business function analytics, bundling finance and supply chain modules with prescriptive features for disruption recovery.

- Oracle delivers scalable databases and analytics engines, emphasizing big data monetization and edge-AI for emerging eVTOL fleets.

What are the Market Trends in Aviation Analytics Market?

- Shift towards condition-based maintenance using predictive insights to optimize labor and inventory.

- Integration of AI for fuel efficiency, yielding 1-4.3% savings through dynamic routing.

- Monetization of anonymized data via benchmarking services for industry-wide improvements.

- Adoption of hybrid cloud architectures to mitigate cyber-risks while enabling real-time processing.

- Rise in prescriptive analytics for 15% cost reductions in disruption recovery.

- Emphasis on safety-performance metrics driven by regulations like FAA security rules.

- Use of computer-vision for enhanced baggage and passenger flow management.

What are the Market Segments and their Subsegments Covered in the Aviation Analytics Report?

By Analytics Type

-

Descriptive Analytics

-

Diagnostic Analytics

-

Predictive Analytics

-

Prescriptive Analytics

-

Real-time Analytics

-

Big Data Analytics

-

AI-based Analytics

-

Machine Learning Analytics

-

IoT Analytics

-

Cloud Analytics

-

Others

By Application

- Fuel Management

- Route Management

- Revenue Management

- Customer Analytics

- Inventory Management

- Maintenance Analytics

- Flight Risk Management

- Supply Chain Analytics

- Navigation Services

- Predictive Maintenance

- Others

By End-User

- Airlines

- Airports

- MRO Providers

- OEMs

- Cargo Operators

- Government Agencies

- Aviation Authorities

- Leasing Companies

- Ground Handlers

- Consultants

- Others

By Deployment

- On-premise

- Cloud

By Component

- Software

- Services

By Business Function

- Finance

- Operations

- Supply Chain

- Sales & Marketing

- Maintenance

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

Aviation analytics involve software and services for analyzing aviation data to improve efficiency, safety, and revenue in areas like flights, passengers, and operations.

Key factors include predictive maintenance adoption, fuel optimization needs, big data from aircraft sensors, safety regulations, and AI integration for real-time decisions.

The market is projected to grow from around USD 4.2 billion in 2026 to USD 11.6 billion by 2035.

The CAGR is expected to be 12% from 2026 to 2035.

North America will contribute notably, holding a dominant 35% share due to advanced infrastructure and OEM presence.

Major players include Boeing, Safran, GE Aerospace, SITA, Amadeus, Honeywell, IBM, SAP, and Oracle.

The report provides in-depth analysis of size, trends, segments, drivers, restraints, regional insights, key players, and forecasts.

Stages include data capture from sensors, storage and processing via platforms, analysis with AI tools, integration into operations, and insight delivery for decision-making.

Trends evolve towards AI-driven fuel savings, prescriptive disruption recovery, and hybrid clouds; preferences shift to outcome-based models and real-time safety analytics.

Factors include FAA security rules, GDPR privacy limits, and sustainability mandates pushing fuel and emissions analytics.