Anesthesia Equipment Market Size, Share and Trends 2026 to 2035

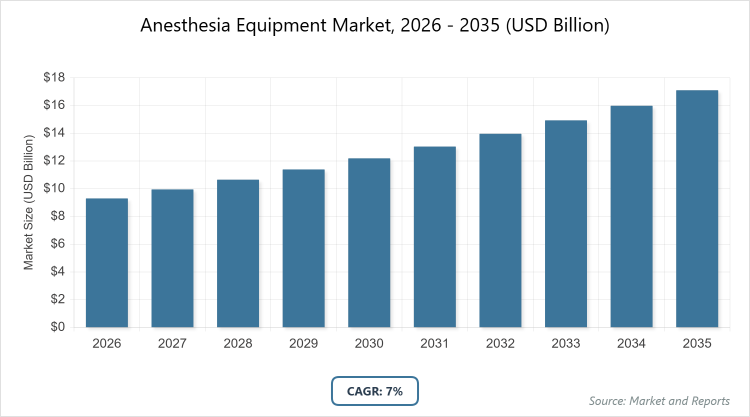

According to MarketnReports, the global Anesthesia Equipment market size was estimated at USD 9.3 billion in 2025 and is expected to reach USD 18.2 billion by 2035, growing at a CAGR of 7.0% from 2026 to 2035. Anesthesia Equipment Market is driven by rising surgical volumes, increasing prevalence of chronic diseases, and technological advancements in patient monitoring and safety features.

Key Insights

- The global Anesthesia Equipment market was valued at USD 9.3 billion in 2025 and is projected to reach USD 18.2 billion by 2035.

- The market is expected to grow at a CAGR of 7.0% from 2026 to 2035.

- The market is driven by rising surgical volumes worldwide, growing prevalence of chronic respiratory and cardiovascular diseases, and advancements in anesthesia delivery systems emphasizing patient safety and precision.

- Anesthesia Devices dominate the type segment with 29.4% share as they enable controlled anesthesia delivery, integrated ventilators, automated drug administration, and real-time monitoring, essential for complex surgeries and regulatory compliance.

- Respiratory Care dominates the application segment with 26.7% share due to high incidence of chronic respiratory disorders requiring ventilatory support, airway management, and precise monitoring to reduce perioperative risks.

- Hospitals dominate the end-user segment with 54.8% share owing to high concentration of surgical procedures, substantial budgets for advanced technologies, and integration in operating rooms and ICUs aligned with safety standards.

- North America dominates the global market due to high surgical volumes, rapid adoption of advanced technologies, strong healthcare infrastructure, and focus on patient safety innovations.

Industry Overview

The Anesthesia Equipment market encompasses a range of medical devices and disposables used to administer general or regional anesthesia during surgical procedures, critical care, and pain management. This includes anesthesia workstations, ventilators, monitors, breathing circuits, endotracheal tubes, and other accessories that ensure precise delivery of anesthetic agents, patient monitoring, and respiratory support. The market supports safe and effective anesthesia administration by minimizing complications, enhancing patient outcomes, and integrating with modern healthcare systems through innovations in digital monitoring, automation, and safety features. It plays a critical role in hospitals, clinics, and ambulatory settings where surgical interventions are performed.

Market Dynamics

Growth Drivers

The Anesthesia Equipment market experiences robust growth due to the increasing number of surgical procedures driven by rising cases of chronic diseases such as cancer, cardiovascular conditions, obesity, and neurological disorders. Technological advancements in anesthesia delivery systems, including automated drug dosing, real-time monitoring, and integrated ventilators, enhance patient safety and procedural efficiency. Regulatory emphasis on advanced safety features, growing healthcare infrastructure investments in emerging economies, and the shift toward minimally invasive surgeries further propel demand. Additionally, the expansion of ambulatory surgical centers and increasing accessibility of advanced devices in developing regions contribute significantly to market expansion.

Restraints

Market growth faces challenges from disruptions caused by public health crises, such as epidemics, which can limit elective surgeries, affect hospital procedures, and delay patient follow-ups. High costs associated with advanced equipment and the need for stringent regulatory compliance may also restrain adoption in resource-limited settings. Market fragmentation and potential stabilization post-pandemic recovery periods can impact consistent growth trajectories.

Opportunities

Significant opportunities arise from increasing research and development activities focused on innovative, portable, and energy-efficient anesthesia solutions. Government initiatives supporting healthcare modernization, foreign investments in low-cost manufacturing hubs, and rising awareness of patient safety create avenues for expansion. The growing aging population driving orthopedic and chronic disease-related surgeries, along with integration of digital technologies for enhanced clinical efficiency, offers substantial potential in emerging markets.

Challenges

The market contends with the need for continuous compliance with evolving safety regulations and standards, which can increase development costs. Perioperative complications, though mitigated by advanced equipment, remain a concern requiring ongoing innovation. High market fragmentation and competition among players also pose challenges in maintaining pricing power and market share.

Anesthesia Equipment Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Anesthesia Equipment Market |

| Market Size 2025 | USD 9.3 Billion |

| Market Forecast 2035 | USD 18.2 Billion |

| Growth Rate | CAGR of 7.0% |

| Report Pages | 220 |

| Key Companies Covered | GE Healthcare, Draegerwerk AG & Co KGaA, Philips Healthcare, Ambu A/S, Mindray, and Others |

| Segments Covered | By Type, By Application, By End User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

Market Segmentation

The Anesthesia Equipment market is segmented by type, application, end-user, and region.

Based on Type Segment, Anesthesia Devices hold the dominant position with a 29.4% share as they provide comprehensive solutions including workstations, ventilators, and monitors that facilitate precise anesthesia delivery, automated functions, and real-time patient monitoring, making them indispensable for complex procedures and safety compliance. Disposables rank as the second most dominant, including circuits and endotracheal tubes, driven by recurring demand in every procedure for hygiene, airway management, and infection control, supporting steady market growth through single-use applications.

Based on Application Segment, Respiratory Care leads with a 26.7% share due to the high prevalence of chronic respiratory conditions requiring ventilatory support, precise airway stability, and integrated monitoring during surgeries and critical care, significantly driving demand for related equipment. Orthopedics emerges as the second most dominant with strong growth potential from an aging population, rising accidents, and increasing joint/bone surgeries, boosting the need for reliable anesthesia support in these procedures.

Based on End-User Segment, Hospitals dominate with a 54.8% share as they perform the majority of surgeries, possess larger budgets for advanced technologies, and integrate equipment into operating rooms and ICUs, aligning with regulatory safety requirements and high patient volumes. Clinics and Ambulatory Surgical Centers follow, gaining traction from the shift toward outpatient procedures and cost-effective care settings.

Recent Developments

- In May 2025, Fisher & Paykel Healthcare Corporation Limited launched Optiflow Switch and Optiflow Trace nasal high-flow interface devices tailored for anesthesia applications, enhancing patient comfort and respiratory support during procedures.

- In February 2025, Mindray introduced the A8 and A9 anesthesia workstations to advance perioperative care through improved usability and performance features.

- In 2025, Mindray released the A9 Anesthesia Workstation equipped with a large touchscreen display, built-in vaporizer, and advanced monitoring capabilities to elevate anesthesia delivery precision.

Regional Analysis

North America to dominate the global market

North America leads the Anesthesia Equipment market with strong growth fueled by high surgical volumes, advanced healthcare infrastructure, rapid adoption of technological innovations, and emphasis on patient safety standards, particularly in the United States with a 7.1% CAGR driven by R&D investments and increasing procedures.

Europe exhibits steady expansion supported by well-established healthcare systems, regulatory focus on safety, and rising demand for advanced monitoring, with countries like the United Kingdom showing an 8.0% CAGR due to robust infrastructure and emergency care needs.

Asia Pacific demonstrates the fastest growth potential from booming healthcare infrastructure, government initiatives, low manufacturing costs, and rising chronic diseases, with China at 7.7% CAGR from foreign investments and orthopedic awareness, and Japan at 7.5% CAGR from aging population-driven surgeries.

Latin America and Middle East & Africa show emerging growth through improving healthcare access, increasing surgical needs, and investments in medical technology, though at a slower pace compared to developed regions.

Key Market Players and Strategies of each

- GE Healthcare focuses on innovation in anesthesia workstations and monitoring systems, leveraging strong global presence and partnerships for technology integration and market expansion.

- Draegerwerk AG & Co KGaA emphasizes safety-focused ventilators and anesthesia delivery solutions, investing in R&D to meet regulatory standards and enhance patient outcomes.

- Philips Healthcare prioritizes advanced monitoring and digital integration in anesthesia equipment, pursuing strategic collaborations to improve clinical efficiency and expand in emerging markets.

- Ambu A/S specializes in single-use disposables like endotracheal tubes and circuits, driving growth through hygiene-focused innovations and cost-effective offerings for hospitals and ambulatory settings.

- Mindray advances through recent launches of next-generation workstations, targeting perioperative care improvements and global market penetration with user-friendly, high-tech solutions.

Market Trends

- Integration of digital technologies and automation for enhanced monitoring and clinical efficiency.

- Rising demand for portable and energy-efficient anesthesia equipment in diverse settings.

- Increased focus on patient safety features and regulatory-compliant designs.

- Growing adoption in ambulatory surgical centers and outpatient procedures.

- Expansion driven by chronic disease prevalence and aging populations requiring more surgeries.

Market Segments and their subsegment Covered in the Report

By Type

- Anesthesia Devices

- Workstation

- Ventilators

- Monitors

- Disposables

- Circuits

- Endotracheal Tubes

- Others

By Application

- Respiratory Care

- Orthopedics

- Neurology

- Urology

- Cardiology

- Other

By End User

- Hospitals

- Clinics

- Ambulatory Surgical Centers

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global Anesthesia Equipment Market, (2026 - 2035) (USD Billion)2.2 Global Anesthesia Equipment Market: SnapshotChapter 3. Global Anesthesia Equipment Market - Industry Analysis

3.1 Anesthesia Equipment Market: Market Dynamics3.2 Market Drivers3.2.1 The anesthesia equipment market is growing due to rising surgical volumes, technological advancements in safety and automation, expanding healthcare infrastructure, growth of minimally invasive procedures, and increasing demand from ambulatory surgical centers.3.3 Market Restraints3.3.1 The anesthesia equipment market faces challenges from disruptions to elective surgeries during public health crises, high costs of advanced devices, strict regulatory requirements, and inconsistent growth in post-pandemic recovery phases.3.4 Market Opportunities3.4.1 The anesthesia equipment market offers strong opportunities through R&D in portable and energy-efficient technologies, healthcare modernization initiatives, low-cost manufacturing expansion, digital integration, and rising surgical demand from aging populations in emerging markets.3.5 Market Challenges3.5.1 The anesthesia equipment market faces challenges from evolving regulatory compliance requirements, perioperative safety risks, high market fragmentation, and intense competition that pressures pricing and market share.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Type3.7.2 Market Attractiveness Analysis By Application3.7.3 Market Attractiveness Analysis By End UserChapter 4. Global Anesthesia Equipment Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global Anesthesia Equipment Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global Anesthesia Equipment Market - Type Analysis

5.1 Global Anesthesia Equipment Market Overview: Type5.1.1 Global Anesthesia Equipment Market share, By Type, 2025 and 20355.2 Anesthesia Devices5.2.1 Global Anesthesia Equipment Market by Anesthesia Devices, 2026 - 2035 (USD Billion)5.3 Disposables5.3.1 Global Anesthesia Equipment Market by Disposables, 2026 - 2035 (USD Billion)Chapter 6. Global Anesthesia Equipment Market - Application Analysis

6.1 Global Anesthesia Equipment Market Overview: Application6.1.1 Global Anesthesia Equipment Market Share, By Application, 2025 and 20356.2 Respiratory Care6.2.1 Global Anesthesia Equipment Market by Respiratory Care, 2026 - 2035 (USD Billion)6.3 Orthopedics6.3.1 Global Anesthesia Equipment Market by Orthopedics, 2026 - 2035 (USD Billion)6.4 Neurology6.4.1 Global Anesthesia Equipment Market by Neurology, 2026 - 2035 (USD Billion)6.5 Urology6.5.1 Global Anesthesia Equipment Market by Urology, 2026 - 2035 (USD Billion)6.6 Cardiology6.6.1 Global Anesthesia Equipment Market by Cardiology, 2026 - 2035 (USD Billion)6.7 Other6.7.1 Global Anesthesia Equipment Market by Other, 2026 - 2035 (USD Billion)Chapter 7. Global Anesthesia Equipment Market - End User Analysis

7.1 Global Anesthesia Equipment Market Overview: End User7.1.1 Global Anesthesia Equipment Market Share, By End User, 2025 and 20357.2 Hospitals7.2.1 Global Anesthesia Equipment Market by Hospitals, 2026 - 2035 (USD Billion)7.3 Clinics7.3.1 Global Anesthesia Equipment Market by Clinics, 2026 - 2035 (USD Billion)7.4 Ambulatory Surgical Centers7.4.1 Global Anesthesia Equipment Market by Ambulatory Surgical Centers, 2026 - 2035 (USD Billion)Chapter 8. Anesthesia Equipment Market - Regional Analysis

8.1 Global Anesthesia Equipment Market Regional Overview8.2 Global Anesthesia Equipment Market Share, by Region, 2025 & 2035 (USD Billion)8.3 North America8.3.1 North America Anesthesia Equipment Market, 2026 - 2035 (USD Billion)8.3.1.1 North America Anesthesia Equipment Market, by Country, 2026 - 2035 (USD Billion)8.3.2 North America Anesthesia Equipment Market, by Type, 2026 - 20358.3.2.1 North America Anesthesia Equipment Market, by Type, 2026 - 2035 (USD Billion)8.3.3 North America Anesthesia Equipment Market, by Application, 2026 - 20358.3.3.1 North America Anesthesia Equipment Market, by Application, 2026 - 2035 (USD Billion)8.3.4 North America Anesthesia Equipment Market, by End User, 2026 - 20358.3.4.1 North America Anesthesia Equipment Market, by End User, 2026 - 2035 (USD Billion)8.4 Europe8.4.1 Europe Anesthesia Equipment Market, 2026 - 2035 (USD Billion)8.4.1.1 Europe Anesthesia Equipment Market, by Country, 2026 - 2035 (USD Billion)8.4.2 Europe Anesthesia Equipment Market, by Type, 2026 - 20358.4.2.1 Europe Anesthesia Equipment Market, by Type, 2026 - 2035 (USD Billion)8.4.3 Europe Anesthesia Equipment Market, by Application, 2026 - 20358.4.3.1 Europe Anesthesia Equipment Market, by Application, 2026 - 2035 (USD Billion)8.4.4 Europe Anesthesia Equipment Market, by End User, 2026 - 20358.4.4.1 Europe Anesthesia Equipment Market, by End User, 2026 - 2035 (USD Billion)8.5 Asia Pacific8.5.1 Asia Pacific Anesthesia Equipment Market, 2026 - 2035 (USD Billion)8.5.1.1 Asia Pacific Anesthesia Equipment Market, by Country, 2026 - 2035 (USD Billion)8.5.2 Asia Pacific Anesthesia Equipment Market, by Type, 2026 - 20358.5.2.1 Asia Pacific Anesthesia Equipment Market, by Type, 2026 - 2035 (USD Billion)8.5.3 Asia Pacific Anesthesia Equipment Market, by Application, 2026 - 20358.5.3.1 Asia Pacific Anesthesia Equipment Market, by Application, 2026 - 2035 (USD Billion)8.5.4 Asia Pacific Anesthesia Equipment Market, by End User, 2026 - 20358.5.4.1 Asia Pacific Anesthesia Equipment Market, by End User, 2026 - 2035 (USD Billion)8.6 Latin America8.6.1 Latin America Anesthesia Equipment Market, 2026 - 2035 (USD Billion)8.6.1.1 Latin America Anesthesia Equipment Market, by Country, 2026 - 2035 (USD Billion)8.6.2 Latin America Anesthesia Equipment Market, by Type, 2026 - 20358.6.2.1 Latin America Anesthesia Equipment Market, by Type, 2026 - 2035 (USD Billion)8.6.3 Latin America Anesthesia Equipment Market, by Application, 2026 - 20358.6.3.1 Latin America Anesthesia Equipment Market, by Application, 2026 - 2035 (USD Billion)8.6.4 Latin America Anesthesia Equipment Market, by End User, 2026 - 20358.6.4.1 Latin America Anesthesia Equipment Market, by End User, 2026 - 2035 (USD Billion)8.7 The Middle-East and Africa8.7.1 The Middle-East and Africa Anesthesia Equipment Market, 2026 - 2035 (USD Billion)8.7.1.1 The Middle-East and Africa Anesthesia Equipment Market, by Country, 2026 - 2035 (USD Billion)8.7.2 The Middle-East and Africa Anesthesia Equipment Market, by Type, 2026 - 20358.7.2.1 The Middle-East and Africa Anesthesia Equipment Market, by Type, 2026 - 2035 (USD Billion)8.7.3 The Middle-East and Africa Anesthesia Equipment Market, by Application, 2026 - 20358.7.3.1 The Middle-East and Africa Anesthesia Equipment Market, by Application, 2026 - 2035 (USD Billion)8.7.4 The Middle-East and Africa Anesthesia Equipment Market, by End User, 2026 - 20358.7.4.1 The Middle-East and Africa Anesthesia Equipment Market, by End User, 2026 - 2035 (USD Billion)Chapter 9. Company Profiles

9.1 GE Healthcare9.1.1 Overview9.1.2 Financials9.1.3 Product Portfolio9.1.4 Business Strategy9.1.5 Recent Developments9.2 Draegerwerk AG & Co KGaA9.2.1 Overview9.2.2 Financials9.2.3 Product Portfolio9.2.4 Business Strategy9.2.5 Recent Developments9.3 Philips Healthcare9.3.1 Overview9.3.2 Financials9.3.3 Product Portfolio9.3.4 Business Strategy9.3.5 Recent Developments9.4 Ambu A/S9.4.1 Overview9.4.2 Financials9.4.3 Product Portfolio9.4.4 Business Strategy9.4.5 Recent Developments9.5 Mindray9.5.1 Overview9.5.2 Financials9.5.3 Product Portfolio9.5.4 Business Strategy9.5.5 Recent Developments

Frequently Asked Questions

Anesthesia Equipment refers to medical devices and disposables used to administer anesthesia, monitor patients, and support respiration during surgical and critical care procedures, including workstations, ventilators, monitors, circuits, and endotracheal tubes.

Key factors include rising surgical volumes, increasing chronic diseases, technological advancements in monitoring and delivery systems, healthcare infrastructure expansion, and regulatory emphasis on patient safety.

The market is projected to grow from USD 9.3 billion in 2025 to USD 18.2 billion by 2035, reflecting sustained expansion over the forecast period.

The market is expected to grow at a CAGR of 7.0% during the period.

North America will contribute notably due to high surgical volumes and technology adoption, with Asia Pacific showing rapid growth from infrastructure development.

Major players include GE Healthcare, Draegerwerk AG & Co KGaA, Philips Healthcare, Ambu A/S, and Mindray.

The report provides comprehensive analysis of market size, trends, segmentation, dynamics, regional insights, competitive landscape, and forecasts to guide strategic decisions.

The value chain includes raw material sourcing, component manufacturing, device assembly, regulatory approval, distribution to healthcare facilities, usage in procedures, and after-sales support and maintenance.

Trends show a shift toward digital integration, safety-enhanced devices, single-use disposables for infection control, and portable solutions, with preferences favoring precision, efficiency, and patient outcomes.

Strict safety regulations, standards for device performance, and compliance requirements drive adoption of advanced features, while environmental concerns push for energy-efficient and sustainable designs.