Amphibious Excavators Market Size, Share and Trends 2026 to 2035

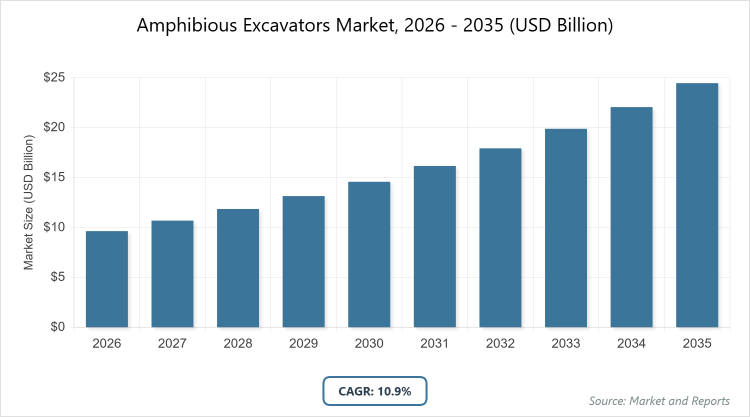

According to MarketReports, the global amphibious excavators market size was estimated at USD 9.64 billion in 2026 and is expected to reach USD 24.46 billion by 2035, growing at a CAGR of 10.9% from 2026 to 2035. The global amphibious excavators market is primarily driven by rising investments in dredging, wetland restoration, and flood control projects, fueled by the need for specialized machinery that can operate efficiently in challenging terrains like swamps, marshes, and shallow water.

What are the Key Insights into the Amphibious Excavators Market?

- The global amphibious excavators market is projected to grow from approximately USD 9.64 billion in 2026 to USD 24.46 billion by 2035, reflecting a compound annual growth rate (CAGR) of around 10.9%.

- Among types, medium amphibious excavators dominate as the leading subsegment, holding over 55% market share for their versatility in various projects.

- In application segments, dredging holds the dominant position, accounting for around 28% share due to extensive use in waterway maintenance.

- By end-use, construction is the most prominent, driven by infrastructure and land reclamation demands.

- Asia Pacific emerges as the dominant region, contributing over 43% market share, owing to rapid development and environmental projects.

What is the Amphibious Excavators Industry?

Industry Overview

The amphibious excavators industry encompasses specialized heavy machinery designed for operations in both terrestrial and aquatic environments, featuring floating undercarriages or pontoons that enable excavation, dredging, and material handling in wetlands, rivers, lakes, and coastal areas without sinking. These machines integrate standard excavator components like booms, arms, and buckets with amphibious adaptations for buoyancy and propulsion, catering to applications in construction, environmental remediation, mining, and disaster relief where traditional equipment cannot access soft or waterlogged terrains.

Serving as a niche segment within the construction equipment sector, the market emphasizes durability, versatility, and efficiency, incorporating advancements in hydraulics, materials, and remote controls to minimize environmental impact while enhancing productivity in challenging conditions, ultimately supporting infrastructure development, flood management, and ecological restoration amid global climate challenges and urbanization pressures.

What Drives the Amphibious Excavators Market?

Growth Drivers

The amphibious excavators market is propelled by escalating demand for wetland restoration and flood control projects, driven by climate change impacts and urbanization that necessitate efficient machinery for inaccessible terrains, coupled with government investments in infrastructure like ports, canals, and coastal defenses.

Technological innovations, such as GPS integration, remote operation, and hybrid power systems, improve precision and safety, attracting adoption in mining and oil & gas sectors for pipeline installation and site preparation. Additionally, rising environmental regulations promoting sustainable land reclamation and disaster relief efforts boost market penetration, as these excavators offer reduced soil disturbance and faster project completion compared to conventional methods.

Restraints

High initial costs and maintenance requirements for specialized components like pontoons and corrosion-resistant materials limit affordability, particularly for small contractors in developing regions facing budget constraints. Limited skilled operators and training infrastructure hinder widespread use, while competition from alternative solutions like barges or standard excavators with attachments erodes market share in less challenging environments. Furthermore, supply chain vulnerabilities for custom parts and fluctuating raw material prices increase operational expenses, restraining growth amid economic uncertainties.

Opportunities

The expansion of renewable energy projects, such as offshore wind farms and hydroelectric dams, presents avenues for amphibious excavators in site preparation and maintenance, appealing to green initiatives with low-impact designs. Emerging markets in Asia and Africa offer untapped potential through infrastructure booms and natural resource extraction, where localized manufacturing and rentals can capture demand. Moreover, advancements in electric and autonomous models align with sustainability trends, enabling premium offerings and partnerships with governments for environmental projects.

Challenges

Stringent safety and environmental standards require ongoing R&D investments, complicating compliance across regions and elevating costs for manufacturers. Intense weather conditions and terrain variability test equipment reliability, leading to downtime and repair issues in remote operations. Additionally, geopolitical tensions disrupting global trade affect component availability, while addressing operator safety in hazardous waters demands innovative features without compromising affordability.

Amphibious Excavators Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Amphibious Excavators Market |

| Market Size 2025 | USD 9.64 Billion |

| Market Forecast 2035 | USD 24.46 Billion |

| Growth Rate | CAGR of 10.9% |

| Report Pages | 220 |

| Key Companies Covered | Hitachi Construction Machinery Co., Ltd, Liebherr-International AG, Volvo Construction Equipment AB, Aquarius Systems, Wetland Equipment, Wilco Manufacturing, L.L.C, and Ultratrex Machinery Sdn. Bhd |

| Segments Covered | By Type, By Application, By End-Use, By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Amphibious Excavators Market Segmented?

The amphibious excavators market is segmented by type, application, end-use, and region.

By type, including small, medium, and large, with medium emerging as the most dominant due to its optimal balance of power, maneuverability, and cost-effectiveness for weights between 20-35 tons, ideal for dredging and land reclamation in diverse terrains; this dominance drives the market by enabling high-volume adoption in infrastructure projects and commanding significant revenue through widespread utility, while small ranks as the second most dominant, valued for its agility in lighter tasks like stump removal and small excavations under 19 tons, supporting growth via accessibility for smaller contractors and niche applications.

By application, the market divides into dredging, highway construction, oil & gas pipeline installation, environmental restoration, and others, where dredging dominates owing to its essential role in sediment removal for navigation and flood prevention, fueled by global water management needs; its prevalence propels market expansion by integrating with large-scale environmental and infrastructure initiatives, whereas highway construction follows as the second dominant, critical for remote area access and cost-efficient building, contributing through rising investments in transportation networks.

By end-use, segments include construction, mining, oil & gas, and others, with construction leading as it encompasses broad applications in site preparation and reclamation, driven by urbanization; this segment fuels overall dynamics by generating consistent demand and fostering innovations in durable designs, while oil & gas secures second place, utilized for pipeline laying in marshy areas, enhancing market resilience through energy sector expansions.

What are the Recent Developments in the Amphibious Excavators Market?

- In April 2023, Hawk Excavator launched new long-reach arms and amphibious undercarriages equipped with RTK GPS technology, designed for heavy-duty excavation in lakes, construction, and mining, aiming to improve precision and efficiency in challenging environments.

- In February 2024, the Provincial Engineer’s Office in Lanao del Norte, Philippines, commissioned a new amphibious excavator for dredging silted shores and rivers, highlighting increased governmental focus on flood control and waterway maintenance in flood-prone regions.

- In 2025, Wetland Equipment introduced an upgraded model with enhanced corrosion-resistant materials and hybrid power options, targeting environmental restoration projects to align with sustainability goals and expand market presence in eco-sensitive areas.

How Does Regional Performance Vary in the Amphibious Excavators Market?

- Asia Pacific to dominate the market

Asia Pacific dominates the amphibious excavators market, fueled by extensive infrastructure initiatives like China’s Belt and Road and India’s rural road programs, alongside frequent flooding and wetland projects; China leads this region with its massive manufacturing capabilities, high demand from urban development and mining, and government subsidies for environmental equipment, driving innovation in cost-effective models while exporting to neighboring countries. India follows with rapid growth from dam and canal constructions, supported by schemes like PMGSY, enhancing accessibility in rural areas.

North America exhibits steady growth, supported by land reclamation and disaster relief efforts in flood-prone zones; the United States predominates with its advanced R&D ecosystem, presence of key manufacturers like Wetland Equipment, and investments in coastal infrastructure, fostering adoption in mining and oil & gas. Canada contributes through pipeline projects in marshy terrains, with emphasis on sustainable mining practices.

Europe maintains a mature market, influenced by stringent environmental regulations and restoration projects; Germany stands out as the dominating country, leveraging engineering expertise for high-quality, eco-compliant models and exports, while focusing on riverbank stabilization and wetland preservation. The UK and France add momentum through flood defense initiatives and heritage site maintenances.

Latin America shows emerging potential, driven by mining and agricultural expansions in wetland areas; Brazil leads with its Amazonian projects and infrastructure upgrades, promoting durable equipment for remote operations amid economic growth. Mexico supports regional dynamics through oil exploration in coastal regions.

The Middle East & Africa region represents nascent opportunities, focused on oil & gas and desalination projects; the United Arab Emirates dominates via luxury coastal developments and investments in flood control, with Saudi Arabia advancing through Vision 2030’s infrastructure push in arid-wetland interfaces.

Who are the Key Market Players in the Amphibious Excavators Industry?

- Hitachi Construction Machinery Co., Ltd. invests in hybrid technologies and global partnerships to enhance durability for dredging applications.

- Liebherr-International AG focuses on customization and R&D for corrosion-resistant models, targeting European environmental projects.

- Volvo Construction Equipment AB emphasizes sustainability with electric variants and service networks for mining sectors.

- Aquarius Systems prioritizes lightweight designs and acquisitions for expansion in wetland restoration.

- Wetland Equipment adopts innovation in pontoon systems and collaborations for disaster relief equipment.

- Wilco Manufacturing, L.L.C. leverages cost-effective undercarriages and regional manufacturing for oil & gas markets.

- Ultratrex Machinery Sdn. Bhd. pursues affordable custom models and exports to emerging Asian economies.

What are the Current Market Trends in Amphibious Excavators?

- Increasing integration of GPS and telematics for precision in dredging and remote operations.

- Shift toward hybrid and electric models to reduce emissions in eco-sensitive areas.

- Growth in long-reach arms for extended access in deep water excavations.

- Adoption of autonomous features for enhanced safety in hazardous environments.

- Expansion of rental services to lower entry barriers for small projects.

- Focus on lightweight materials to improve mobility and fuel efficiency.

- Rise in customized attachments for specialized tasks like pipeline installation.

What Market Segments are Covered in the Report?

By Type

- Small

- Medium

- Large

By Application

- Dredging

- Highway Construction

- Oil & Gas Pipeline Installation

- Environmental Restoration

- Others

By End-Use

- Construction

- Mining

- Oil & Gas

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Amphibious excavators are specialized construction machines equipped with floating undercarriages for operations in water and soft terrains, used for excavation, dredging, and material handling.

Key factors include climate-driven flood control projects, infrastructure investments, technological advancements in hybrid systems, and environmental regulations.

The market is projected to grow from approximately USD 9.64 billion in 2026 to USD 24.46 billion by 2035, driven by global infrastructure demands.

The compound annual growth rate (CAGR) is expected to be around 10.9% from 2026 to 2035, indicating strong expansion.

Asia Pacific will contribute notably, holding the largest share due to extensive wetland and infrastructure projects.

Hitachi Construction Machinery Co., Ltd, Liebherr-International AG, Volvo Construction Equipment AB, Aquarius Systems, Wetland Equipment, Wilco Manufacturing, L.L.C, and Ultratrex Machinery Sdn. Bhd

The report provides insights into size, trends, segmentation, regional analysis, players, and forecasts for strategic decisions.

Stages include raw material sourcing, component manufacturing, assembly, distribution, and after-sales services like maintenance.

Trends are evolving toward sustainable, tech-integrated models, with preferences for versatile, efficient equipment in environmental applications.

Regulations on emissions drive hybrid innovations, while environmental concerns boost demand for low-impact machines but increase compliance costs.