Active Wound Care Market Size, Share and Trends 2026 to 2035

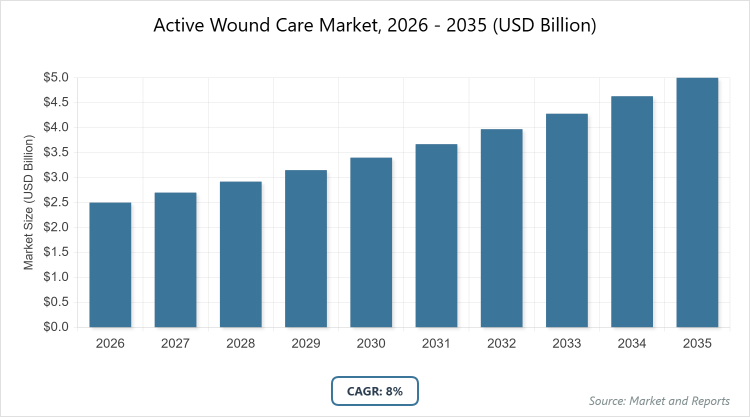

According to MarketnReports, the global Active Wound Care Market size was estimated at USD 2.5 Billion in 2025 and is expected to reach USD 5.3 Billion by 2035, growing at a CAGR of 8% from 2026 to 2035. Active Wound Care Market is driven by increasing prevalence of chronic wounds and advancements in regenerative medicine.

What is the Industry Overview of Active Wound Care Market?

The active wound care market encompasses advanced therapeutic interventions designed to promote faster and more effective healing of complex wounds through biological and technological means. This market focuses on products that actively participate in the healing process, such as skin substitutes, growth factors, and biomaterials, rather than passive coverings. Market definition includes biologics, tissue-engineered products, and other innovative solutions aimed at addressing chronic and acute wounds that do not respond well to traditional methods, catering to patients with conditions like diabetes, ulcers, and burns.

What are the Key Insights into Active Wound Care Market?

- The global active wound care market was valued at USD 2.5 billion in 2025 and is projected to reach USD 5.3 billion by 2035.

- The market is anticipated to grow at a CAGR of 8% during the forecast period from 2026 to 2035.

- The market is driven by the rising incidence of chronic diseases such as diabetes, an aging population, and technological innovations in regenerative therapies.

- Biological skin equivalents dominate the product segment with a 40% share due to their effectiveness in mimicking natural skin structure and accelerating tissue regeneration in severe wounds.

- Chronic wounds dominate the application segment with a 60% share as they require advanced interventions to manage prolonged healing times associated with underlying health conditions.

- Hospitals dominate the end-user segment with a 50% share owing to their advanced facilities and high volume of complex wound cases requiring specialized care.

- North America dominates the regional segment with a 45% share attributed to its robust healthcare infrastructure, high prevalence of diabetes, and strong adoption of innovative medical technologies.

What are the Market Dynamics of Active Wound Care Market?

Growth Drivers

The growth drivers of the active wound care market are primarily fueled by the escalating global burden of chronic diseases, particularly diabetes, which leads to a higher incidence of non-healing wounds like diabetic foot ulcers. Advancements in biotechnology, including the development of bioengineered skin substitutes and growth factor therapies, have significantly improved healing outcomes, reducing amputation rates and hospital stays. Additionally, an aging population worldwide increases susceptibility to pressure ulcers and venous leg ulcers, driving demand for effective active treatments. Government initiatives and increased healthcare spending in emerging economies further support market expansion by improving access to advanced wound care solutions.

Restraints

Restraints in the active wound care market include the high cost of advanced products such as biological skin equivalents and tissue-engineered therapies, which limit accessibility in low-income regions and for uninsured patients. Reimbursement challenges and varying insurance coverage for these innovative treatments also hinder widespread adoption, as healthcare providers may opt for cheaper traditional options. Moreover, stringent regulatory approvals for biologics and potential risks like immune rejection or infection complicate market entry for new products, slowing innovation and increasing development expenses for manufacturers.

Opportunities

Opportunities in the active wound care market arise from the growing emphasis on home-based care and telemedicine, enabling remote monitoring and self-administration of treatments, which can expand market reach in underserved areas. Emerging markets in Asia-Pacific and Latin America present untapped potential due to rising healthcare awareness and improving infrastructure. Innovations in AI-integrated wound assessment tools and personalized regenerative medicine offer avenues for product differentiation and improved efficacy. Partnerships between key players and research institutions could accelerate the development of cost-effective, next-generation therapies to address unmet needs in chronic wound management.

Challenges

Challenges facing the active wound care market involve the complexity of wound healing processes, which vary by patient, making standardized treatments less effective and requiring tailored approaches that increase costs and training needs. Supply chain disruptions for biological materials, such as donor tissues for allografts, can lead to shortages and price volatility. Additionally, lack of skilled healthcare professionals in wound care management, especially in rural areas, impedes proper application of active products. Environmental concerns over biohazard waste from biologics and ethical issues in sourcing animal-derived xenografts further complicate market growth.

Active Wound Care Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Active Wound Care Market |

| Market Size 2025 | USD 2.5 Billion |

| Market Forecast 2035 | USD 5.3 Billion |

| Growth Rate | CAGR of 8% |

| Report Pages | 220 |

| Key Companies Covered |

Organogenesis, MiMedx, Integra LifeSciences, Smith+Nephew, Solventum, Convatec Group, and Others |

| Segments Covered | By Product, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Active Wound Care Market?

The Active Wound Care Market is segmented by product, application, end-user, and region. All the segments have been analyzed based on present and future trends and the market is estimated from 2026 to 2035.

Based on Product Segment, biological skin equivalents emerge as the most dominant subsegment, holding approximately 40% market share, while growth factors rank as the second most dominant with around 25%. Biological skin equivalents dominate due to their ability to provide a scaffold for cell migration and vascularization, effectively treating large or deep wounds that traditional methods cannot heal, thereby driving market growth through reduced healing time and lower complication rates; growth factors, as the second dominant, enhance cellular proliferation and angiogenesis, supporting overall market expansion by complementing other therapies in accelerating wound closure for chronic cases.

Based on Application Segment, diabetic foot ulcers stand out as the most dominant subsegment with about 35% share, followed by pressure ulcers as the second most dominant at roughly 20%. Diabetic foot ulcers dominate because of the global rise in diabetes prevalence, necessitating specialized active care to prevent amputations and manage infection risks, which propels market growth by increasing demand for targeted biologics; pressure ulcers, the second dominant, arise from prolonged immobility in elderly or bedridden patients, driving the market through the need for preventive and regenerative solutions that improve patient outcomes and reduce healthcare burdens.

Based on End-User Segment, hospitals are the most dominant subsegment, capturing nearly 50% share, with home care settings as the second most dominant at approximately 20%. Hospitals dominate owing to their equipped facilities for handling severe wounds and performing advanced procedures, fueling market growth by serving as primary centers for initial treatment and innovation adoption; home care settings, the second dominant, gain traction from the shift toward outpatient care and cost savings, contributing to market expansion by enabling continued therapy post-discharge and improving accessibility for chronic wound patients.

What are the Recent Developments in Active Wound Care Market?

- In November 2025, Solventum announced its agreement to acquire Acera Surgical, a company specializing in synthetic treatment options for soft tissue repair, enhancing Solventum’s portfolio in advanced wound management; the acquisition was completed in December 2025, aiming to integrate Acera’s innovative nanotechnology-based scaffolds to improve healing outcomes for complex wounds.

- In December 2025, New Horizon Medical Solutions acquired the business assets of Applied Tissue Technologies, including transparent negative pressure wound therapy devices and micro grafting kits, to bolster its wound care offerings and provide more comprehensive solutions for chronic wound patients.

- In October 2025, Smith+Nephew launched the ALLEVYN COMPLETE CARE Foam Dressing, demonstrated to absorb 93% of mechanical energy for pressure injury prevention, marking a significant advancement in proactive wound care.

- In September 2025, Smith+Nephew introduced the CENTRIO PRP System in the U.S., designed to support regenerative healing in wounds through platelet-rich plasma technology.

- In July 2025, Zimmer Biomet acquired Monogram Technologies, gaining access to AI-navigated robotic systems for orthopaedic applications that intersect with wound care in post-surgical healing.

- In March 2025, Mölnlycke Health Care completed the acquisition of P.G.F. Industry Solutions GmbH, adding Granudacyn wound cleansing solutions to its portfolio for enhanced infection management in active wound care.

What is the Regional Analysis of Active Wound Care Market?

North America to dominate the global market.

North America holds the dominant position in the active wound care market, driven by advanced healthcare systems and high diabetes rates, with the United States as the leading country due to its extensive research funding, widespread adoption of biologics, and strong presence of key players like Organogenesis, which facilitate rapid innovation and market penetration.

Europe follows as a significant region, benefiting from robust regulatory frameworks and aging populations, where Germany stands out as the dominating country owing to its advanced medical technology sector and government-supported healthcare initiatives that promote the use of tissue-engineered products for chronic wound treatment.

Asia-Pacific is experiencing rapid growth due to increasing healthcare investments and rising chronic disease prevalence, with China as the dominating country propelled by its large patient pool, expanding manufacturing capabilities, and government policies aimed at improving access to regenerative therapies.

Latin America shows emerging potential with improving healthcare access and awareness, led by Brazil as the dominating country through its focus on public health programs addressing diabetes-related wounds and partnerships with international firms for technology transfer.

The Middle East and Africa region is gradually expanding, supported by infrastructure developments, with South Africa as the dominating country due to its relatively advanced medical facilities and efforts to combat infectious wounds through imported active care solutions.

What are the Key Market Players in Active Wound Care Market?

Organogenesis is a leading player in the active wound care market, focusing on regenerative medicine with products like Apligraf and NuShield; its strategies include heavy investment in clinical trials to demonstrate efficacy, strategic partnerships with hospitals for product integration, and expansion into emerging markets to capture growing demand for biological skin substitutes.

MiMedx specializes in amniotic tissue-based products such as EpiFix, employing strategies like robust R&D for new allograft applications, acquisitions to broaden its portfolio, and targeted marketing to wound care specialists to enhance adoption in chronic wound treatments.

Integra LifeSciences offers a range of dermal regeneration templates and growth factors, with strategies centered on mergers and acquisitions for technology enhancement, global distribution network expansion, and collaboration with research institutions to innovate in tissue engineering.

Smith+Nephew provides advanced biologics and wound management systems, utilizing strategies such as product launches for pressure injury prevention, investments in digital health for wound monitoring, and acquisitions to strengthen its regenerative portfolio.

Solventum focuses on nanotechnology-based scaffolds post its acquisition of Acera Surgical, with strategies including integration of acquired technologies for soft tissue repair, emphasis on home care solutions, and partnerships for clinical validation to drive market share growth.

Convatec Group delivers growth factor therapies and skin substitutes, employing strategies like portfolio diversification through R&D, regional expansions in Asia-Pacific, and sustainability initiatives in product development to meet evolving regulatory demands.

What are the Market Trends in Active Wound Care Market?

- Integration of AI and digital tools for personalized wound assessment and remote monitoring to improve treatment outcomes.

- Rise in regenerative therapies using stem cells and 3D bioprinting for custom skin substitutes.

- Shift toward home-based care solutions with user-friendly active wound products to reduce hospital visits.

- Growing focus on sustainable and bioresorbable materials to address environmental concerns in biologics.

- Expansion of telemedicine platforms for wound care consultations in underserved regions.

- Increased adoption of combination therapies blending growth factors with biomaterials for enhanced healing.

- Emphasis on cost-effective innovations to make active care accessible in emerging markets.

What Market Segments and their Subsegments are Covered in the Active Wound Care Report?

- By Product

- Allografts

- Xenografts

- Collagen Products

- Growth Factors

- Biological Dressings

- Synthetic Skin Substitutes

- Cell-based Therapies

- Tissue Engineered Products

- Topical Agents

- Stem Cell Therapies

- Others

- By Application

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Leg Ulcers

- Surgical Wounds

- Burns

- Trauma Wounds

- Arterial Ulcers

- Chronic Leg Ulcers

- Skin Grafts

- Infectious Wounds

- Others

By End-User

-

- Hospitals

- Specialty Clinics

- Home Care Settings

- Ambulatory Surgical Centers

- Nursing Homes

- Wound Care Centers

- Physician Offices

- Long-term Care Facilities

- Research Institutes

- Rehabilitation Centers

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Active Wound Care Market - Industry Analysis

Chapter 4. Global Active Wound Care Market- Competitive Landscape

Chapter 5. Global Active Wound Care Market - Product Analysis

Chapter 6. Global Active Wound Care Market - Application Analysis

Chapter 7. Global Active Wound Care Market - End-User Analysis

Chapter 8. Active Wound Care Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

The active wound care market refers to the sector focused on advanced products and therapies that actively promote wound healing through biological mechanisms, including skin substitutes, growth factors, and tissue-engineered solutions for chronic and acute wounds.

Key factors include rising chronic disease prevalence, technological advancements in regenerative medicine, an aging population, increasing surgical procedures, and expanding healthcare access in emerging regions.

The market was valued at USD 2.5 billion in 2025 and is projected to reach USD 5.3 billion by 2035.

The CAGR is expected to be 8% during 2026-2035.

North America will contribute notably, holding a 45% share due to advanced healthcare infrastructure and high chronic wound incidence.

Major players include Organogenesis, MiMedx, Integra LifeSciences, Smith+Nephew, Solventum, and Convatec Group.

The report provides comprehensive analysis including market size, trends, segmentation, regional insights, key players, and forecasts from 2026 to 2035.

Stages include raw material sourcing (e.g., biologics), product development and manufacturing, clinical testing and regulatory approval, distribution through healthcare channels, and end-user application with post-treatment monitoring.

Trends are shifting toward AI-integrated and home-based solutions, with consumers preferring sustainable, personalized therapies that offer faster healing and convenience.

Stringent FDA approvals for biologics, reimbursement policies, and environmental regulations on biohazard waste and sustainable sourcing impact product development and market entry.