5G Core Market Size, Share and Trends 2026 to 2035

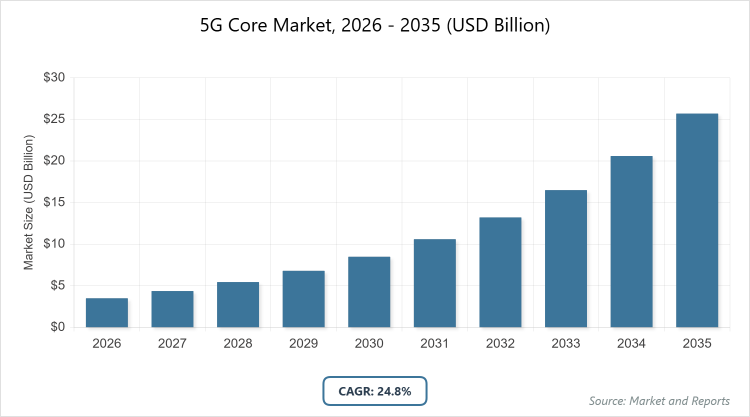

According to MarketnReports, the global 5G Core market size was estimated at USD 3.5 billion in 2025 and is expected to reach USD 35 billion by 2035, growing at a CAGR of 24.8% from 2026 to 2035. 5G Core Market is driven by the increasing demand for high-speed connectivity, low-latency communication, and support for next-generation applications.

What are the Key Insights of 5G Core Market?

- The global 5G Core market size was estimated at USD 3.5 billion in 2025 and is expected to reach USD 35 billion by 2035.

- The market is projected to grow at a CAGR of 24.8% from 2026 to 2035.

- The market is driven by rising adoption of IoT devices, demand for low-latency applications, and expansion of 5G infrastructure worldwide.

- In the Component segment, Solutions dominate with a 65% share due to the critical need for software-defined networking and virtualization technologies that enable efficient core functionality.

- In the Deployment Model segment, Cloud dominates with a 60% share owing to its scalability, cost-effectiveness, and support for dynamic resource allocation in multi-vendor environments.

- In the Network Function segment, AMF dominates with a 25% share because it handles essential mobility and access management, ensuring seamless user connectivity across diverse devices and locations.

- In the End-Use segment, Telecom Operators dominate with an 80% share as they lead the deployment and monetization of 5G services through infrastructure investments.

- Asia Pacific dominates the regional landscape with a 40% share, driven by rapid 5G rollouts in countries like China and India, supported by government initiatives and high mobile penetration.

What is the 5G Core Industry Overview?

The 5G Core market encompasses the central architecture of fifth-generation wireless networks, designed to support enhanced mobile broadband, massive machine-type communications, and ultra-reliable low-latency communications. It represents a shift from traditional monolithic networks to a service-based, cloud-native framework that enables network slicing, virtualization, and seamless integration with edge computing. The market definition includes software, hardware, and services that form the standalone core, distinct from non-standalone setups reliant on 4G infrastructure, facilitating advanced use cases like IoT ecosystems, smart manufacturing, and autonomous systems by providing flexible, scalable, and efficient network management.

What are the Market Dynamics in 5G Core?

Growth Drivers

The primary growth drivers for the 5G Core market include the escalating demand for ultra-high-speed data transfer and minimal latency to support emerging technologies such as autonomous vehicles, remote healthcare, and industrial automation. Telecom operators are increasingly investing in standalone 5G cores to enable network slicing, which allows customized virtual networks for different applications, thereby optimizing resource utilization and opening new revenue streams. Additionally, the proliferation of IoT devices, projected to exceed billions globally, necessitates a robust core network capable of handling massive connectivity without compromising performance. Government policies promoting digital transformation and smart city initiatives further accelerate adoption, as they mandate advanced infrastructure to enhance economic productivity and public services.

Restraints

Restraints in the 5G Core market stem from high initial deployment costs associated with upgrading legacy systems to cloud-native architectures, which can deter smaller operators in developing regions. Interoperability challenges between multi-vendor equipment and existing 4G networks often lead to integration complexities, delaying rollouts and increasing operational expenses. Security concerns, including vulnerabilities in virtualized environments and potential cyber threats to critical infrastructure, pose significant hurdles, requiring substantial investments in robust encryption and threat detection mechanisms. Regulatory variations across countries regarding spectrum allocation and data privacy also create barriers, slowing down global standardization and market expansion.

Opportunities

Opportunities abound in the 5G Core market through the integration of artificial intelligence and machine learning for automated network management, enabling predictive maintenance and optimized traffic routing. The rise of private 5G networks for enterprises offers tailored solutions in sectors like manufacturing and logistics, where dedicated cores ensure reliability and data sovereignty. Expansion into edge computing synergies presents avenues for low-latency applications in remote areas, fostering innovation in areas such as augmented reality and real-time analytics. Collaborations between telecom giants and tech firms can unlock new ecosystems, particularly in underserved markets, by leveraging open-source platforms to reduce costs and accelerate deployment.

Challenges

Challenges in the 5G Core market involve talent shortages in skilled professionals for managing complex, software-centric networks, leading to dependency on external vendors and potential delays. Spectrum scarcity in densely populated urban areas complicates efficient allocation, impacting network performance and coverage. Environmental concerns related to energy consumption of data centers supporting cloud-based cores are gaining traction, pushing for sustainable practices that may increase upfront costs. Geopolitical tensions affecting supply chains for key components, such as semiconductors, add uncertainty, potentially disrupting manufacturing and deployment timelines.

5G Core Market: Report Scope

| Report Attributes | Report Details |

| Report Name | 5G Core Market |

| Market Size 2025 | USD 3.5 Billion |

| Market Forecast 2035 | USD 35 Billion |

| Growth Rate | CAGR of 24.8% |

| Report Pages | 220 |

| Key Companies Covered |

Ericsson, Nokia, Huawei Technologies, Samsung Electronics, ZTE Corporation, and Others |

| Segments Covered | By Component, By Deployment Model, By Network Function, By End-Use, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of 5G Core?

The 5G Core market is segmented by Component, Deployment Model, Network Function, End-Use, and Region.

Based on Component Segment. Solutions emerge as the most dominant subsegment, commanding a significant share due to their role in providing the software foundation for network virtualization and orchestration, which is essential for achieving the flexibility and efficiency promised by 5G. Services rank as the second most dominant, offering consulting, integration, and maintenance support that ensures smooth transitions from legacy systems. The dominance of Solutions stems from the shift toward cloud-native architectures, enabling operators to scale operations dynamically and reduce hardware dependency, thereby driving market growth through cost savings and rapid innovation in service delivery.

Based on Deployment Model Segment. Cloud stands out as the most dominant subsegment, favored for its ability to offer on-demand resources and multi-tenancy, which supports diverse applications without extensive physical infrastructure. On-Premises is the second most dominant, appealing to organizations requiring stringent data control and security. Cloud’s dominance is attributed to its alignment with digital transformation trends, allowing for faster deployment and updates via over-the-air mechanisms, which in turn propels the market by facilitating global scalability and enabling new business models like as-a-service offerings.

Based on Network Function Segment. Access and Mobility Management Function (AMF) is the most dominant subsegment, critical for handling user authentication and mobility across networks, ensuring uninterrupted connectivity. Session Management Function (SMF) follows as the second most dominant, managing data sessions and quality of service. AMF’s leading position arises from its foundational role in user-centric operations, supporting the massive influx of connected devices, which drives the overall market by enhancing reliability and enabling advanced features like seamless handovers in mobile environments.

Based on End-Use Segment. Telecom Operators dominate as the primary subsegment, leveraging 5G cores to expand service portfolios and monetize infrastructure investments. Enterprises are the second most dominant, adopting private networks for customized applications. The prevalence of Telecom Operators is due to their control over spectrum and large-scale deployments, which fuels market expansion by pioneering use cases and setting standards that encourage broader adoption across industries.

What are the Recent Developments in 5G Core Market?

- In 2025, Ericsson announced a major partnership with a leading Asian telecom operator to deploy a cloud-native 5G core, enhancing network slicing capabilities for enterprise clients and supporting over 100 million subscribers with improved latency.

- Nokia unveiled advancements in its 5G core portfolio, including AI-driven automation tools that optimize resource allocation, demonstrated through a successful trial in Europe focusing on energy-efficient operations.

- Huawei launched a new series of 5G core solutions tailored for industrial IoT, incorporating edge computing integration, which was piloted in manufacturing hubs to enable real-time data processing.

What is the Regional Analysis of 5G Core Market?

Asia Pacific to dominate the global market.

Asia Pacific leads the 5G Core market, driven by aggressive infrastructure investments in countries like China, where operators such as China Mobile have achieved widespread standalone 5G coverage, supported by government-backed initiatives for digital economy growth. The region’s high population density and rapid urbanization fuel demand for advanced connectivity, with India emerging as a key player through spectrum auctions and partnerships that accelerate deployments in urban and rural areas alike.

North America holds a strong position, with the United States dominating through innovations from carriers like Verizon and AT&T, focusing on private networks and mmWave spectrum utilization to support enterprise applications in healthcare and autonomous driving.

Europe follows closely, with Germany leading due to its industrial base adopting 5G for smart factories, bolstered by EU regulations promoting cross-border interoperability and sustainability in network operations.

Latin America shows emerging growth, led by Brazil’s spectrum allocations and telecom expansions, addressing connectivity gaps in remote areas to support economic development.

The Middle East and Africa are gaining traction, with the United Arab Emirates at the forefront through visionary projects like smart cities in Dubai, leveraging 5G cores for tourism and logistics enhancements.

What are the Key Market Players in 5G Core?

- Ericsson. Ericsson employs strategies focused on R&D in cloud-native solutions and strategic alliances with telecom operators worldwide, emphasizing open RAN compatibility to drive interoperability and reduce vendor lock-in, while investing in AI for predictive network management.

- Nokia. Nokia’s approach includes comprehensive end-to-end 5G core offerings with a strong emphasis on security and sustainability, pursuing acquisitions and partnerships to expand its portfolio in edge computing and private networks.

- Huawei Technologies. Huawei prioritizes cost-effective, high-performance core solutions with integrated AI capabilities, leveraging its global supply chain and government collaborations in Asia to advance 5G adoption in emerging markets.

- Samsung Electronics. Samsung focuses on innovative hardware-software integration for 5G cores, targeting enterprise segments through customized deployments and collaborations with cloud providers for hybrid models.

- ZTE Corporation. ZTE’s strategies revolve around modular, scalable core architectures, with heavy investments in R&D for network slicing and a push into international markets via competitive pricing and technology transfers.

- Cisco Systems. Cisco leverages its networking expertise to offer virtualized 5G core solutions, emphasizing cybersecurity integrations and partnerships with operators for multi-cloud environments.

- NEC Corporation. NEC adopts a customer-centric strategy, providing tailored 5G core services with a focus on Japan and Asia, incorporating biometrics and AI for enhanced user authentication.

- Oracle Corporation. Oracle’s tactics include cloud-based 5G core platforms with database optimizations, targeting telecoms through SaaS models and integrations with enterprise IT systems.

What are the Market Trends in 5G Core?

- Increasing adoption of cloud-native architectures for greater flexibility and scalability.

- Rise in network slicing to support diverse applications like IoT and ultra-low latency services.

- Integration of AI and machine learning for automated network optimization and fault detection.

- Growing emphasis on security enhancements to counter cyber threats in virtualized environments.

- Expansion of private 5G cores for enterprises in manufacturing and healthcare sectors.

- Shift toward open-source and open RAN standards to promote vendor diversity.

- Focus on energy-efficient solutions amid sustainability concerns.

- Collaborations between telecoms and hyperscalers for hybrid cloud deployments.

What Market Segments and Subsegments are Covered in the 5G Core Report?

By Component

- Solutions

- Services

By Deployment Model

- Cloud

- On-Premises

By Network Function

- Access and Mobility Management Function (AMF)

- Session Management Function (SMF)

- User Plane Function (UPF)

- Policy Control Function (PCF)

- Unified Data Management (UDM)

- Authentication Server Function (AUSF)

- Network Slice Selection Function (NSSF)

- Network Exposure Function (NEF)

- Network Repository Function (NRF)

- Others

By End-Use

- Telecom Operators

- Enterprises

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

5G Core refers to the central architecture of 5G networks, comprising software, hardware, and services that enable advanced features like network slicing, low latency, and massive connectivity, distinct from legacy systems.

Key factors include rising IoT adoption, demand for low-latency applications, government initiatives for digital infrastructure, and advancements in cloud-native technologies.

The market is projected to grow from approximately USD 4.4 billion in 2026 to USD 35 billion by 2035.

The CAGR is expected to be 24.8% during 2026-2035.

Asia Pacific will contribute notably, driven by rapid deployments in China and India.

Major players include Ericsson, Nokia, Huawei Technologies, Samsung Electronics, and ZTE Corporation.

The report provides in-depth analysis of market size, trends, segments, regional insights, key players, and forecasts from 2026 to 2035.

Stages include component manufacturing, software development, system integration, deployment, and ongoing maintenance and support services.

Trends are shifting toward cloud-native and AI-integrated solutions, with preferences for scalable, secure networks supporting enterprise-specific applications.

Regulatory factors include spectrum allocation policies and data privacy laws, while environmental concerns focus on energy consumption and sustainable infrastructure.