4PL Logistics Market Size, Share and Trends 2026 to 2035

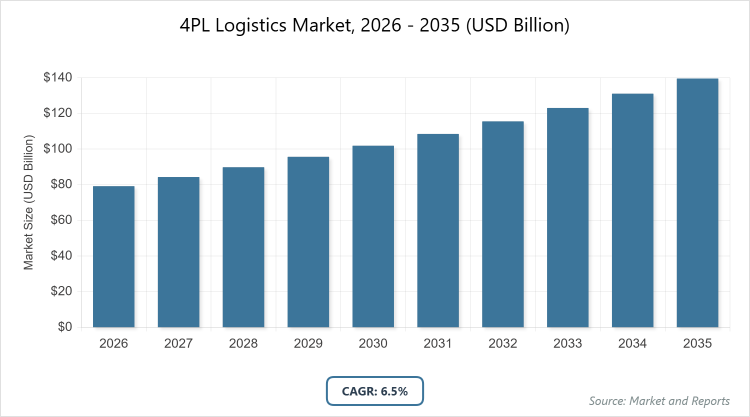

According to MarketnReports, the global 4PL Logistics market size was estimated at USD 79.2 billion in 2025 and is expected to reach USD 148.6 billion by 2035, growing at a CAGR of 6.5% from 2026 to 2035. The 4PL Logistics Market is driven by increasing complexity in supply chains and demand for end-to-end optimization.

What are the Key Insights into 4PL Logistics?

- The global 4PL Logistics market was valued at USD 79.2 billion in 2025 and is projected to reach USD 148.6 billion by 2035.

- The market is expected to grow at a CAGR of 6.5% during the forecast period from 2026 to 2035.

- The market is driven by globalization of trade, e-commerce boom, supply chain digitization, and the need for resilient, sustainable logistics networks.

- In the type segment, the solution integration model dominates with a 40% share due to its ability to consolidate multiple vendors and technologies for streamlined operations.

- In the application segment, supply chain management dominates with a 35% share as it provides end-to-end visibility and optimization critical for complex global chains.

- In the end-user segment, retail & e-commerce dominates with a 25% share owing to high-volume, fast-paced delivery requirements.

- Asia Pacific dominates the regional market with a 35% share, driven by manufacturing hubs in China, rapid e-commerce growth, and infrastructure investments.

What is the Industry Overview of 4PL Logistics?

The 4PL Logistics market involves third-party providers that oversee and integrate the entire supply chain, acting as a single point of contact to manage multiple 3PLs, technology, and processes for optimized efficiency, cost reduction, and strategic alignment. Market definition includes comprehensive logistics solutions that encompass planning, execution, and oversight of transportation, warehousing, inventory, and distribution, leveraging advanced analytics, AI, and digital platforms to provide value-added services beyond traditional logistics, while addressing challenges in global trade volatility, sustainability, and technological integration for seamless end-to-end visibility.

What are the Market Dynamics of 4PL Logistics?

Growth Drivers

The 4PL Logistics market is propelled by the increasing complexity of global supply chains, where 4PL providers offer integrated solutions that coordinate multiple 3PLs, technology platforms, and data analytics to optimize costs, reduce lead times, and enhance visibility. The e-commerce surge, particularly in emerging markets, demands agile logistics for last-mile delivery and reverse flows, driving adoption of 4PL for scalable, tech-driven networks. Advancements in AI, IoT, and blockchain enable real-time tracking and predictive analytics, improving resilience against disruptions like pandemics or trade wars. Sustainability initiatives, including green transportation and carbon tracking, further boost demand as companies seek 4PL partners for eco-friendly strategies.

Restraints

High implementation costs for advanced 4PL systems, including technology integration and consulting fees, limit adoption among small and medium enterprises in cost-sensitive regions. Dependency on data sharing raises privacy and security concerns, with regulations like GDPR adding compliance burdens. Limited skilled talent in supply chain analytics and digital transformation hinders effective utilization. Volatility in global trade, such as tariffs and geopolitical tensions, disrupts 4PL networks, while resistance from traditional 3PL providers slows market transition.

Opportunities

Opportunities lie in leveraging AI and machine learning for predictive logistics, enabling proactive risk management and dynamic routing in volatile markets. Expansion into emerging economies with growing e-commerce and manufacturing offers untapped potential for customized 4PL solutions. Partnerships with tech firms for blockchain-based transparency can differentiate services, while sustainability-focused 4PL models attract eco-conscious clients. The rise of omnichannel retail creates demand for integrated inventory management across physical and digital channels.

Challenges

Challenges include integrating legacy systems with modern 4PL platforms, requiring significant IT overhauls and change management. Rapid technological evolution demands continuous investment to avoid obsolescence, straining resources. Supply chain disruptions from climate events or pandemics test 4PL resilience, while varying international regulations complicate global operations. Ensuring data accuracy across multiple partners remains critical to avoid errors in analytics-driven decisions.

4PL Logistics Market: Report Scope

| Report Attributes | Report Details |

| Report Name | 4PL Logistics Market |

| Market Size 2025 | USD 79.2 Billion |

| Market Forecast 2035 | USD 148.6 Billion |

| Growth Rate | CAGR of 6.5% |

| Report Pages | 210 |

| Key Companies Covered | DHL Supply Chain, Kuehne + Nagel, DB Schenker, UPS Supply Chain Solutions, Accenture, CEVA Logistics, XPO Logistics, 4PL Insights, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of 4PL Logistics?

The 4PL Logistics market is segmented by type, application, end-user, and region.

By Type. Solution integration model is the most dominant subsegment, holding approximately 40% market share, due to its comprehensive coordination of vendors and tech for seamless operations. This dominance drives the market by reducing complexity and costs in multi-tier supply chains. Lead logistics provider model ranks as the second most dominant, with around 30% share, focusing on strategic oversight, propelling growth through enhanced decision-making and efficiency.

By Application. Supply chain management emerges as the most dominant subsegment, capturing about 35% share, primarily because it offers end-to-end visibility and optimization. This leads to market growth by enabling resilient, data-driven networks. Transportation management follows as the second most dominant, with roughly 25% share, streamlining freight operations, driving the market via cost savings and speed improvements.

By End-User. Retail & e-commerce represents the most dominant subsegment at about 25% share, driven by high-volume, fast-delivery needs. This dominance accelerates market expansion through agile, customer-centric logistics. Automotive ranks second most dominant, holding around 20% share, requiring precise just-in-time supply, contributing to growth via inventory optimization.

What are the Recent Developments in 4PL Logistics?

- In January 2025, DHL Supply Chain expanded its 4PL services in Asia with AI-driven predictive analytics for e-commerce clients.

- In December 2024, Kuehne + Nagel launched a blockchain-based platform for transparent 4PL supply chain tracking.

- In November 2024, DB Schenker partnered with a tech startup for IoT-integrated 4PL solutions in automotive logistics.

- In October 2024, UPS Supply Chain Solutions acquired a 4PL software firm to enhance its digital offerings.

- In September 2024, Accenture released a report on sustainable 4PL models, influencing industry practices.

What is the Regional Analysis of 4PL Logistics?

- Asia Pacific to dominate the global market.

Asia Pacific holds the largest share at approximately 35%, with China as the dominating country, due to rapid industrialization, massive manufacturing bases, and government initiatives promoting infrastructure development. This region’s growth is fueled by low-cost labor, abundant raw materials, and increasing investments in oil & gas and mining, positioning it as a key hub for coating production and consumption. High urbanization rates drive demand in the construction and transportation sectors. India’s Make in India campaign boosts local manufacturing of coatings. Southeast Asian nations like Vietnam expand through foreign direct investments. Environmental policies push for low-VOC innovations. Strong export networks enhance global supply chains.

North America follows closely, driven by advanced technological adoption and stringent safety standards, where the United States dominates through its robust energy sector and R&D investments. Growth stems from shale gas exploration and renewable energy projects requiring durable coatings, though higher costs moderate expansion. Canadian oil sands operations demand specialized solutions for harsh climates. Government subsidies for green energy promote sustainable coatings. The region’s focus on aerospace and automotive industries requires high-performance materials. Collaborations between universities and companies foster innovation in nanotechnology.

Europe exhibits strong performance with emphasis on sustainability and regulation, led by Germany through its engineering excellence and firms like BASF. The region’s expansion benefits from EU environmental policies favoring low-VOC coatings and a focus on the marine and power industries. Horizon Europe funds research in eco-friendly formulations. The UK’s offshore wind farms increase demand for marine protection. Multilingual compliance aids exports to diverse markets like France and Italy. Circular economy initiatives recycle coating waste, reducing environmental impact.

Latin America shows steady but moderate advancement, dominated by Brazil’s oil & gas and mining sectors, supported by foreign investments, though limited by economic fluctuations. Mexico benefits from NAFTA ties, enhancing trade with North America for supply chains. Government infrastructure plans in Argentina promote road and bridge protection. The rise of renewable projects in Chile creates niches for wind turbine coatings. However, political instability affects consistent investments. Emerging mining in Peru demands wear-resistant solutions for equipment.

The Middle East and Africa remain emerging, with the United Arab Emirates and Saudi Arabia leading through oil-funded infrastructure, constrained by lower diversification but showing potential via energy projects. Vision 2030 in Saudi Arabia invests in downstream chemical processing. South Africa’s mining industry adopts conveyor and pump protections. Technology transfers from European partners build local expertise in Egypt. However, water scarcity influences waterborne coating preferences. Investments in solar farms create demand for dust-resistant surfaces in arid areas.

What are the Key Market Players in 4PL Logistics?

- DHL Supply Chain. DHL focuses on digital 4PL platforms with AI analytics, expanding through partnerships in e-commerce and sustainability.

- Kuehne + Nagel. Kuehne + Nagel emphasizes blockchain for transparency, investing in global networks for automotive and pharma logistics.

- DB Schenker. DB Schenker pursues IoT-integrated solutions, strategizing on green logistics for energy and manufacturing sectors.

- UPS Supply Chain Solutions. UPS leverages acquisitions for tech enhancements, targeting retail and healthcare for agile supply chains.

- Accenture. Accenture offers consulting-led 4PL, focusing on digital transformation and risk management for diverse industries.

- CEVA Logistics. CEVA specializes in end-to-end optimization, expanding through mergers for transportation and warehouse management.

- XPO Logistics. XPO invests in predictive analytics, targeting e-commerce for fast, resilient delivery networks.

- 4PL Insights. 4PL Insights focuses on customized models, strategizing on data-driven insights for SMEs.

What are the Market Trends in 4PL Logistics?

- Increasing adoption of AI and ML for predictive analytics.

- Rise of blockchain for transparent supply chains.

- Focus on sustainable and green logistics practices.

- Expansion of digital twins for virtual simulation.

- Growth in e-commerce-driven 4PL solutions.

- Integration of IoT for real-time tracking.

What Market Segments and Subsegments are Covered in the 4PL Logistics Report?

By Type

- Solution Integration Model

- Comprehensive Transportation Model

- Lead Logistics Provider Model

- Industry Innovator Model

- Synergy Plus Operating Model

- End-to-End Supply Chain Management

- Vendor Managed Inventory

- Network Optimization

- Risk Management

- Digital Transformation

- Others

By Application

- Supply Chain Management

- Transportation Management

- Inventory Management

- Order Management

- Demand Forecasting

- Warehouse Management

- Procurement Management

- Reverse Logistics

- Customs Clearance

- Analytics & Reporting

- Others

By End-User

- Automotive

- Consumer Goods

- Healthcare & Pharmaceuticals

- Retail & E-Commerce

- Industrial & Manufacturing

- Food & Beverages

- Aerospace & Defense

- Oil & Gas

- Chemicals

- Electronics & Technology

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

4PL Logistics involves outsourcing entire supply chain management to a lead provider that integrates multiple 3PLs and technologies for optimization.

Key factors include supply chain complexity, e-commerce growth, digitization, and sustainability demands.

The market is projected to grow from USD 79.2 billion in 2025 to USD 148.6 billion by 2035.

The CAGR is expected to be 6.5%.

Asia Pacific will contribute notably, holding around 35% share due to industrialization and manufacturing growth.

Major players include DHL Supply Chain, Kuehne + Nagel, DB Schenker, UPS Supply Chain Solutions, and Accenture.

The report provides detailed analysis of size, trends, segments, regional outlook, key players, and forecasts.

Stages include strategic planning, vendor selection, technology integration, execution, monitoring, and optimization.

Trends evolve toward AI and blockchain, with preferences for sustainable, transparent supply chains.

Trade regulations and environmental standards for emissions drive adoption of green practices and compliance.