3D Scanner Market Size, Share and Trends 2026 to 2035

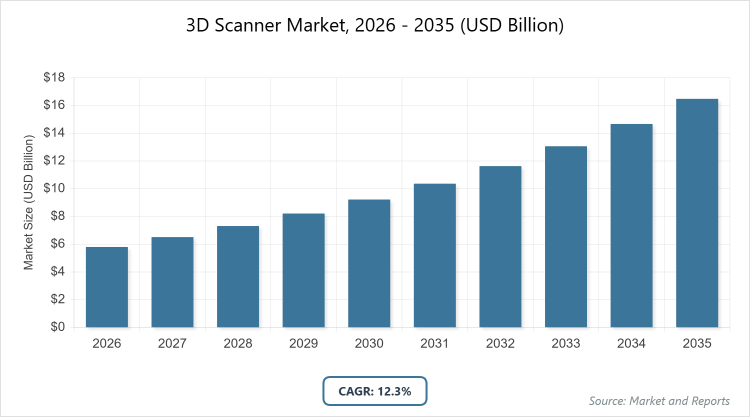

According to MarketnReports, the global 3D Scanner market size was estimated at USD 5.8 billion in 2025 and is expected to reach USD 18.4 billion by 2035, growing at a CAGR of 12.3% from 2026 to 2035. The 3D Scanner Market is driven by increasing adoption of digital twin technologies, rising demand for quality inspection in manufacturing, and rapid growth in reverse engineering applications.

What are the Key Insights into the 3D Scanner?

- The global 3D Scanner market was valued at USD 5.8 billion in 2025 and is projected to reach USD 18.4 billion by 2035.

- The market is expected to grow at a CAGR of 12.3% during the forecast period from 2026 to 2035.

- The market is driven by rising adoption in Industry 4.0, growth in additive manufacturing, demand for metrology-grade accuracy, and expansion in healthcare and cultural heritage sectors.

- In the type segment, laser scanners dominate with a 38% share due to their high precision and long-range capabilities, essential for large-object scanning in aerospace and construction.

- In the application segment, quality control & inspection dominate with a 42% share as it ensures dimensional accuracy in manufacturing, reducing defects and rework costs.

- In the end-user segment, automotive & aerospace dominate with a 32% share, owing to strict tolerances and the need for reverse engineering of legacy parts.

- North America dominates the regional market with a 38% share, driven by a strong R&D ecosystem, advanced manufacturing, and the presence of key players like Faro and Hexagon.

What is the Industry Overview of 3D Scanner?

The 3D Scanner market comprises non-contact and contact-based devices that capture the shape and appearance of physical objects to create precise digital 3D models, enabling applications in quality control, reverse engineering, cultural preservation, and medical planning. Market definition includes laser triangulation, structured light, photogrammetry, and LiDAR-based systems that generate point clouds or mesh data with high accuracy, supporting industries requiring exact replication, dimensional verification, or virtual reconstruction while addressing challenges in scan speed, resolution, portability, and integration with CAD/CAM software.

What are the Market Dynamics of 3D Scanner?

Growth Drivers

The 3D Scanner market is propelled by the rapid adoption of digital twins and Industry 4.0, where precise 3D models enable predictive maintenance, virtual simulation, and quality assurance in manufacturing. Increasing integration with additive manufacturing accelerates reverse engineering and customized production, particularly in aerospace for lightweight components. Growing applications in healthcare for patient-specific implants and orthotics, combined with cultural heritage digitization projects, drive demand for high-resolution systems. Advancements in portable and handheld scanners improve field usability, while falling hardware costs and improved software make technology accessible to SMEs.

Restraints

High capital costs for metrology-grade and long-range scanners limit adoption in price-sensitive sectors and developing regions. Technical limitations such as surface reflectivity issues, scan time for large objects, and post-processing complexity reduce efficiency. Stringent data privacy regulations (GDPR, HIPAA) complicate usage in medical and cultural applications. Competition from photogrammetry apps on smartphones offers low-cost alternatives for basic needs, eroding entry-level market share. Supply chain disruptions for optical and laser components increase prices and lead times.

Opportunities

Opportunities arise from the integration of AI for automated point cloud processing and feature recognition, reducing manual effort and errors. Expansion into emerging applications like underwater scanning and drone-mounted LiDAR opens new verticals. Partnerships between scanner manufacturers and software firms can deliver end-to-end solutions for digital twin creation. Growing demand in construction for BIM integration and in education for affordable learning tools presents untapped potential. Development of hybrid scanning systems combining multiple technologies offers superior accuracy across diverse surfaces.

Challenges

Challenges include achieving sub-millimeter accuracy consistently across materials and environments, requiring continuous calibration and environmental control. Rapid technological obsolescence demands frequent hardware and software upgrades, straining budgets. Cybersecurity risks in connected scanners threaten proprietary design data. Varying international metrology standards complicate global certification and interoperability. Shortage of skilled operators and post-processing experts slows adoption in many regions.

3D Scanner Market: Report Scope

| Report Attributes | Report Details |

| Report Name | 3D Scanner Market |

| Market Size 2025 | USD 5.8 Billion |

| Market Forecast 2035 | USD 18.4 Billion |

| Growth Rate | CAGR of 12.3% |

| Report Pages | 225 |

| Key Companies Covered | Faro Technologies, Hexagon AB, Artec 3D, Creaform (AMETEK), ZEISS Group, Trimble Inc., Topcon Corporation, GOM (Zeiss), Shining 3D, Scantech, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of 3D Scanner?

The 3D Scanner market is segmented by type, application, end-user, and region.

By Type. Laser scanners are the most dominant subsegment, holding approximately 38% market share, due to their long-range capability and high accuracy in industrial and outdoor applications. This dominance drives the market by enabling efficient scanning of large structures in aerospace and construction, reducing project timelines. Structured light scanners rank as the second most dominant, with around 28% share, offering superior detail for small to medium objects, propelling growth through applications in medical and cultural heritage digitization.

By Application. Quality control & inspection emerges as the most dominant subsegment, capturing about 42% share, primarily because it ensures compliance with tight tolerances in manufacturing. This leads to market growth by minimizing defects and supporting zero-defect initiatives in automotive and aerospace. Reverse engineering follows as the second most dominant, with roughly 25% share, enabling legacy part reproduction and design updates, driving the market via cost savings and innovation.

By End-User. Automotive & aerospace represents the most dominant subsegment at about 32% share, driven by requirements for lightweight components and precise quality checks. This dominance accelerates market expansion through high-value contracts and adoption of digital twins. Manufacturing ranks second most dominant, holding around 22% share, due to widespread use in general production, contributing to growth via automation and efficiency gains.

What are the Recent Developments in 3D Scanner?

- In March 2025, Faro Technologies launched the Focus Premium Max LiDAR scanner with extended range and improved noise reduction for large-scale industrial applications.

- In January 2025, Hexagon AB introduced the Absolute Scanner AS1 with enhanced blue-light technology for faster data capture in metrology.

- In November 2024, Artec 3D released the Leo wireless scanner with onboard processing and improved tracking for field use.

- In August 2024, Creaform launched the HandySCAN BLACK|Elite Limited Edition with 30% higher resolution for aerospace inspection.

- In June 2024, ZEISS introduced the T-SCAN Hawk 2 handheld scanner with integrated photogrammetry for improved accuracy in automotive applications.

What is the Regional Analysis of the 3D Scanner?

- North America is expected to dominate the global market.

North America holds the largest share at approximately 38%, with the United States as the dominating country, attributed to its advanced manufacturing ecosystem, high R&D investment, and presence of leading companies like Faro and Hexagon. This region’s leadership is supported by strong demand in aerospace and automotive for precision metrology, favorable government funding for innovation, and widespread adoption of digital twin technologies, positioning it as a hub for high-end scanner development and deployment. The concentration of aerospace giants in Washington and California drives demand for large-volume scanning. NASA’s use of scanners for spacecraft inspection sets benchmarks for accuracy. Defense contracts fund portable systems for field use.

Europe follows with steady growth, driven by precision engineering and regulatory compliance, where Germany dominates through its industrial strength and firms like Zeiss and GOM. The region’s expansion benefits from EU funding for digital manufacturing and a strong focus on quality control in the automotive and machinery sectors, supported by collaborative research networks. Horizon Europe programs finance multi-sensor scanner projects. The UK’s advanced manufacturing hubs in the Midlands promote adoption in aerospace. Multilingual software interfaces support diverse markets in France and Italy. REACH and CE marking regulations ensure safe and compliant devices. Industry consortia share calibration best practices.

Asia Pacific is the fastest-growing region, exhibiting a high CAGR, with China leading due to massive industrial output and government-backed smart manufacturing initiatives. This area’s potential is amplified by rapid adoption in electronics and automotive, cost-effective production, and increasing investments in quality assurance technologies across India, Japan, and South Korea. Massive electronics manufacturing clusters in Shenzhen drive demand for inline inspection. India’s Make in India campaign subsidizes scanner adoption in SMEs. Japan’s precision engineering tradition favors high-resolution systems.

Latin America demonstrates moderate progress, dominated by Brazil’s aerospace and automotive sectors, supported by foreign investments though limited by economic variability; growth is aided by adoption in manufacturing and construction. Mexico benefits from NAFTA ties, facilitating tech transfers from North America. Government digital initiatives in Argentina promote education in scanning technologies. The rise of EVs in Chile creates demand for component inspection. However, currency fluctuations impact import costs for high-end devices. Emerging aerospace in Colombia adopts a prototype development.

The Middle East and Africa remain emerging, with the United Arab Emirates leading through smart city and infrastructure projects, constrained by lower tech penetration but promising via diversification into advanced manufacturing and oil & gas inspection. Saudi Arabia’s Vision 2030 funds R&D centers for localized scanner use. South Africa’s mining sector adopts for equipment reverse engineering. Technology partnerships with European firms build expertise in Egypt. However, water scarcity impacts cooling in high-end laser systems. Investments in solar farms create demand for panel inspection.

What are the Key Market Players in 3D Scanner?

- Faro Technologies. Faro focuses on portable and large-volume laser scanners, investing in software integration for industrial metrology and construction applications.

- Hexagon AB. Hexagon emphasizes high-accuracy metrology solutions, pursuing acquisitions to expand in automotive and aerospace quality control.

- Artec 3D. Artec specializes in handheld structured light scanners, targeting cultural heritage and reverse engineering with wireless innovations.

- Creaform (AMETEK). Creaform develops portable metrology-grade scanners, focusing on user-friendly designs for field inspection in manufacturing.

- ZEISS Group. ZEISS invests in optical and blue-light technology for precision scanning in medical and industrial sectors.

- Trimble Inc. Trimble targets construction and geospatial applications with LiDAR and photogrammetry integration.

- Topcon Corporation. Topcon focuses on surveying and infrastructure scanning with rugged, long-range systems.

- GOM (Zeiss). GOM specializes in structured light for high-resolution industrial inspection, leveraging optical expertise.

What are the Market Trends in 3D Scanner?

- Increasing adoption of handheld and wireless scanners for field applications.

- Integration of AI for automated feature recognition and post-processing.

- Rise of long-range LiDAR for large-scale construction and heritage.

- Growth in metrology-grade portable systems for in-line inspection.

- Expansion of photogrammetry combined with laser scanning.

- Focus on blue-light technology for improved accuracy on shiny surfaces.

- Development of software ecosystems for seamless CAD integration.

What Market Segments and Subsegments are Covered in the 3D Scanner Report?

By Type

- Laser Scanners

- Structured Light Scanners

- Photogrammetry Scanners

- LiDAR Scanners

- Time-of-Flight Scanners

- Contact Scanners

- Handheld Scanners

- Stationary Scanners

- Portable Scanners

- Metrology-Grade Scanners

- Others

By Application

- Quality Control & Inspection

- Reverse Engineering

- Rapid Prototyping

- Cultural Heritage & Archaeology

- Medical & Dental

- Architecture & Construction

- Automotive & Aerospace

- Entertainment & Media

- Education & Research

- Forensic Analysis

- Others

By End-User

- Automotive & Aerospace

- Healthcare & Medical

- Architecture, Engineering & Construction (AEC)

- Consumer Goods & Electronics

- Manufacturing

- Education & Research Institutions

- Cultural Institutions & Museums

- Government & Defense

- Media & Entertainment

- Oil & Gas

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

3D Scanners are devices that capture the shape and appearance of physical objects to create accurate digital 3D models using laser, light, or photogrammetry.

Key factors include Industry 4.0 adoption, quality inspection needs, reverse engineering demand, and advancements in portable technology.

The market is projected to grow from USD 5.8 billion in 2025 to USD 18.4 billion by 2035.

The CAGR is expected to be 12.3%.

North America will contribute notably, holding around 38% share due to advanced manufacturing and R&D.

Major players include Faro Technologies, Hexagon AB, Artec 3D, Creaform, and ZEISS Group.

The report delivers detailed analysis of size, trends, segments, regional insights, competitive landscape, and forecasts.

Stages encompass component manufacturing, scanner assembly, software development, distribution, training, and after-sales support.

Trends shift toward portable, AI-integrated, and multi-sensor systems, with preferences for high accuracy and ease of use.

Data privacy regulations and environmental standards for energy-efficient devices influence design and market access.