3D Printed Wearable Market Size, Share and Trends 2026 to 2035

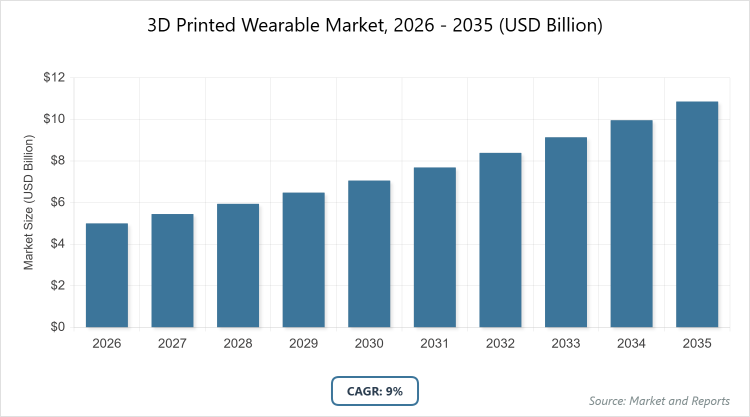

According to MarketnReports, the global 3D Printed Wearable market size was estimated at USD 5 billion in 2025 and is expected to reach USD 12 billion by 2035, growing at a CAGR of 9% from 2026 to 2035. The 3D Printed Wearable Market is driven by rising demand for personalized healthcare devices and advancements in additive manufacturing technologies.

What are the Key Insights into 3D Printed Wearable?

- The global 3D Printed Wearable market was valued at USD 5 billion in 2025 and is projected to reach USD 12 billion by 2035.

- The market is expected to grow at a CAGR of 9% during the forecast period from 2026 to 2035.

- The market is driven by increasing adoption of personalized medical devices, technological advancements in 3D printing materials, and growing demand in the fitness and fashion sectors.

- In the type segment, prosthetics dominate with a 35% share due to their customization for patient-specific needs, improving comfort and functionality in healthcare.

- In the application segment, medical & healthcare dominates with a 50% share as it enables precise implants and aids, reducing surgery times and costs.

- In the end-user segment, hospitals dominate with a 30% share owing to high demand for custom orthopedic and surgical tools.

- North America dominates the regional market with a 35% share, driven by advanced R&D infrastructure, strong healthcare spending, and the presence of key innovators like 3D Systems.

What is the Industry Overview of 3D Printed Wearable?

The 3D Printed Wearable market involves additive manufacturing techniques to create customized, lightweight devices worn on the body, integrating electronics, sensors, and biocompatible materials for enhanced functionality in health monitoring, fitness tracking, and medical prosthetics. Market definition includes products fabricated layer-by-layer using 3D printers, offering personalization, rapid prototyping, and material efficiency, catering to sectors requiring precise fit, durability, and integration with IoT for real-time data collection, while addressing challenges in scalability and regulatory compliance for wearable tech.

What are the Market Dynamics of 3D Printed Wearable?

Growth Drivers

The 3D Printed Wearable market is propelled by the surging need for personalized healthcare solutions, where 3D printing allows for bespoke prosthetics and implants tailored to individual anatomy, enhancing patient outcomes and reducing recovery times. Advancements in biocompatible materials and multi-material printing enable integration of sensors for smart wearables, driving adoption in fitness and remote monitoring. Rising chronic diseases and aging populations increase demand for custom orthotics and hearing aids, while cost efficiencies in production attract manufacturers. Government initiatives promoting additive manufacturing and sustainability further accelerate innovation and market penetration.

Restraints

High initial investment in 3D printing equipment and materials poses a barrier for small-scale manufacturers and startups, limiting widespread adoption in emerging markets. Regulatory hurdles for medical-grade wearables, requiring stringent certifications like FDA approval, delay product launches and increase compliance costs. Limited material options for durable, flexible wearables restrict applications in high-stress environments, while intellectual property concerns over designs hinder collaboration. Supply chain vulnerabilities for specialized filaments and powders, exacerbated by global disruptions, impact production consistency.

Opportunities

Opportunities emerge from integrating AI and IoT into 3D printed wearables for real-time health tracking, appealing to telehealth and wellness sectors. Expansion into fashion with customizable, sustainable accessories offers growth in consumer markets, while bioprinting advancements promise revolutionary medical applications like skin grafts. Emerging economies with rising healthcare access present untapped potential for affordable prosthetics. Partnerships between tech firms and material scientists can develop new composites, and e-commerce platforms for on-demand printing enable mass customization.

Challenges

Challenges include ensuring biocompatibility and long-term durability of printed materials under body stress, requiring ongoing R&D to prevent failures. Scalability issues in mass production versus customization limit market reach, while skill gaps in 3D design and printing workforce slow innovation. Cybersecurity risks in connected wearables pose data privacy threats, and environmental concerns over plastic waste from printing necessitate sustainable practices. Varying global standards complicate international expansion.

3D Printed Wearable Market: Report Scope

| Report Attributes | Report Details |

| Report Name | 3D Printed Wearable Market |

| Market Size 2025 | USD 5 Billion |

| Market Forecast 2035 | USD 12 Billion |

| Growth Rate | CAGR of 9% |

| Report Pages | 190 |

| Key Companies Covered | 3D Systems Corporation, Stratasys Ltd., Materialise NV, HP Inc., EOS GmbH, Carbon, Inc., Formlabs Inc., GE Additive, Renishaw plc, Desktop Metal, Inc., and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of 3D Printed Wearable?

The 3D Printed Wearable market is segmented by type, application, end-user, and region.

By Type. Prosthetics are the most dominant subsegment, holding approximately 35% market share, due to their ability to provide patient-specific fits that improve mobility and reduce rejection rates. This dominance drives the market by addressing unmet needs in amputee care, lowering costs through rapid prototyping. Orthopedic implants rank as the second most dominant, with around 25% share, offering customized solutions for joint replacements, propelling growth via enhanced surgical precision and patient recovery.

By Application. Medical & healthcare emerges as the most dominant subsegment, capturing about 50% share, primarily because it facilitates tailored devices for therapy and diagnostics. This leads to market growth by minimizing invasive procedures and improving treatment efficacy. Sports & fitness follows as the second most dominant, with roughly 20% share, enabling performance-tracking gear, driving the market through consumer demand for personalized athletic aids.

By End-User. Hospitals represent the most dominant subsegment at about 30% share, driven by needs for on-site custom fabrication. This dominance accelerates market expansion through efficient patient care integration. Pharma & biotech companies rank second most dominant, holding around 20% share, using wearables for drug delivery trials, contributing to growth via R&D advancements.

What are the Recent Developments in 3D Printed Wearable?

- In January 2025, Ortho Solutions acquired Meshworks to enhance 3D printed orthopedic wearables with advanced mesh technology.

- In June 2024, Ricoh USA launched RICOH 3D for Healthcare Innovation Studio for point-of-care 3D printed medical wearables.

- In January 2024, Texas A&M University developed 3D-printed electronic skin mimicking human sensory functions.

- In October 2023, Fingy3D advanced prosthetic fingers with 3D printing for improved dexterity.

- In June 2020, GE Additive collaborated with Rejoint for 3D printed knee implants (noted for ongoing impact).

What is the Regional Analysis of 3D Printed Wearable?

- North America is expected to dominate the global market.

North America holds the largest share at approximately 35%, with the United States as the dominating country, owing to its robust R&D ecosystem, high healthcare investment, and presence of leaders like 3D Systems. This region’s growth is fueled by FDA support for innovative devices, strong startup culture in wearables, and demand for custom prosthetics amid rising chronic conditions. Collaborations between universities and industry giants accelerate material advancements for biocompatible printing. The region’s focus on veteran care through VA programs boosts prosthetic applications.

Europe follows with steady growth, driven by advanced manufacturing and a sustainability focus, where Germany dominates through engineering expertise and companies like EOS. The region’s expansion benefits from EU grants for health tech and the aging population’s needs for orthopedic wearables. Horizon Europe funds research in bioprinting for personalized medicine. The UK’s NHS pilots 3D printed aids for cost savings. Multilingual design software supports diverse markets like France and Italy. Emphasis on the circular economy promotes recyclable materials in wearables.

Asia Pacific is the fastest-growing region, exhibiting a high CAGR, with China leading due to massive production capabilities and government initiatives for smart manufacturing. This area’s potential is enhanced by low-cost printing and rising fitness trends in India and Japan. Massive investments in 5G enable sensor-integrated wearables for health monitoring. India’s medtech startups innovate affordable prosthetics for rural access. Southeast Asian nations like Singapore adopt sports tech. Cultural emphasis on wellness boosts consumer demand for customized fitness gear.

Latin America demonstrates moderate progress, dominated by Brazil’s healthcare reforms and growing biotech sector, supported by foreign investments, though challenged by infrastructure. Mexico benefits from nearshoring, integrating with U.S. supply chains for joint R&D. Government programs in Argentina promote 3D printing in education. The rise of telemedicine in Colombia creates needs for remote-fitted wearables. However, economic variability affects consistent funding. Emerging eco-tourism demands sustainable, lightweight outdoor gear.

The Middle East and Africa remain emerging, with the United Arab Emirates leading through tech diversification and smart city projects, limited by access but promising via medical tourism. Saudi Arabia’s Vision 2030 funds additive manufacturing hubs for healthcare. South Africa’s universities pioneer low-cost prosthetics for underserved communities. Technology transfers from European firms build local expertise. However, water scarcity influences material choices for durable wearables. Investments in solar-powered printers address energy concerns in remote areas.

What are the Key Market Players in 3D Printed Wearable?

- 3D Systems Corporation. 3D Systems focuses on medical-grade printing with biocompatible materials, leveraging acquisitions for expanded prosthetic solutions.

- Stratasys Ltd. emphasizes multi-material wearables, investing in R&D for flexible electronics integration in fitness trackers.

- Materialise NV. Materialise specializes in software for custom designs, partnering with hospitals for orthopedic implants.

- HP Inc. pursues affordable consumer wearables, using Multi Jet Fusion for high-volume production.

- EOS GmbH. EOS targets industrial applications, developing metal-printed sensors for aerospace wearables.

- Carbon, Inc. Carbon innovates with resin-based printing for soft, durable fitness devices.

- Formlabs Inc. offers desktop solutions for prototyping, focusing on accessible medical aids.

- GE Additive. GE Additive advances bioprinting for hearing aids, collaborating with healthcare firms.

What are the Market Trends in 3D Printed Wearable?

- Increasing integration of AI for design optimization and personalization.

- Rise of bioprinting for skin-like sensors in medical wearables.

- Adoption of sustainable, recyclable materials to reduce environmental impact.

- Growth in smart wearables with embedded IoT for health monitoring.

- Expansion of on-demand printing via e-commerce platforms.

- Focus on hybrid printing combining metals and polymers.

What Market Segments and Subsegments are Covered in the 3D Printed Wearable Report?

By Type

- Prosthetics

- Orthopedic Implants

- Surgical Instruments

- Fitness Trackers

- Smart Watches

- Hearing Aids

- Eyewear Frames

- Dental Appliances

- Customized Footwear

- Wearable Sensors

- Others

By Application

- Medical & Healthcare

- Consumer Electronics

- Sports & Fitness

- Fashion & Jewelry

- Aerospace & Defense

- Automotive

- Education & Research

- Military

- Personal Use

- Industrial

- Others

By End-User

- Hospitals

- Pharma & Biotech Companies

- Academic Institutes

- Consumer Goods Manufacturers

- Sports Organizations

- Fashion Brands

- Aerospace Companies

- Automotive Firms

- Military & Defense

- Individuals

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

3D Printed Wearables are customized devices created using additive manufacturing, integrating sensors and materials for health, fitness, and fashion applications.

Key factors include technological advancements, demand for personalization, healthcare needs, and sustainable manufacturing.

The market is projected to grow from USD 5 billion in 2025 to USD 12 billion by 2035.

The CAGR is expected to be 9%.

North America will contribute notably, holding around 35% share due to innovation and healthcare investment.

Major players include 3D Systems, Stratasys, Materialise, HP Inc., and EOS GmbH.

The report provides analysis of size, trends, segments, regions, players, and forecasts.

Stages include material sourcing, design, printing, assembly, testing, and distribution.

Trends evolve toward smart integration and sustainability, with preferences for customized, eco-friendly devices.

Medical regulations like FDA approvals and environmental pushes for biodegradable materials influence compliance and innovation.