3D Printed Medical Devices Market Size, Share and Trends 2026 to 2035

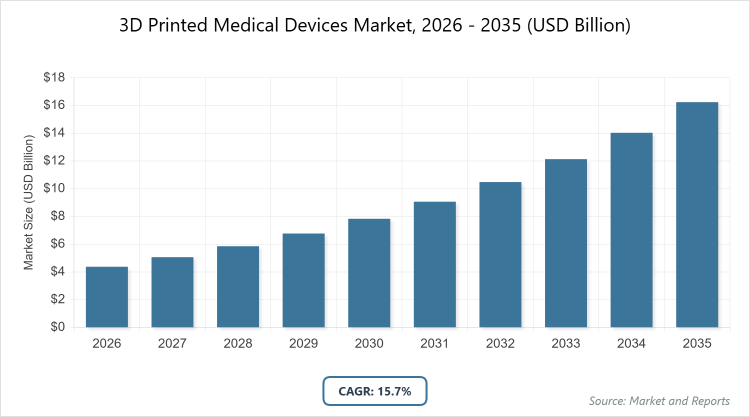

According to MarketnReports, the global 3D Printed Medical Devices market size was estimated at USD 4.37 billion in 2025 and is expected to reach USD 18.84 billion by 2035, growing at a CAGR of 15.7% from 2026 to 2035. 3D Printed Medical Devices Market is driven by the increasing demand for personalized and customized medical solutions.

What are the Key Insights for 3D Printed Medical Devices Market?

- The global 3D Printed Medical Devices market was valued at USD 4.37 billion in 2025 and is projected to reach USD 18.84 billion by 2035.

- The market is expected to grow at a CAGR of 15.7% during the forecast period from 2026 to 2035.

- The market is driven by advancements in additive manufacturing technologies and the growing need for customized healthcare solutions.

- In the technology segment, Laser Beam Melting dominated with 34% share due to its high precision in producing durable metal-based devices for implants.

- In the application segment, Prosthetics and Implants held the largest share of 40% owing to the capability to create patient-specific solutions that improve fit and functionality.

- In the end-user segment, Hospitals and Clinics accounted for 45% share because of on-site printing capabilities that enable rapid prototyping and surgical planning.

- North America dominated the market with 40% share, attributed to advanced healthcare infrastructure, high R&D investments, and favorable regulatory environments.

What is the Industry Overview of 3D Printed Medical Devices?

The 3D printed medical devices market encompasses the use of additive manufacturing technologies to produce customized medical equipment, implants, and tools tailored to individual patient needs. This market involves layering materials such as plastics, metals, and biomaterials to create precise, patient-specific devices that enhance treatment outcomes and reduce production times compared to traditional methods. Market definition includes hardware like printers, software for design, services for customization, and materials used in fabrication, all aimed at applications in orthopedics, dentistry, and surgery, driven by innovation in bioprinting and regulatory approvals for clinical use.

What are the Market Dynamics in 3D Printed Medical Devices?

Growth Drivers

Technological advancements in 3D printing, such as improved material biocompatibility and faster printing speeds, are propelling market expansion by enabling the production of complex, customized devices that traditional manufacturing cannot achieve efficiently. The rising prevalence of chronic diseases like orthopedic conditions and dental issues increases demand for personalized implants and prosthetics, reducing surgery times and improving patient recovery rates. Additionally, supportive government initiatives and FDA approvals for 3D-printed devices streamline market entry, fostering innovation and adoption across healthcare providers.

Restraints

High initial costs for 3D printing equipment and materials pose a significant barrier, particularly for smaller healthcare facilities in developing regions, limiting widespread adoption. Regulatory challenges, including stringent quality control and certification processes, can delay product launches and increase compliance expenses. Moreover, limited reimbursement policies for 3D-printed devices in some countries hinder market growth by affecting affordability for patients and providers.

Opportunities

The integration of AI and machine learning in design software presents opportunities to optimize device customization and predict patient outcomes more accurately. Emerging applications in bioprinting for tissue and organ fabrication could revolutionize regenerative medicine, opening new revenue streams. Expanding into untapped markets in Asia-Pacific and Latin America, where healthcare infrastructure is improving, offers potential for partnerships and localized manufacturing to meet rising demand.

Challenges

Material limitations, such as ensuring long-term biocompatibility and strength for implants, remain a challenge, requiring ongoing R&D to develop advanced biomaterials. Intellectual property issues and cybersecurity risks in digital design files could impede innovation and trust in the technology. Supply chain disruptions for specialized materials and skilled workforce shortages in operating 3D printers also pose operational hurdles for manufacturers.

3D Printed Medical Devices Market: Report Scope

| Report Attributes | Report Details |

| Report Name | 3D Printed Medical Devices Market |

| Market Size 2025 | USD 4.37 Billion |

| Market Forecast 2035 | USD 18.84 Billion |

| Growth Rate | CAGR of 15.7% |

| Report Pages | 240 |

| Key Companies Covered |

3D Systems, Stratasys, Materialise, EOS GmbH, SLM Solutions, Renishaw, EnvisionTEC, General Electric, and Others |

| Segments Covered | By Technology, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Market Segmentation for 3D Printed Medical Devices Structured?

The 3D Printed Medical Devices market is segmented by technology, application, end-user, and region.

Based on Technology Segment. Laser Beam Melting is the most dominant subsegment, followed by Photopolymerization as the second most dominant. Laser Beam Melting leads due to its ability to produce high-strength metal implants with intricate designs, driving the market by enabling durable, biocompatible orthopedic and dental applications that enhance surgical precision and patient outcomes; Photopolymerization supports growth through cost-effective resin-based printing for surgical models and guides, facilitating rapid prototyping and customization in clinical settings.

Based on Application Segment. Prosthetics and Implants is the most dominant subsegment, followed by Surgical Guides as the second most dominant. Prosthetics and Implants dominate because they allow for patient-specific tailoring that improves fit, reduces rejection rates, and accelerates recovery, propelling market expansion in orthopedics and craniofacial procedures; Surgical Guides contribute by providing accurate preoperative planning tools that minimize surgical errors and time, boosting efficiency in complex operations.

Based on End-User Segment. Hospitals and Clinics is the most dominant subsegment, followed by Pharma and Biotech Companies as the second most dominant. Hospitals and Clinics lead owing to point-of-care printing capabilities that enable immediate customization of devices, driving the market through enhanced surgical workflows and cost savings; Pharma and Biotech Companies advance growth via R&D in bioprinting for drug testing and tissue models, fostering innovation in personalized medicine.

What are the Recent Developments in 3D Printed Medical Devices?

- In November 2024, HP introduced advancements in metal 3D printing and polymer technologies, along with partnerships to expand additive manufacturing in various medical applications, enhancing accessibility and precision for device production.

- In November 2024, 3D Systems unveiled next-generation Stereolithography (SLA) and Figure 4 portfolios at Formnext 2024, designed to accelerate the creation of production-grade medical parts with improved speed and accuracy.

- In September 2025, Croom Medical launched Biofuse, a 3D-printed porous ingrowth substrate using Laser-Powder-Bed-Fusion technology, allowing orthopedic implant manufacturers to control pore size and lattice gradients for better integration.

- In October 2025, CustoMED secured USD 6 million in funding to advance its 3D printing initiatives for customized medical devices, supporting expansion in personalized healthcare solutions.

- In March 2025, surgeons in Basel implanted the first MDR-compliant 3D-printed PEEK facial implant, demonstrating reduced supply chain dependencies and improved dimensional accuracy for craniofacial reconstructions.

- In February 2025, Stratasys Direct’s Tucson facility achieved ISO 13485 certification, ensuring compliance for medical device manufacturing and strengthening its position in producing high-quality 3D-printed components.

How does Regional Analysis Impact 3D Printed Medical Devices Market?

North America to dominate the global market.

North America leads the market, primarily driven by the United States as the dominating country, due to robust R&D investments, advanced healthcare systems, and rapid FDA approvals that facilitate innovation in personalized implants and surgical tools, with Canada contributing through growing adoption in academic research.

Europe holds a significant share, with Germany as the dominating country, supported by strong manufacturing expertise and EU regulatory frameworks promoting bioprinting advancements, while the UK and France enhance growth through collaborations in orthopedic and dental applications.

Asia-Pacific is experiencing the fastest growth, led by China as the dominating country, fueled by increasing healthcare expenditure and local manufacturing capabilities, with Japan and India adding momentum via technological integrations in prosthetics and rising medical tourism.

Latin America shows emerging potential, with Brazil as the dominating country, driven by improving infrastructure and demand for affordable customized devices, supported by Mexico’s focus on cross-border partnerships in surgical instruments.

The Middle East and Africa region is gradually expanding, with South Africa as the dominating country, propelled by investments in healthcare modernization and adoption of 3D printing for prosthetics, while the UAE contributes through innovation hubs in medical technology.

Who are the Key Market Players in 3D Printed Medical Devices?

- 3D Systems focuses on expanding its healthcare portfolio through innovations in SLA and Figure 4 technologies, emphasizing partnerships with hospitals for point-of-care printing and regulatory clearances to accelerate adoption in implants and surgical planning.

- Stratasys employs strategies like ISO certifications and collaborations with medical institutions to enhance material offerings, prioritizing R&D in biocompatible polymers and metals to support customized prosthetics and expand in emerging markets.

- Materialise leverages software expertise via Mimics Innovation Suite, pursuing acquisitions and alliances with device manufacturers to integrate AI-driven design tools, aiming to streamline workflows and capture value in personalized medicine.

- EOS GmbH concentrates on metal 3D printing advancements, forming strategic partnerships with orthopedic firms and investing in sustainable materials to meet regulatory standards and drive growth in high-precision implants.

- SLM Solutions adopts a focus on laser-based technologies, engaging in joint ventures for bioprinting research and expanding service networks to provide end-to-end solutions for cranio-maxillofacial and dental applications.

- Renishaw implements vertical integration strategies, combining metal additive manufacturing with metrology expertise, and collaborates on clinical trials to validate neural and spinal devices, targeting premium segments.

- EnvisionTEC pursues market penetration through affordable desktop printers for clinics, emphasizing material diversity and software updates to enable rapid prototyping in tissue engineering and hearing aids.

- General Electric utilizes its additive division for large-scale production, forming ecosystems with software providers and healthcare giants to innovate in bioprinting and secure long-term contracts in radiology-guided devices.

What are the Market Trends in 3D Printed Medical Devices?

- Rising integration of AI and machine learning in design software for optimized device customization and predictive modeling.

- Growing focus on sustainable and biocompatible materials to reduce environmental impact and improve long-term implant performance.

- Expansion of point-of-care 3D printing in hospitals for immediate surgical planning and cost-effective prototyping.

- Increasing adoption of bioprinting for tissue and organ fabrication, advancing regenerative medicine applications.

- Regulatory advancements and streamlined approvals accelerating market entry for patient-specific devices.

- Shift toward mass customization in orthopedics and dentistry to address aging populations and chronic conditions.

- Collaborations between tech firms and healthcare providers to enhance supply chain resilience and localization.

What Market Segments and their Subsegments are Covered in the 3D Printed Medical Devices Report?

By Technology

- Laser Beam Melting

- Photopolymerization

- Droplet Deposition

- Electron Beam Melting

- Others

By Application

- Surgical Guides

- Surgical Instruments

- Prosthetics and Implants

- Tissue Engineering

- Others

By End-User

- Hospitals and Clinics

- Academic Institutions

- Pharma and Biotech Companies

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

3D printed medical devices are customized tools, implants, and equipment produced using additive manufacturing techniques, layering materials to create precise, patient-specific solutions for applications like surgery and prosthetics.

Key factors include technological advancements in printing materials, rising demand for personalized healthcare, increasing chronic disease prevalence, and supportive regulatory frameworks.

The market is projected to grow from approximately USD 5.06 billion in 2026 to USD 18.84 billion by 2035.

The CAGR is expected to be 15.7% during 2026-2035.

North America will contribute notably, driven by advanced infrastructure and high innovation adoption.

Major players include 3D Systems, Stratasys, Materialise, EOS GmbH, and SLM Solutions.

The report provides comprehensive analysis including size, trends, segments, key players, regional insights, and forecasts.

Stages include material sourcing, design and software development, printing and fabrication, quality testing, regulatory approval, and distribution to end-users.

Trends show a shift toward bioprinting and sustainable materials, with consumers preferring personalized, cost-effective devices that improve outcomes.

Stringent FDA and EU regulations ensure safety but can delay launches, while environmental concerns push for eco-friendly materials and waste reduction in printing processes.