3D Printed Medical Device Market Size, Share and Trends 2026 to 2035

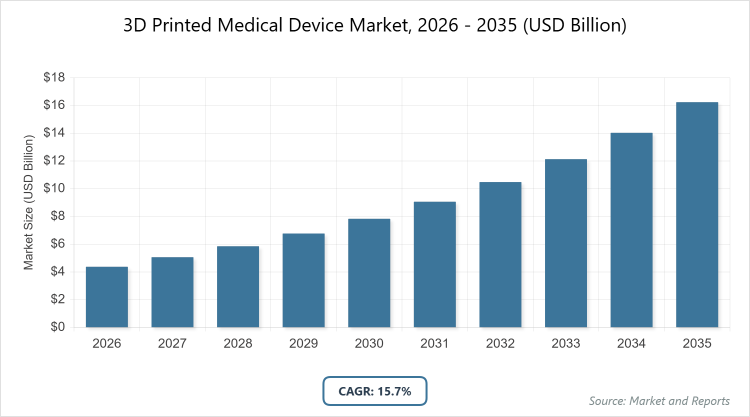

According to MarketnReports, the global 3D Printed Medical Device market size was estimated at USD 4.37 billion in 2025 and is expected to reach USD 18.84 billion by 2035, growing at a CAGR of 15.7% from 2026 to 2035. The 3D Printed Medical Device Market is driven by rising demand for personalized medical solutions and technological advancements in additive manufacturing.

What are the Key Insights into 3D Printed Medical Device?

- The global 3D Printed Medical Device market was valued at USD 4.37 billion in 2025 and is projected to reach USD 18.84 billion by 2035.

- The market is expected to grow at a CAGR of 15.7% during the forecast period from 2026 to 2035.

- The market is driven by increasing chronic diseases, aging populations, advancements in 3D printing materials, and demand for patient-specific devices.

- In the type segment, prosthetics & implants dominate with a 40% share due to their customization capabilities for better fit and functionality in orthopedic and dental applications.

- In the application segment, orthopedics dominates with a 35% share as it benefits from precise joint replacements and trauma repairs, reducing surgery complications.

- In the end-user segment, hospitals dominate with a 45% share owing to integration with surgical workflows for on-demand device fabrication.

- North America dominates the regional market with a 40% share, driven by advanced R&D, high healthcare spending, and supportive FDA regulations.

What is the Industry Overview of 3D Printed Medical Device?

The 3D Printed Medical Device market involves the use of additive manufacturing technologies to produce customized medical tools, implants, and prosthetics that offer precise anatomical fits, reduced production times, and enhanced biocompatibility for improved patient outcomes. Market definition includes devices fabricated layer-by-layer from biocompatible materials like metals, polymers, and ceramics based on digital models from medical imaging, enabling complex geometries, porosity for tissue integration, and rapid prototyping while addressing regulatory compliance, material safety, and scalability for applications in surgery, orthopedics, and dentistry.

What are the Market Dynamics of 3D Printed Medical Device?

Growth Drivers

The 3D Printed Medical Device market is propelled by the rising need for personalized healthcare solutions, where additive manufacturing allows for patient-specific designs that improve implant integration, reduce rejection rates, and shorten recovery times in orthopedics and dentistry. Technological advancements in multi-material printing and bioprinting enable the creation of complex structures with embedded sensors or drug-eluting features, expanding applications in regenerative medicine and drug delivery. Increasing prevalence of chronic conditions like osteoarthritis and cardiovascular diseases, coupled with an aging global population, drives demand for cost-effective, customized devices. Government initiatives funding 3D printing research and favorable reimbursement policies for innovative treatments further accelerate adoption and market growth.

Restraints

High initial costs for 3D printers, specialized materials, and regulatory certifications limit accessibility for smaller healthcare facilities and in developing regions, where traditional manufacturing remains more economical. Stringent approval processes from agencies like the FDA and EMA require extensive clinical validation for safety and efficacy, delaying product commercialization and increasing expenses. Limited standardization in printing protocols and material properties can result in variability in device quality and performance. Supply chain dependencies for biocompatible filaments and powders, along with intellectual property challenges in design sharing, further constrain expansion.

Opportunities

Opportunities arise from the integration of AI and machine learning for optimized device design and predictive simulations, enabling faster iterations and personalized outcomes in complex surgeries. Expansion into bioprinting for organoids and vascularized tissues offers potential in transplant medicine, addressing organ shortages. Partnerships with hospitals for point-of-care printing reduce lead times and costs, while sustainable, bioresorbable materials appeal to eco-conscious markets. Emerging economies with improving healthcare infrastructure present untapped demand for affordable prosthetics, and advancements in 4D printing for adaptive devices open futuristic applications.

Challenges

Challenges include ensuring long-term biocompatibility and mechanical reliability of printed devices under bodily stresses, necessitating rigorous testing to prevent failures like implant breakage. Scalability from prototypes to high-volume production is limited by print speeds and quality control, impacting cost competitiveness. Skill gaps in 3D design and printing among medical professionals hinder widespread use, while cybersecurity risks in digital files threaten patient data. Varying global regulations complicate international trade, and environmental concerns over plastic waste require greener manufacturing practices.

3D Printed Medical Device Market: Report Scope

| Report Attributes | Report Details |

| Report Name | 3D Printed Medical Device Market |

| Market Size 2025 | USD 4.37 Billion |

| Market Forecast 2035 | USD 18.84 Billion |

| Growth Rate | CAGR of 15.7% |

| Report Pages | 225 |

| Key Companies Covered | 3D Systems Corporation, Stratasys Ltd., Materialise NV, GE Additive, EnvisionTEC (Desktop Metal), Organovo Holdings, Inc., SLM Solutions Group AG, Oxford Performance Materials, Inc., and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of 3D Printed Medical Device?

The 3D Printed Medical Device market is segmented by type, application, end-user, and region.

By Type. Prosthetics & implants are the most dominant subsegment, holding approximately 40% market share, due to their ability to provide tailored fits that enhance patient comfort and functionality. This dominance drives the market by addressing diverse needs in amputation and joint replacement, lowering costs through reduced waste. Surgical guides rank as the second most dominant, with around 25% share, offering precise preoperative planning, propelling growth via minimized surgical errors and shorter operation times.

By Application. Orthopedics emerges as the most dominant subsegment, capturing about 35% share, primarily because it allows for custom bone and joint devices. This leads to market growth by improving surgical accuracy and patient recovery in high-demand trauma cases. Dental follows as the second most dominant, with a roughly 20% share, enabling personalized crowns and aligners, driving the market through aesthetic and functional advancements in oral care.

By End-User. Hospitals dominate at about 45% share, driven by on-site customization capabilities. This dominance accelerates market expansion through efficient patient care integration. Academic institutions rank second at around 20% share, using devices for research and training, contributing to growth via innovation and skill development.

What are the Recent Developments in 3D Printed Medical Device?

- In September 2025, Stratasys launched new biocompatible materials for dental 3D printing, enhancing precision in crown and bridge production.

- In July 2025, Materialise received FDA clearance for its Mimics Planner for orthopedic surgery, improving preoperative planning with 3D models.

- In May 2025, 3D Systems partnered with a biotech firm to develop bio-printed vascular structures for organ implants.

- In March 2025, GE Additive expanded its medical portfolio with new metal printing capabilities for spinal implants.

- In January 2025, EnvisionTEC introduced high-resolution printers for custom hearing aids, targeting audiology clinics.

What is the Regional Analysis of 3D Printed Medical Device?

- North America is expected to dominate the global market.

North America holds the largest share at approximately 40%, with the United States as the dominating country, due to advanced R&D, high healthcare spending, and supportive FDA regulations. This region’s growth is fueled by a strong biotech ecosystem and demand for custom implants amid rising chronic diseases. The presence of leading universities and research centers like MIT and Johns Hopkins drives innovation in bioprinting and material science. High insurance reimbursement for personalized devices encourages hospital adoption. Canada’s investment in healthcare technology through CIHR grants supports regional cohesion. Venture capital funding in Silicon Valley and Boston accelerates startups specializing in patient-specific solutions. Strategic partnerships between device manufacturers and hospitals enable point-of-care printing trials.

Europe follows with steady growth, driven by EU funding for medtech and emphasis on personalized medicine, where Germany dominates through engineering expertise and companies like EOS. The region’s expansion benefits from aging populations and regulatory harmonization. Horizon Europe initiatives allocate billions for additive manufacturing in healthcare. The UK’s NHS pilots 3D printed devices for cost-effective surgeries. France’s strong pharmaceutical base integrates printing for drug-device combinations. Italy and Spain focus on dental and craniofacial applications. Multilingual regulatory support under EMA facilitates cross-border approvals. Sustainability directives promote bioresorbable materials, reducing long-term environmental impact.

Asia Pacific is the fastest-growing region, with China leading due to its manufacturing capabilities and government initiatives for healthcare innovation. This area’s potential is enhanced by low costs and rising medical tourism. Massive investments under Made in China 2025 build advanced printing facilities. India’s medtech hubs in Bangalore develop affordable prosthetics for rural patients. Japan’s precision engineering excels in orthopedic implants for elderly care. South Korea’s biotech investments target regenerative applications. Southeast Asian nations like Singapore establish centers of excellence for clinical trials. Rapid urbanization increases demand for trauma and reconstructive devices.

Latin America demonstrates moderate progress, dominated by Brazil’s expanding healthcare sector, supported by foreign investments though challenged by economic variability. Mexico leverages nearshoring for collaborative R&D with U.S. firms. Government programs in Argentina train surgeons in 3D planning software. Chile’s private clinics adopt for high-end cosmetic reconstructions. Colombia’s growing biotech scene focuses on veterinary applications. However, reimbursement gaps slow institutional uptake. Emerging medical tourism in Costa Rica demands customized, high-quality implants at competitive prices.

The Middle East and Africa remain emerging, with the UAE leading through medical tourism and smart health projects, limited by infrastructure but promising via diversification. Saudi Arabia’s Vision 2030 funds national 3D printing labs for orthopedic devices. Israel’s startup ecosystem innovates in cranio-maxillofacial solutions. South Africa’s universities pioneer low-cost prosthetics for trauma victims. Egypt partners with European firms for technology transfer. However, regulatory harmonization lags in many areas. Investments in mobile printing units address accessibility in remote regions.

What are the Key Market Players in 3D Printed Medical Device?

- 3D Systems Corporation. 3D Systems focuses on biocompatible materials and surgical planning software, leveraging partnerships for orthopedic applications.

- Stratasys Ltd. emphasizes multi-material printing for dental and surgical guides, investing in R&D for enhanced precision.

- Materialise NV. Materialise specializes in design software for custom implants, pursuing collaborations with hospitals for point-of-care solutions.

- GE Additive. GE Additive targets metal implants with electron beam melting, focusing on aerospace-grade quality for medical use.

- EnvisionTEC (Desktop Metal). EnvisionTEC offers resin-based printing for hearing aids, strategizing on high-resolution custom devices.

- Organovo Holdings, Inc. advances bioprinting for tissue implants, investing in regenerative medicine.

- SLM Solutions Group AG. SLM Solutions develops laser-based metal printing for spinal implants, targeting scalable production.

- Desktop Metal, Inc. focuses on affordable metal printing, expanding through acquisitions for medical applications.

What are the Market Trends in 3D Printed Medical Device?

- Increasing adoption of bioprinting for tissue and organ fabrication.

- Rise of multi-material printing for functional devices.

- Integration of AI in design and simulation.

- Focus on bioresorbable and sustainable materials.

- Expansion of point-of-care 3D printing in hospitals.

- Growth in wearable and implantable sensors.

What Market Segments and Subsegments are Covered in the 3D Printed Medical Device Report?

By Type

- Surgical Guides

- Surgical Instruments

- Prosthetics & Implants

- Tissue Engineering Products

- Dental Devices

- Orthopedic Devices

- Cranio-Maxillofacial Devices

- Hearing Aids

- Custom Braces

- Bio-Printed Organs

- Others

By Application

- Orthopedic

- Dental

- Craniomaxillofacial

- Internal Implants

- External Prosthetics

- Wearables

- Research & Development

- Education

- Veterinary Medicine

- Drug Delivery Devices

- Others

By End-User

- Hospitals

- Ambulatory Surgical Centers

- Diagnostic Centers

- Academic Institutions

- Medical Device Companies

- Pharmaceutical Companies

- Biotechnology Firms

- Contract Research Organizations

- Specialty Clinics

- Dental Clinics

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

3D Printed Medical Devices are customized tools, implants, and prosthetics created using additive manufacturing for precise, patient-specific healthcare applications.

Key factors include technological advancements, rising chronic diseases, aging populations, and demand for personalized devices.

The market is projected to grow from USD 4.37 billion in 2025 to USD 18.84 billion by 2035.

The CAGR is expected to be 15.7%.

North America will contribute notably, holding around 40% share due to advanced R&D and regulations.

Major players include 3D Systems, Stratasys, Materialise, GE Additive, and EnvisionTEC.

The report provides comprehensive analysis of size, trends, segments, regions, players, and forecasts.

Stages include material sourcing, digital modeling, printing, post-processing, testing, and distribution.

Trends evolve toward bioprinting and personalization, with preferences for biocompatible, sustainable devices.

Regulatory approvals like FDA and environmental concerns over materials influence compliance and sustainability.