Overcapacity Issues Market Size, Share and Trends 2026 to 2035

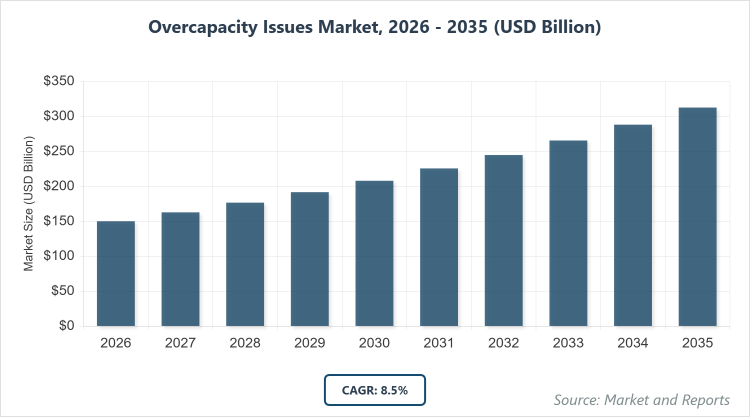

According to MarketnReports, the global Overcapacity Issues Market size was estimated at USD 150 billion in 2025 and is expected to reach USD 350 billion by 2035, growing at a CAGR of 8.5% from 2026 to 2035. Overcapacity Issues Market is driven by escalating global supply-demand imbalances in key industries and increasing demand for optimization solutions.

What are the Key Insights into the Overcapacity Issues Market?

- The global Overcapacity Issues Market was valued at USD 150 billion in 2025.

- The market is projected to grow at a CAGR of 8.5% from 2026 to 2035.

- The Overcapacity Issues Market is driven by rising supply-demand mismatches in manufacturing sectors, technological advancements in optimization tools, and regulatory pressures to address economic inefficiencies.

- Capacity Optimization Services dominate the Product Type segment with approximately 40% share because they provide tailored strategies to reduce excess capacity, improving profitability and resource efficiency in overproduced industries.

- Manufacturing Overcapacity Management dominates the Application segment with around 35% share as industries like steel and automotive face chronic surpluses, necessitating specialized solutions for production adjustments.

- Industrial Manufacturers dominate the End-User segment with over 45% share since they are directly impacted by overcapacity, driving demand for tools to streamline operations and avoid financial losses.

- Asia Pacific dominates the global market with 50% share due to China's leading role in global overproduction in sectors like steel and EVs, supported by government initiatives and rapid industrialization.

What is the Industry Overview of the Overcapacity Issues Market?

The Overcapacity Issues Market refers to the ecosystem of solutions, services, and technologies aimed at addressing excess production capacity in various industries, where supply significantly outpaces demand, leading to inefficiencies, price volatility, and economic pressures. This market includes consulting, software tools, and strategies for capacity rationalization, demand forecasting, and sustainable scaling to mitigate risks like wasted resources and market distortions. The market definition encompasses interventions that help industries realign production with market needs, promote efficient resource allocation, and support regulatory frameworks to prevent chronic overproduction, particularly in sectors like manufacturing, energy, and commodities, fostering resilience in global supply chains.

What are the Market Dynamics of the Overcapacity Issues Market?

Growth Drivers

The Overcapacity Issues Market is propelled by the proliferation of excess production in key global industries, exacerbated by rapid industrialization in emerging economies and fluctuating demand patterns, prompting the need for advanced management solutions to prevent economic downturns. Technological integrations like AI-driven forecasting and IoT for real-time monitoring enhance decision-making, while international trade tensions and sustainability mandates encourage investments in capacity optimization, fostering market growth through collaborative efforts between governments and private sectors to achieve balanced supply chains.

Restraints

Significant restraints stem from the high implementation costs of sophisticated optimization technologies and consulting services, which deter small and medium enterprises in overcapacity-prone sectors from adopting solutions. Additionally, varying regulatory environments across regions create compliance challenges, while resistance to operational changes in traditional industries like steel limits market penetration, compounded by data privacy concerns in digital tools.

Opportunities

Opportunities arise from the integration of green technologies and circular economy principles to repurpose excess capacity, particularly in energy-intensive sectors transitioning to renewables. Emerging markets in Asia and Africa offer expansion potential through localized solutions, while partnerships with tech firms for blockchain-based supply tracking can unlock new revenue streams, addressing global imbalances amid shifting trade dynamics.

Challenges

Challenges include navigating geopolitical tensions that exacerbate overcapacity through export surges and tariffs, as seen in China's steel sector, alongside difficulties in accurate demand prediction amid economic volatility. Workforce reskilling for optimized operations and ensuring interoperability of diverse management tools across industries pose ongoing hurdles, requiring adaptive strategies for effective resolution.

Overcapacity Issues Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Overcapacity Issues Market |

| Market Size 2025 | USD 150 Billion |

| Market Forecast 2035 | USD 350 Billion |

| Growth Rate | CAGR of 8.5% |

| Report Pages | 220 |

| Key Companies Covered |

Deloitte, McKinsey & Company, Boston Consulting Group, KPMG, PwC. and Others. |

| Segments Covered | By Product Type, By Application, By End-User, and By Region. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of the Overcapacity Issues Market?

The Overcapacity Issues Market is segmented by Product Type, Application, End-User, and region.

By Product Type Segment, Capacity Optimization Services represent the most dominant segment while Supply Chain Management Solutions stand as the second most dominant. Capacity Optimization Services lead due to their comprehensive approach in assessing and restructuring production lines to match demand, driving market growth by enabling cost savings and preventing price collapses in saturated sectors like manufacturing.

By Application Segment, Manufacturing Overcapacity Management is the most dominant segment followed by Energy Sector Adjustment as the second most dominant. Manufacturing Overcapacity Management dominates as it targets high-impact industries with chronic surpluses, propelling market expansion through targeted interventions that enhance competitiveness and sustainability.

By End-User Segment, Industrial Manufacturers is the most dominant while Government Agencies constitute the second most dominant. Industrial Manufacturers prevail owing to their direct exposure to production excesses, supporting market growth by adopting solutions that streamline operations and foster innovation in response to global pressures.

What are the Recent Developments in the Overcapacity Issues Market?

- In 2025, the OECD highlighted a surge in global steel overcapacity to over 680 million metric tons, prompting new international collaborations for capacity reduction strategies.

- China announced policy reforms in early 2026 to curb excess production in EVs and solar panels, integrating AI tools for better demand forecasting.

- The EU launched a 2025 initiative with subsidies for green steel projects to address overcapacity while promoting sustainable practices.

- Major consulting firms like Deloitte expanded their overcapacity advisory services in 2026, focusing on Asia Pacific markets amid trade tensions.

What is the Regional Analysis of the Overcapacity Issues Market?

Asia Pacific to dominate the global market

Asia Pacific commands the largest share, led by China with its massive overproduction in steel and manufacturing, driven by rapid industrialization, government subsidies, and export strategies that necessitate advanced management solutions.

North America exhibits strong growth, dominated by the United States through trade policies addressing import surges and investments in domestic capacity optimization technologies.

Europe focuses on regulatory-driven adjustments, with Germany leading in sustainable reforms to tackle steel and automotive surpluses amid energy transitions.

Latin America shows emerging trends, spearheaded by Brazil via resource-based industries seeking tools to balance mining and agriculture overcapacities.

The Middle East and Africa are developing, with the UAE pioneering diversification efforts to manage oil-related industrial excesses through consulting partnerships.

Who are the Key Market Players in the Overcapacity Issues Market?

Deloitte employs data analytics and policy advisory strategies to help clients in overproduced sectors realign capacities with market demands.

McKinsey & Company focuses on digital transformation tools for supply chain optimization, targeting manufacturing clients amid global imbalances.

Boston Consulting Group prioritizes sustainability integrations, advising on green transitions to mitigate overcapacity risks.

KPMG adopts regulatory compliance frameworks, partnering with governments for industry-wide capacity adjustments.

PwC leverages AI forecasting platforms to drive proactive strategies in energy and automotive sectors.

What are the Market Trends in the Overcapacity Issues Market?

- Increasing adoption of AI and predictive analytics for real-time demand forecasting to prevent overproduction.

- Shift toward sustainable practices, including circular economy models to repurpose excess capacity.

- Growth in international trade agreements aimed at curbing export-driven overcapacity.

- Expansion of digital platforms for inventory and asset management in manufacturing.

- Rising focus on regional diversification to balance global supply chains.

- Integration of blockchain for transparent capacity tracking across industries.

- Emphasis on workforce reskilling programs to adapt to optimized production levels.

What Market Segments and their Subsegments are Covered in the Report?

By Product Type

- Capacity Optimization Services

- Supply Chain Management Solutions

- Demand Forecasting Tools

- Asset Utilization Software

- Production Scaling Technologies

- Inventory Management Systems

- Market Intelligence Platforms

- Consulting and Advisory Services

- Regulatory Compliance Tools

- Sustainability Integration Solutions

- Others

By Application

- Manufacturing Overcapacity Management

- Energy Sector Adjustment

- Transportation and Logistics Optimization

- Construction Capacity Balancing

- Automotive Production Scaling

- Steel and Metals Regulation

- Chemical Industry Control

- Textile and Apparel Adjustment

- Electronics Supply Management

- Food and Beverage Inventory

- Others

By End-User

- Industrial Manufacturers

- Government Agencies

- Consulting Firms

- Supply Chain Companies

- Energy Providers

- Automotive OEMs

- Construction Companies

- Logistics Providers

- Trade Organizations

- Financial Institutions

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions

The Overcapacity Issues Market involves solutions and services to address excess production capacity exceeding demand in various industries, focusing on optimization and balancing strategies.

Key factors include global trade tensions, technological advancements in forecasting, regulatory reforms, and shifts toward sustainable production in overproduced sectors.

The market is expected to grow from approximately USD 150 billion in 2026 to USD 350 billion by 2035.

The CAGR is projected to be 8.5% during the forecast period.

Asia Pacific will contribute notably, driven by China's dominant role in global overproduction and related management needs.

Major players include Deloitte, McKinsey & Company, Boston Consulting Group, KPMG, and PwC.

The report provides detailed analysis of market size, dynamics, segmentation, trends, regional insights, and competitive strategies.

Stages include assessment of capacity gaps, development of optimization tools, implementation of strategies, monitoring and adjustment, and regulatory compliance.

Trends favor AI-driven solutions and sustainability, while preferences shift toward integrated platforms for efficient capacity management.

Factors include trade tariffs, emission regulations, and government policies aimed at reducing industrial surpluses for environmental sustainability.