North America Frozen Bakery Products Market Size, Share and Trends 2026 to 2035

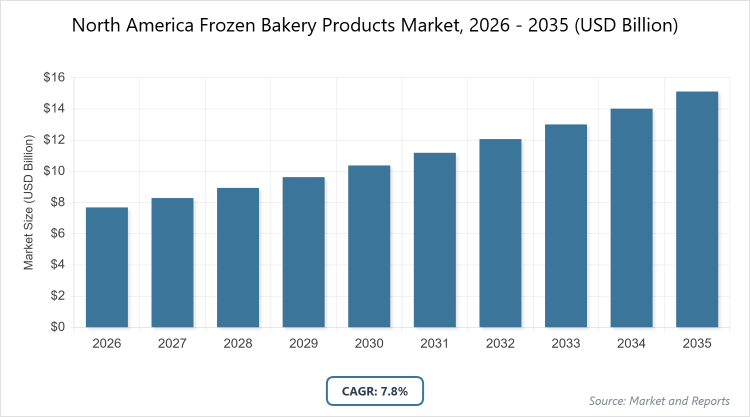

According to MarketnReports, the North America Frozen Bakery Products market size was estimated at USD 7.69 billion in 2025 and is expected to reach USD 16.5 billion by 2035, growing at a CAGR of 7.8% from 2026 to 2035. Increasing demand for convenient, ready-to-bake products amid busy lifestyles.

What are the Key Insights into the North America Frozen Bakery Products Market?

- The North America frozen bakery products market size was valued at USD 7.69 billion in 2025 and is projected to reach USD 16.5 billion by 2035.

- The North America frozen bakery products market is expected to grow at a CAGR of 7.8% during the forecast period from 2026 to 2035.

- The North America frozen bakery products market is driven by rising consumer preference for convenient foods, expansion of quick-service restaurants, and advancements in freezing technologies.

- In the product type segment, bread dominates with a 40% share due to its staple status, versatility in daily meals, and high demand in both retail and foodservice for quick preparation.

- In the end-use segment, retail dominates with a 50% share owing to widespread supermarket availability and consumer shifts toward at-home baking convenience.

- In the distribution channel segment, supermarkets & hypermarkets dominate with a 45% share because of their extensive reach, promotional strategies, and ability to stock diverse frozen options.

- United States dominates the North America frozen bakery products market with an 80% share, driven by large consumer base, advanced cold chain infrastructure, and strong presence of key manufacturers.

What are the North America Frozen Bakery Products?

Industry Overview

North America’s frozen bakery products encompass a range of baked goods that are partially or fully baked, frozen, and distributed for later consumption, including breads, pastries, pizzas, and desserts designed for extended shelf life and ease of preparation. These products are manufactured using freezing technologies to preserve freshness, texture, and nutritional value without preservatives, catering to both commercial and household needs. The market definition refers to the regional industry focused on the production, distribution, and consumption of these certified or standardized frozen items within North America, emphasizing quality control, supply chain efficiency, and innovation to meet diverse consumer preferences while addressing food safety regulations. This sector supports the foodservice and retail landscapes by offering time-saving solutions that align with modern convenience trends and evolving dietary requirements.

What are the Market Dynamics in North America Frozen Bakery Products?

Growth Drivers

The North American frozen bakery products market is fueled by the escalating demand for convenience-oriented foods amid hectic urban lifestyles, where consumers seek quick, high-quality meal solutions without compromising on taste. Advancements in freezing and packaging technologies have enhanced product shelf life and maintained sensory attributes, encouraging wider adoption in households and foodservice outlets. Rising health consciousness has spurred innovation in healthier variants, such as low-sugar or gluten-free options, aligning with dietary trends and broadening market appeal. The expansion of quick-service restaurants and cafes, particularly in urban areas, drives bulk demand for ready-to-bake items that reduce labor costs and ensure consistency. Additionally, robust e-commerce growth and improved cold chain logistics facilitate easier access, supporting market penetration in remote areas and boosting overall consumption.

Restraints

High production and distribution costs associated with maintaining cold chains and specialized equipment restrain the North American frozen bakery products market, particularly for smaller manufacturers facing margin pressures. Stringent food safety regulations and certification requirements increase compliance burdens, potentially delaying product launches and elevating prices for end consumers. Consumer perceptions of frozen products as inferior to fresh baked goods in terms of quality and freshness hinder broader acceptance in premium segments. Supply chain disruptions, such as those from energy price fluctuations or transportation issues, affect availability and lead to inventory challenges. Moreover, competition from fresh bakery alternatives and private-label conventional products limits market share in price-sensitive demographics.

Opportunities

Opportunities in the North American frozen bakery products market arise from the growing trend toward plant-based and organic variants, catering to vegan and health-focused consumers seeking sustainable options. Integration of smart packaging and IoT for better traceability can enhance consumer trust and open premium pricing avenues. Expansion into untapped rural markets through enhanced distribution networks and partnerships with regional retailers presents growth potential. Innovations in flavor profiles and ethnic-inspired products can attract diverse demographics, including millennials and Gen Z. Furthermore, collaborations with e-commerce platforms for subscription models and customized bundles could capitalize on the shift to online shopping, driving incremental sales.

Challenges

Challenges in the North American frozen bakery products market include maintaining product quality during thawing and baking, as inconsistencies can lead to consumer dissatisfaction and returns. Environmental concerns over packaging waste and energy-intensive freezing processes pressure manufacturers to adopt sustainable practices amid regulatory scrutiny. Fragmented supply chains with dependency on imported ingredients expose the market to global price volatilities and trade barriers. Educating consumers on the benefits of frozen over fresh remains difficult, especially in regions with strong traditional baking cultures. Additionally, labor shortages in manufacturing and logistics complicate scaling operations to meet surging demand.

North America Frozen Bakery Products Market: Report Scope

| Report Attributes | Report Details |

| Report Name | North America Frozen Bakery Products Market |

| Market Size 2025 | USD 7.69 Billion |

| Market Forecast 2035 | USD 16.5 Billion |

| Growth Rate | CAGR of 7.8% |

| Report Pages | 220 |

| Key Companies Covered |

Dawn Food Products, Inc., General Mills, Inc., Bridgford Foods Corporation, Lantmannen, T. Marzetti Company, Aryzta AG, Associated British Foods Plc, Flowers Foods Inc., Grupo Bimbo S.A.B, Europastry S.A, and Others |

| Segments Covered | By Product Type, By End-Use, By Distribution Channel, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the North America Frozen Bakery Products Market Segmentation Analyzed?

The North America Frozen Bakery Products market is segmented by product type, end-use, distribution channel, and region.

Based on Product Type Segment, bread emerges as the most dominant subsegment, followed by cakes & pastries as the second most dominant. Bread leads due to its essential role in daily diets, high volume sales in retail and foodservice, and ease of freezing without quality loss; this dominance drives the market by supporting staple consumption patterns and enabling innovations like artisanal or whole-grain variants that cater to health trends, boosting overall category growth.

Based on the end-use segment, retail stands out as the most dominant subsegment, with food service industry as the second most dominant. Retail dominates because it offers convenient access for household consumers seeking ready-to-bake options amid busy schedules; this drives market expansion through increased shelf space in supermarkets and promotional activities that encourage trial and repeat purchases.

Based on the Distribution Channel Segment, supermarkets & hypermarkets are the most dominant subsegment, with the online channel as the second most dominant. Supermarkets & hypermarkets lead owing to their broad assortment, competitive pricing, and in-store visibility that attract bulk buyers; their dominance propels the market by facilitating mass distribution and integrating with loyalty programs to enhance consumer engagement.

What are the Recent Developments in North America Frozen Bakery Products?

- In January 2026, General Mills launched a new line of gluten-free frozen bread doughs, targeting health-conscious consumers and expanding its portfolio in the U.S. retail market.

- In March 2026, Aryzta AG introduced innovative frozen artisanal pastries with plant-based ingredients, partnering with major Canadian retailers to meet rising demand for vegan options.

- In April 2026, Grupo Bimbo announced the acquisition of a U.S.-based frozen bakery facility to enhance production capacity and supply chain efficiency in North America.

- In May 2025, Dawn Food Products unveiled eco-friendly packaging for its frozen donut range, aligning with sustainability trends and appealing to environmentally aware buyers.

- In June 2025, Flowers Foods Inc. expanded its frozen bagel offerings with organic variants, focusing on the growing clean-label segment in the foodservice industry.

How Does Regional Analysis Shape the North America Frozen Bakery Products Market?

- The United States is to dominate the global market.

The United States commands the North American frozen bakery products market with its vast consumer base and advanced retail infrastructure, where innovation in product varieties and strong demand from quick-service restaurants drive growth; the country’s dominance is reinforced by leading manufacturers and efficient cold chains that ensure widespread availability.

Canada contributes significantly to the North American frozen bakery products market through its multicultural population demanding diverse ethnic baked goods, with urban centers like Toronto leading adoption; government support for food innovation and expanding e-commerce enhances market accessibility amid cold climate preferences for convenient foods.

Mexico is emerging in the North American frozen bakery products market, propelled by urbanization and rising middle-class incomes, where traditional items like frozen tortillas blend with modern pastries; increasing foreign investments and retail expansions in cities like Mexico City bolster supply chains and consumer choices.

Who are the Key Market Players in North America Frozen Bakery Products?

- Dawn Food Products, Inc. focuses on innovation in premium frozen ingredients and partnerships with foodservice chains to expand its gluten-free and clean-label offerings.

- General Mills, Inc. emphasizes acquisitions and R&D for healthier frozen bakery variants, leveraging its strong distribution network for retail dominance.

- Bridgford Foods Corporation pursues cost-effective production and private-label strategies to serve convenience stores and supermarkets efficiently.

- Lantmannen invests in sustainable sourcing and plant-based products, targeting eco-conscious consumers through expanded Canadian operations.

- T. Marzetti Company develops ready-to-bake solutions for institutional buyers, focusing on quality assurance and flavor customization.

- Aryzta AG expands through mergers and technology upgrades for high-volume frozen bread production in the U.S.

- Associated British Foods Plc strengthens its portfolio with organic lines, utilizing marketing campaigns to boost foodservice adoption.

- Flowers Foods Inc. prioritizes regional expansions and artisan-style frozen goods to capture niche markets.

- Grupo Bimbo S.A.B leverages cross-border supply chains and e-commerce integrations for broad market penetration.

- Europastry S.A. innovates in ethnic pastries and collaborates with online platforms to enhance direct-to-consumer sales.

What are the Market Trends in North America Frozen Bakery Products?

- Increasing demand for gluten-free and plant-based frozen bakery items amid health trends.

- Growth in e-commerce and online delivery for convenient home baking solutions.

- Adoption of sustainable packaging to address environmental concerns.

- Rise in premium artisanal frozen products for foodservice differentiation.

- Expansion of clean-label and organic variants to attract conscious consumers.

- Integration of ethnic flavors in frozen bakery assortments.

- Focus on extended shelf-life technologies for reduced waste.

- Partnerships between manufacturers and retailers for private-label growth.

What Market Segments and Subsegments are Covered in the North America Frozen Bakery Products Report?

By Product Type

- Bread

- Pizza Crust

- Cakes & Pastries

- Waffles

- Donuts

- Cookies

- Muffins

- Bagels

- Croissants

- Pretzels

- Others

By End-Use

- Retail

- Food Service Industry

- Food Processing Industry

- Households

- Commercial Bakeries

- Quick Service Restaurants

- Hotels

- Cafes

- Institutional Catering

- Supermarkets

- Others

By Distribution Channel

- Bakery And Confectionery

- Retail

- Catering

- Online Channel

- Wholesale Distributors

- Convenience Stores

- Hypermarkets

- Specialty Stores

- Direct Sales

- E-commerce Platforms

- Others

By Region

- United States

- Canada

- Mexico

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global North America Frozen Bakery Products Market - Industry Analysis

Chapter 4. Global North America Frozen Bakery Products Market- Competitive Landscape

Chapter 5. Global North America Frozen Bakery Products Market - Product Type Analysis

Chapter 6. Global North America Frozen Bakery Products Market - End-Use Analysis

Chapter 7. Global North America Frozen Bakery Products Market - Distribution Channel Analysis

Chapter 8. North America Frozen Bakery Products Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

North America frozen bakery products are baked goods like bread, pastries, and pizzas that are frozen to extend shelf life, offering convenience for retail and foodservice use.

Key factors include convenience demand, health trends toward gluten-free options, e-commerce growth, and technological advancements in freezing.

The market is projected to grow from over USD 7.69 billion in 2025 to USD 16.5 billion by 2035.

The CAGR is expected to be 7.8% from 2026 to 2035.

The United States will contribute notably, driven by its large market size and innovation hub status.

Major players include Dawn Food Products, Inc., General Mills, Inc., Aryzta AG, Grupo Bimbo S.A.B, and Flowers Foods Inc.

The report provides in-depth analysis on size, trends, segments, key players, regional insights, and forecasts.

Stages include raw material sourcing, manufacturing and freezing, packaging, distribution, retail, and consumption.

Trends favor sustainable and healthy options, with consumers preferring convenient, plant-based, and gluten-free products.

Factors include food safety regulations, sustainability mandates, and environmental concerns over packaging waste.