Commercial Cold Equipment Market Size, Share and Trends 2026 to 2035

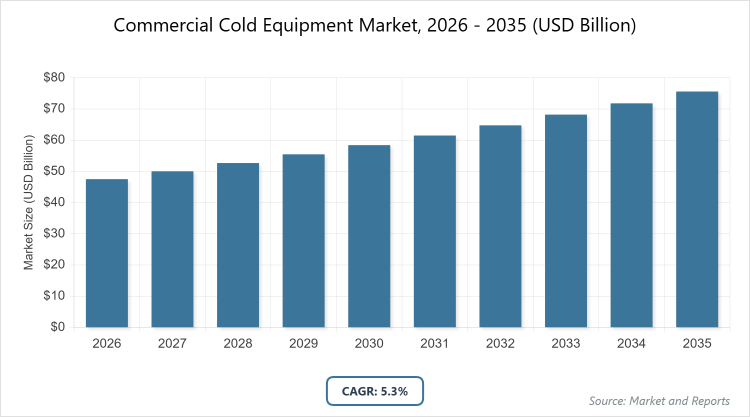

According to MarketnReports, the global Commercial Cold Equipment market size was estimated at USD 47.50 billion in 2025 and is expected to reach USD 79.61 billion by 2035, growing at a CAGR of 5.30% from 2026 to 2035. The rapid expansion of food retail and hospitality sectors along with increasing cold chain infrastructure.

What are the Key Insights into the Commercial Cold Equipment Market?

- The global Commercial Cold Equipment market was valued at USD 47.50 billion in 2025 and is projected to reach USD 79.61 billion by 2035.

- The market is expected to grow at a CAGR of 5.30% during the forecast period.

- The market is driven by increasing demand for energy-efficient refrigeration solutions and the expansion of cold chain logistics.

- The refrigerated display cases segment dominates the type segment with a 30% share & why it is because it enhances product visibility and impulse purchases in retail settings.

- The food & beverage retail segment dominates the application segment with a 35% share & why it is dominated due to the proliferation of supermarkets and convenience stores requiring reliable cooling for perishable items.

- The supermarkets & hypermarkets segment dominates the end-user segment with a 28% share & why it is dominated owing to high-volume storage needs and focus on fresh food offerings.

- North America dominates the global market with a 31% share & why it is dominated thanks to mature retail infrastructure and presence of major supermarket chains.

What is the Commercial Cold Equipment?

Industry Overview

The Commercial Cold Equipment market encompasses refrigeration systems and devices designed for business use, including storage, display, and transportation of perishable goods in sectors like food service, retail, and healthcare. Market definition includes equipment such as refrigerators, freezers, display cases, and walk-in coolers that maintain low temperatures to preserve the quality and safety of products, driven by the need for efficient cold chain management and compliance with food safety regulations.

What are the Market Dynamics in Commercial Cold Equipment?

Growth Drivers

The growth drivers in the Commercial Cold Equipment market are propelled by the expanding food and beverage industry, particularly in emerging economies, where rising disposable incomes boost demand for frozen and chilled products, necessitating advanced refrigeration solutions. Technological advancements in energy-efficient systems, such as variable speed compressors and natural refrigerants, reduce operational costs and align with sustainability goals, encouraging upgrades from outdated equipment.

The surge in e-commerce grocery delivery and hyperlocal logistics requires compact, reliable cold storage units for dark stores and last-mile delivery, expanding market reach. Stringent food safety regulations globally mandate precise temperature control, driving adoption of smart monitoring systems integrated with IoT for real-time data and compliance.

Restraints

Restraints in the Commercial Cold Equipment market include high initial investment costs for advanced, eco-friendly systems, which can deter small and medium enterprises from adopting new technologies despite long-term savings. Volatility in raw material prices, such as steel and refrigerants, impacts manufacturing costs and profitability, leading to price fluctuations that affect market stability. The phase-out of high-GWP refrigerants under international agreements like the Kigali Amendment requires costly retrofits and transitions, posing challenges for existing installations. Additionally, a lack of skilled technicians for installation and maintenance in developing regions hampers efficient deployment and service, limiting market penetration.

Opportunities

Opportunities in the Commercial Cold Equipment market arise from the growing adoption of sustainable practices, with demand for low-GWP refrigerants and solar-powered units opening avenues for innovation in green technologies. Expansion of healthcare and pharmaceutical sectors, especially post-pandemic, increases need for precise temperature-controlled storage for vaccines and biologics, creating specialized niches. Emerging markets in Asia-Pacific and Latin America offer potential through urbanization and retail chain growth, where partnerships with local players can facilitate customized solutions. Integration of AI and predictive analytics for maintenance and energy optimization presents new service models, such as subscription-based monitoring, enhancing customer retention and revenue streams.

Challenges

Challenges in the Commercial Cold Equipment market involve navigating complex regulatory landscapes for refrigerant usage and energy efficiency standards, which vary by region and require ongoing compliance efforts. Supply chain disruptions, exacerbated by global events, affect component availability and lead times, impacting production schedules. Intense competition from low-cost imports pressures pricing and margins, necessitating differentiation through quality and innovation. Finally, addressing environmental concerns like refrigerant leaks and energy consumption demands continuous R&D investment to develop leak-proof, efficient systems amid rising scrutiny from consumers and regulators.

Commercial Cold Equipment Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Commercial Cold Equipment Market |

| Market Size 2025 | USD 47.50 Billion |

| Market Forecast 2035 | USD 79.61 Billion |

| Growth Rate | CAGR of 5.30% |

| Report Pages | 220 |

| Key Companies Covered |

Carrier Global Corporation, Daikin Industries, Ltd., Danfoss A/S, Emerson Electric Co., GEA Group Aktiengesellschaft, Johnson Controls International plc, Hussmann Corporation, Panasonic Corporation, Lennox International Inc., True Manufacturing Co., Inc., and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Market Segmentation Done in Commercial Cold Equipment?

The Commercial Cold Equipment market is segmented by type, application, end-user, and region.

Based on the Type Segment, Refrigerated display cases emerge as the most dominant subsegment, holding approximately 30% market share, primarily because they provide optimal visibility and accessibility for products in retail environments, driving sales through impulse buys and helping market growth by supporting the expansion of supermarkets and convenience stores. Refrigerators & freezers follow as the second dominant, with around 25% share, valued for their essential role in bulk storage and preservation, contributing to market expansion by enabling efficient cold chain operations in food service and distribution.

Based on the Application Segment, Food & beverage retail stands out as the most dominant subsegment, capturing about 35% of the market, due to the increasing number of retail outlets requiring reliable cooling for fresh produce and dairy, which helps drive the market by enhancing product shelf life and consumer appeal. Food service ranks second with roughly 28% share, driven by demand in restaurants and hotels for consistent temperature control, propelling market growth through improved food safety and operational efficiency.

Based on the End-User Segment, Supermarkets & hypermarkets are the most dominant subsegment, accounting for 28% share, attributed to their large-scale operations needing extensive refrigeration for diverse product ranges, enhancing market drive by facilitating global food retail expansion. Hotels & restaurants follow with 22% share, fueled by hospitality sector growth and focus on quality preservation, which advances the market through innovative, energy-efficient solutions tailored to service needs.

What are the Recent Developments in Commercial Cold Equipment?

- In September 2025, Carrier Global Corporation acquired a European refrigeration startup specializing in CO2-based systems, investing USD 200 million to integrate sustainable technologies into its commercial portfolio.

- In November 2025, Daikin Industries launched a new line of AI-enabled commercial freezers with predictive maintenance features, reducing downtime by 25% for food retail applications.

- In January 2026, Emerson Electric Co. partnered with a major supermarket chain in North America to deploy energy-efficient condensing units, achieving 15% energy savings across 500 stores.

- In February 2026, Danfoss introduced advanced variable speed compressors for walk-in coolers, compliant with new EU energy regulations, targeting the growing European market.

- In March 2026, Johnson Controls expanded its production facility in Asia-Pacific, adding capacity for 100,000 units annually to meet rising demand in emerging markets.

What is the Regional Analysis of Commercial Cold Equipment?

- North America is expected to dominate the global market.

North America holds the largest share in the Commercial Cold Equipment market at 31%, driven by a mature retail sector and the presence of major chains like Walmart and Costco, with the United States dominating through high adoption of smart refrigeration and stringent food safety standards, supported by Canada’s focus on energy-efficient imports.

Asia Pacific is the fastest-growing region with a projected CAGR of 7%, fueled by urbanization and retail expansion in China and India, where China leads with massive investments in cold chain infrastructure for e-commerce and food exports.

Europe maintains a significant 25% share, characterized by strict environmental regulations promoting low-GWP systems, led by Germany and the UK in adopting sustainable technologies for hospitality and retail.

Latin America accounts for 8% of the market, with growth driven by increasing supermarket chains in Brazil and Mexico, where Brazil dominates through rising demand for frozen foods and improved logistics.

The Middle East and Africa represent 6% share, with the UAE and South Africa leading in hospitality and retail applications, supported by tourism growth and investments in cold storage for imports.

Who are the Key Market Players in Commercial Cold Equipment?

- Carrier Global Corporation. Carrier focuses on sustainable innovations, expanding its portfolio with natural refrigerant systems and IoT integrations for energy management in retail applications.

- Daikin Industries, Ltd. Daikin employs strategies centered on advanced compressor technologies and global expansions, targeting Asia-Pacific with eco-friendly solutions for food service.

- Danfoss A/S. Danfoss leverages R&D in variable speed drives and controls, partnering with OEMs to enhance efficiency in commercial freezers and display cases.

- Emerson Electric Co. emphasizes digital solutions and predictive analytics, providing components for smart refrigeration systems in supermarkets.

- GEA Group Aktiengesellschaft. GEA pursues industrial-scale projects, offering customized cooling solutions for food processing and distribution sectors.

- Johnson Controls International plc. Johnson Controls invests in building automation integrations, delivering energy-efficient HVAC-R systems for hospitality.

- Hussmann Corporation. Hussmann specializes in display merchandising, innovating LED-lit cases for retail to improve visibility and reduce energy use.

- Panasonic Corporation. Panasonic focuses on compact, high-efficiency units for convenience stores, incorporating inverter technology for cost savings.

- Lennox International Inc. Lennox targets North American markets with reliable condensing units, emphasizing service networks for maintenance.

- True Manufacturing Co., Inc. True Manufacturing adopts customizable designs for food service, using durable materials to ensure longevity in demanding environments.

What are the Market Trends in Commercial Cold Equipment?

- Adoption of natural and low-GWP refrigerants to comply with environmental regulations.

- Integration of IoT and AI for smart monitoring and predictive maintenance.

- Rise in energy-efficient systems with variable speed compressors.

- Growth in modular and compact units for hyperlocal delivery logistics.

- Expansion of eco-friendly solar-powered refrigeration in remote areas.

- Increasing demand for customized solutions in pharmaceutical cold chains.

- Focus on reducing food waste through advanced temperature controls.

- Surge in retrofitting older systems with modern, efficient components.

- Development of antimicrobial coatings for hygiene in food storage.

- Collaborations for sustainable supply chain improvements.

What Market Segments and their Subsegments are Covered in the Commercial Cold Equipment Report?

By Type

- Refrigerators & Freezers

- Transportation Refrigeration Equipment

- Refrigerated Display Cases

- Beverage Refrigeration

- Ice Machines

- Vending Machines

- Walk-in Coolers

- Reach-in Refrigerators

- Condensing Units

- Evaporators

- Others

By Application

- Food Service

- Food & Beverage Retail

- Food & Beverage Production

- Food & Beverage Distribution

- Pharmaceuticals

- Healthcare

- Industrial

- Logistics

- Supermarkets & Hypermarkets

- Convenience Stores

- Others

By End-User

- Hotels & Restaurants

- Supermarkets & Hypermarkets

- Convenience Stores

- Bakeries

- Hospitals

- Pharmaceutical Companies

- Food Processing Industries

- Retail Chains

- Catering Services

- Warehouses

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Commercial Cold Equipment Market - Industry Analysis

Chapter 4. Global Commercial Cold Equipment Market- Competitive Landscape

Chapter 5. Global Commercial Cold Equipment Market - Type Analysis

Chapter 6. Global Commercial Cold Equipment Market - Application Analysis

Chapter 7. Global Commercial Cold Equipment Market - End-User Analysis

Chapter 8. Commercial Cold Equipment Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Commercial cold equipment refers to refrigeration systems used in businesses for storing, displaying, and transporting perishable goods at controlled temperatures.

Key factors include expansion of retail sectors, adoption of energy-efficient technologies, stringent food safety regulations, and growth in cold chain logistics.

The market is projected to grow from approximately USD 50.02 billion in 2026 to USD 79.61 billion by 2035.

The CAGR is expected to be 5.30% during the forecast period.

North America will contribute notably, holding around 31% of the global market value due to advanced retail infrastructure.

Major players include Carrier Global Corporation, Daikin Industries, Ltd., Danfoss A/S, Emerson Electric Co., GEA Group Aktiengesellschaft, Johnson Controls International plc, Hussmann Corporation, Panasonic Corporation, Lennox International Inc., and True Manufacturing Co., Inc.

The report provides comprehensive analysis including market size, forecasts, segmentation, dynamics, regional insights, key players, trends, and FAQs.

The value chain includes raw material sourcing, component manufacturing, equipment assembly, distribution, installation, and after-sales service.

Trends are shifting towards sustainable, smart refrigeration systems, with consumers preferring energy-efficient, eco-friendly equipment for cost savings and compliance.

Regulatory factors include refrigerant phase-outs and energy efficiency standards, while environmental factors involve reducing carbon footprints through green technologies.