Europe Precision Medicine Market Size, Share and Trends 2026 to 2035

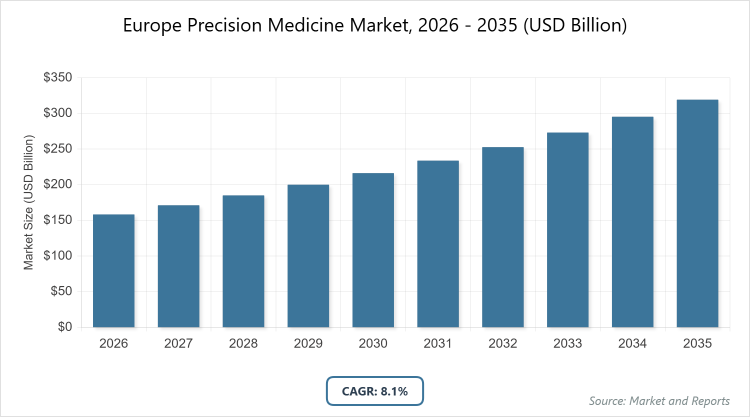

According to MarketnReports, the Europe Precision Medicine market size was estimated at USD 158.4 billion in 2025 and is expected to reach USD 346.7 billion by 2035, growing at a CAGR of 8.1% from 2026 to 2035. Declining costs of genetic sequencing and increasing adoption of targeted therapies.

What are the Key Insights into the Europe Precision Medicine Market?

- The Europe Precision Medicine market was valued at USD 158.4 billion in 2025 and is projected to reach USD 346.7 billion by 2035.

- The market is expected to grow at a CAGR of 8.1% during the forecast period.

- The market is driven by technological advancements in genomics and increasing government initiatives for precision healthcare.

- The gene sequencing segment dominates the technology segment with a 28% share & why it is dominated as it provides essential genomic data for personalized treatments, enabling accurate diagnosis and therapy selection.

- The oncology segment dominates the application segment with a 35% share & why it is dominated due to the high prevalence of cancer and the effectiveness of targeted therapies in improving patient outcomes.

- The hospitals segment dominates the end-user segment with a 41% share & why it is dominated owing to their role as primary care providers implementing precision medicine in clinical settings.

- Germany dominates the regional market with a 27% share & why it is dominated thanks to advanced research infrastructure and strong government support for genomic programs.

What is European Precision Medicine?

Industry Overview

The Europe Precision Medicine market involves tailoring medical treatment to individual characteristics, including genetic makeup, environment, and lifestyle factors, to optimize therapeutic outcomes and minimize adverse effects. Market definition encompasses technologies, diagnostics, and therapeutics that enable patient stratification, precision diagnostics, and targeted treatments across various diseases, supported by genomic data, biomarkers, and advanced analytics to deliver evidence-based, personalized healthcare solutions.

What are the Market Dynamics in Europe’s Precision Medicine?

Growth Drivers

The growth drivers in the Europe Precision Medicine market are fueled by declining costs of genetic sequencing and expanding genomic databases, making personalized approaches more accessible across healthcare systems. Increasing adoption of precision oncology and targeted therapies drives demand for companion diagnostics and biomarker testing. Technological advancements in AI and machine learning enhance genomic data analysis, accelerating biomarker discovery and improving predictive accuracy. Government initiatives, such as national precision medicine programs, promote research and infrastructure development. The pharmaceutical industry’s focus on biomarker-guided drug development expands market opportunities, with regulatory support for expedited approvals.

Rising healthcare investments in molecular diagnostics and next-generation sequencing facilities accelerate penetration. Growing demand for precision therapeutics in oncology, rare diseases, and chronic conditions supports pharmacogenomic testing. Advancements in sequencing technologies improve efficiency and accuracy, boosting provider confidence. Integration into clinical protocols and patient care pathways drives mainstream adoption.

Restraints

Restraints in the Europe Precision Medicine market include high costs for genetic testing and targeted therapies, posing challenges to widespread adoption. Complex regulatory requirements for personalized products delay market entry. Data privacy concerns and genetic information security influence patient acceptance. Insurance coverage limitations and reimbursement decisions restrict accessibility in smaller facilities. Specialized expertise needs for genetic counseling and interpretation limit implementation in community settings. Implementation complexity in clinical workflows hinders integration. Limited clinical evidence for some applications and unclear reimbursement policies create barriers. Ethical concerns and potential genetic discrimination reduce testing uptake.

Opportunities

Opportunities in the Europe Precision Medicine market emerge from growing therapeutic diversity in targeted biologics and companion diagnostics. National programs provide funding for genomic infrastructure. The development of genomic data infrastructure and biobanks enables research and clinical translation. Creation of reimbursement policies for validated tests supports utilization. Workforce development through training programs builds competency. The establishment of clinical practice guidelines standardizes protocols. Professional education enhances understanding of genomic medicine. Ethical guidelines ensure responsible implementation. Integrated platforms combine diagnostics with decision support. Clinical validation through studies demonstrates value. Patient engagement programs improve participation.

Challenges

Challenges in the Europe Precision Medicine market involve high costs for testing and therapies, complicating expansion. Regulatory complexities for products require navigation. Data privacy issues affect acceptance. Coverage limitations restrict access. Expertise requirements limit availability in regions. Workflow integration poses difficulties. Evidence gaps and policy uncertainties hinder implementation. Ethical concerns may limit utilization.

Europe Precision Medicine Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Europe Precision Medicine Market |

| Market Size 2025 | USD 158.4 Billion |

| Market Forecast 2035 | USD 346.7 Billion |

| Growth Rate | CAGR of 8.1% |

| Report Pages | 220 |

| Key Companies Covered |

Illumina, Inc., GE Healthcare, Abbott, Danaher (Cepheid), Exact Sciences, QIAGEN, IBM, Genentech, Biogen, Genelex, and Others |

| Segments Covered | By Technology, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

How is the Market Segmentation Done in European Precision Medicine?

The Europe Precision Medicine market is segmented by technology, application, end-user, and region.

Based on the Technology Segment, Gene sequencing emerges as the most dominant subsegment, holding approximately 28% market share, primarily because it provides foundational genomic insights essential for identifying mutations and tailoring treatments, driving market growth by enabling precise diagnostics and personalized therapies across diseases. Big data analytics follows as the second dominant, with around 20% share, valued for its ability to process vast datasets for pattern recognition and predictive modeling, contributing to market expansion through improved clinical decision-making and research efficiency.

Based on the Application Segment, Oncology stands out as the most dominant subsegment, capturing about 35% of the market, due to the high cancer burden and success of targeted therapies like immunotherapies, which help drive the market by enhancing survival rates and reducing side effects. Neurology ranks second with roughly 18% share, driven by advancements in genetic markers for conditions like Alzheimer’s, propelling market growth through better disease management and preventive strategies.

Based on the End-User Segment, Hospitals are the most dominant subsegment, accounting for 41% share, attributed to their central role in delivering integrated care with access to advanced diagnostics, enhancing market drive by facilitating real-time application of precision medicine. Diagnostic centers follow with 28% share, fueled by specialized testing capabilities, which advance the market through accurate biomarker identification and support for therapeutic decisions.

What are the Recent Developments in Europe Precision Medicine?

- In October 2025, Illumina, Inc. launched a new high-throughput sequencing platform optimized for clinical use, reducing costs by 30% and improving turnaround times for genomic testing in European hospitals.

- In December 2025, QIAGEN partnered with the UK NHS to expand companion diagnostic testing for rare diseases, integrating AI-driven analysis to enhance precision in treatment selection.

- In January 2026, Abbott acquired a European biotech startup specializing in CRISPR-based therapies, aiming to accelerate the development of gene-editing solutions for oncology.

- In February 2026, GE Healthcare introduced an AI-enhanced imaging system for precision diagnostics, receiving CE marking for use in cardiology applications across Europe.

- In March 2026, Biogen collaborated with German research institutes to advance pharmacogenomic studies for neurological disorders, funding a EUR 50 million initiative.

What is the Regional Analysis of Europe Precision Medicine?

- Germany is to dominate the global market.

Germany leads the Europe Precision Medicine market with a 27% share, driven by advanced pharmaceutical research infrastructure and comprehensive genomic programs, dominating through major academic centers and strong precision oncology adoption, with cities like Berlin and Munich hosting key initiatives.

The United Kingdom holds a 22% share, propelled by NHS genomic medicine service expansion and population genomics initiatives, with England leading via integrated research networks in London and Cambridge.

France accounts for 20% of the market, supported by national cancer genomics programs and precision medicine plans, with Paris and Lyon as key hubs for implementation.

Switzerland represents 15% share, fueled by a robust biotech ecosystem and international collaborations, with Basel and Zurich dominating through pharmaceutical innovations.

The rest of Europe comprises 16% of the market, with countries like Italy and Spain showing growth through emerging genomic initiatives and healthcare investments, led by Milan and Barcelona in specialized applications.

Who are the Key Market Players in Europe Precision Medicine?

- Illumina, Inc. Illumina focuses on genomic sequencing platform leadership, expanding into clinical markets through innovations in high-throughput technologies and partnerships for data interpretation.

- GE Healthcare. GE Healthcare employs strategies centered on AI-enhanced diagnostic imaging, integrating precision tools for oncology and cardiology to support clinical decision-making.

- Abbott. Abbott leverages acquisitions and companion diagnostics development, targeting molecular testing for infectious diseases and chronic conditions.

- Danaher (Cepheid). Danaher emphasizes specialized diagnostic platforms, focusing on rapid molecular testing for precision applications in hospitals.

- Exact Sciences. Exact Sciences pursues cancer screening innovations, expanding biomarker-based tests for early detection and monitoring.

- QIAGEN. QIAGEN invests in sample-to-insight solutions, developing assays for companion diagnostics in oncology.

- IBM. IBM concentrates on AI and data analytics, providing Watson Health platforms for genomic interpretation and predictive modeling.

- Genentech. Genentech focuses on targeted biologics, advancing personalized therapies through biomarker-guided development.

- Biogen. Biogen targets neurological disorders, implementing pharmacogenomic strategies for treatment optimization.

- Genelex. Genelex specializes in pharmacogenetic testing, offering solutions for drug response prediction and dosing.

What are the Market Trends in Europe’s Precision Medicine?

- Accelerated integration of precision oncology in clinical practice.

- Artificial intelligence for polygenic risk score development.

- Emphasis on predictive analytics and disease prevention.

- Expansion of specialized applications in preventive healthcare.

- Collaborations between pharma and diagnostic companies.

- Focus on population health and value-based care.

- Integration with hospital programs and pharma operations.

- Clinical validation and regulatory frameworks.

- Ethical frameworks for genetic data protection.

- Development of reimbursement pathways for tests.

What Market Segments and their Subsegments are Covered in the Europe Precision Medicine Report?

By Technology

- Gene Sequencing

- Big Data Analytics

- Drug Discovery

- Companion Diagnostics

- Bioinformatics

- CRISPR

- Artificial Intelligence

- Molecular Diagnostics

- Pharmacogenomics

- Next-Generation Sequencing

- Others

By Application

- Oncology

- Neurology

- Cardiology

- Infectious Diseases

- Immunology

- Rare Diseases

- Respiratory

- Endocrinology

- Gastroenterology

- Hematology

- Others

By End-User

- Hospitals

- Diagnostic Centers

- Research & Academic Institutes

- Pharmaceutical Companies

- Biotechnology Companies

- Healthcare Providers

- Clinical Laboratories

- Government Organizations

- Insurance Providers

- Contract Research Organizations

- Others

By Region

- Germany

- United Kingdom

- France

- Switzerland

- Italy

- Spain

- Rest of Europe

Chapter 1. Preface

Chapter 2. Executive Summary

Chapter 3. Global Europe Precision Medicine Market - Industry Analysis

Chapter 4. Global Europe Precision Medicine Market- Competitive Landscape

Chapter 5. Global Europe Precision Medicine Market - Technology Analysis

Chapter 6. Global Europe Precision Medicine Market - Application Analysis

Chapter 7. Global Europe Precision Medicine Market - End-User Analysis

Chapter 8. Europe Precision Medicine Market - Regional Analysis

Chapter 9. Company Profiles

Frequently Asked Questions

Europe precision medicine is a healthcare approach that tailors treatments based on individual genetic, environmental, and lifestyle factors to optimize outcomes and minimize side effects.

Key factors include declining sequencing costs, AI advancements, government initiatives, and increasing adoption of targeted therapies.

The market is projected to grow from approximately USD 171.2 billion in 2026 to USD 346.7 billion by 2035.

The CAGR is expected to be 8.1% during the forecast period.

Germany will contribute notably, holding around 27% of the market value due to advanced infrastructure and programs.

Major players include Illumina, Inc., GE Healthcare, Abbott, Danaher (Cepheid), Exact Sciences, QIAGEN, IBM, Genentech, Biogen, and Genelex.

The report provides comprehensive analysis including market size, forecasts, segmentation, dynamics, regional insights, key players, trends, and FAQs.

The value chain includes discovery, clinical implementation, therapeutic monitoring, genomic data integration, and treatment decision support.

Trends are shifting towards AI integration and preventive strategies, with consumers preferring personalized, data-driven treatments for better outcomes.

Regulatory factors include complex approval requirements and reimbursement policies, while ethical concerns involve data privacy and genetic discrimination.