Counter UAV Market Size, Share and Trends 2026 to 2035

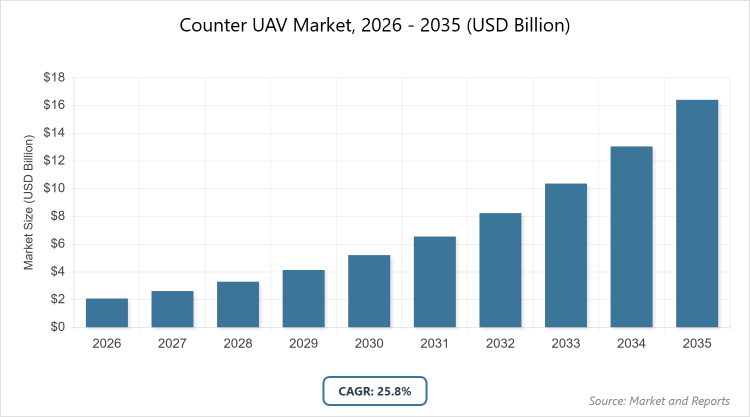

According to MarketnReports, the global Counter UAV Market size was estimated at USD 2.08 Billion in 2025 and is expected to reach USD 19.06 Billion by 2035, growing at a CAGR of 25.8% from 2026 to 2035. Counter UAV Market is driven by escalating drone-related security threats and rising adoption across defense and homeland security sectors.

What is the Counter UAV Market?

The Counter UAV Market encompasses technologies and systems designed to detect, track, identify, and neutralize unauthorized unmanned aerial vehicles (UAVs) or drones. This market addresses the growing threats posed by drones in various sectors, including military operations, critical infrastructure protection, and public safety. Market definition includes hardware such as radars and sensors, software for threat analysis, and integrated platforms that provide comprehensive countermeasures against drone incursions. The industry focuses on mitigating risks from recreational, commercial, and hostile drones through advanced detection and interdiction methods.

Key Insights

- The global Counter UAV Market was valued at USD 2.08 Billion in 2025 and is projected to reach USD 19.06 Billion by 2035.

- The market is expected to grow at a CAGR of 25.8% from 2026 to 2035.

- The market is driven by the increasing proliferation of drones for malicious purposes and heightened security concerns in defense and civilian applications.

- In the technology segment, radar based holds the dominant share of 28% due to its superior long-range detection capabilities and effectiveness in diverse environmental conditions.

- In the application segment, military & defense dominates with 55% share owing to the critical need for protecting military assets and operations from drone-based threats.

- In the end-user segment, military forces lead with 50% share because of substantial investments in advanced defense technologies to counter evolving aerial threats.

- North America dominates the regional market with a 40% share, attributed to high defense expenditures, technological advancements, and stringent security regulations in the United States.

Market Dynamics

Growth Drivers

The Counter UAV Market is propelled by the rapid increase in drone usage across various domains, leading to heightened security risks such as espionage, terrorism, and unauthorized surveillance. Governments worldwide are investing heavily in defense modernization programs, incorporating advanced C-UAV systems to safeguard national borders and critical assets. Technological advancements in sensors, AI, and directed energy weapons enhance detection accuracy and response times, further driving adoption. Additionally, the rise in commercial drone applications, like delivery services, necessitates robust countermeasures to prevent airspace violations and ensure public safety.

Restraints

High development and deployment costs of sophisticated C-UAV systems pose a significant barrier, particularly for smaller organizations and developing nations with limited budgets. Regulatory challenges, including restrictions on jamming technologies and spectrum usage, can hinder market expansion. Moreover, the potential for false positives in detection systems may lead to operational inefficiencies and unnecessary alerts, deterring widespread adoption. Integration complexities with existing security infrastructures also add to the restraints, requiring substantial technical expertise and resources.

Opportunities

Emerging markets in Asia-Pacific and the Middle East present lucrative opportunities due to increasing defense budgets and infrastructure development. The integration of AI and machine learning for predictive threat analysis opens new avenues for innovation in autonomous C-UAV systems. Expanding applications in civilian sectors, such as event security and airport protection, broaden the market scope. Partnerships between technology firms and governments can accelerate the development of cost-effective, scalable solutions to address evolving drone threats.

Challenges

The continuous evolution of drone technologies, including stealth features and swarm capabilities, challenges existing C-UAV systems to keep pace. Ensuring interoperability among multi-vendor components in integrated defense networks remains a technical hurdle. Environmental factors, such as urban clutter and weather conditions, can impair system performance, leading to reliability issues. Additionally, ethical and legal concerns regarding the neutralization of drones, especially in civilian airspace, complicate deployment strategies.

Counter UAV Market Report Scope

| Report Attributes | Report Details |

| Report Name | Counter UAV Market |

| Market Size 2025 | USD 2.08 Billion |

| Market Forecast 2035 | USD 19.06 Billion |

| Growth Rate | CAGR of 25.8% |

| Report Pages | 220 |

| Key Companies Covered | Lockheed Martin, Raytheon Technologies, Thales Group, Boeing, Northrop Grumman, DroneShield, and Others |

| Segments Covered | By Technology, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

Market Segmentation

The Counter UAV Market is segmented by technology, application, end-user, and region. All the segments have been analyzed based on present and future trends and the market is estimated from 2026 to 2035.

Based on Technology Segment, The most dominant subsegment is radar based, holding a significant market share due to its ability to provide long-range, all-weather detection of drones, which is crucial for early threat identification. The second most dominant is radio frequency (RF) based, valued for its cost-effectiveness and capability to detect drone communications signals. Radar based drives the market by enabling reliable surveillance in challenging environments, enhancing overall security postures, while RF based contributes by offering passive detection that minimizes interference and supports layered defense strategies.

Based on Application Segment, Military & defense emerges as the most dominant, driven by the imperative to protect troops and installations from drone reconnaissance and attacks. Homeland security ranks as the second dominant, focusing on safeguarding public spaces and borders. Military & defense propels market growth through substantial funding for advanced systems that integrate seamlessly with existing military operations, whereas homeland security aids expansion by addressing urban threats and ensuring compliance with national security protocols.

Based on End-User Segment, Military forces dominate this segment, owing to their extensive requirements for combat-ready C-UAV solutions in active zones. Government agencies follow as the second dominant, utilizing these systems for protecting official sites and events. Military forces drive the market by demanding high-performance, rugged technologies that evolve with warfare tactics, while government agencies contribute by implementing preventive measures that enhance civilian safety and infrastructure resilience.

Recent Developments

- In October 2025, AeroVironment, Inc. was awarded a USD 95.9 million contract by the US Army to deliver the Next-Generation C-UAS Missile (NGCM) for the Long-Range Kinetic Interceptor program, including the Freedom Eagle interceptor.

- In February 2025, Lockheed Martin unveiled a scalable Counter-Unmanned Aerial System solution featuring modular, open-architecture layered detection and mitigation using AI-enabled software.

- In December 2025, Lockheed Martin collaborated with Microsoft to develop the “Sanctum” Counter-UAS platform, integrating cloud-based AI analytics and multi-sensor tracking for enhanced real-time threat response.

- In July 2025, RTX Corporation partnered with Shield AI to integrate autonomous software into its Multi-Spectral Targeting System, improving drone threat mitigation.

- In June 2025, Blighter Surveillance Systems launched the B422LR radar, offering low-power, long-range detection for border surveillance.

Regional Analysis

North America to dominate the global market.

North America leads the Counter UAV Market, primarily driven by the United States, which dominates due to its massive defense budget and leadership in technological innovation. The region's focus on countering asymmetric threats, coupled with collaborations between government and private sectors, fosters rapid adoption of advanced systems.

Europe holds a significant share, with France and the United Kingdom as dominating countries, emphasizing integrated defense strategies against drone incursions in urban and military settings. Investments in R&D and multinational partnerships enhance the region's capabilities.

Asia-Pacific is the fastest-growing region, led by China and India, where increasing geopolitical tensions and border security needs drive demand. Rapid industrialization and government initiatives for smart city protection further accelerate market expansion.

Latin America shows emerging potential, with Brazil dominating through efforts to secure vast borders and critical infrastructure against illicit drone activities. Regional collaborations and foreign investments support growth.

The Middle East and Africa are witnessing growth, dominated by Saudi Arabia and the UAE, focusing on protecting oil facilities and urban areas from drone threats amid regional conflicts.

Key Market Players and Strategies

Lockheed Martin. Lockheed Martin employs strategies focused on innovation through AI integration and scalable solutions, such as unveiling modular C-UAS systems and collaborating with tech giants like Microsoft for cloud-based platforms to enhance threat detection and response.

Raytheon Technologies (RTX). RTX emphasizes partnerships and demonstrations, including collaborations with Shield AI for autonomous software integration and showcasing radar and interceptor systems to validate performance against complex threats.

Thales Group. Thales pursues product launches and alliances, such as delivering advanced systems to navies and integrating with partners for comprehensive mine countermeasures, extending to C-UAV applications.

Boeing. Boeing focuses on defense contracts and technological advancements, leveraging its aerospace expertise to develop integrated C-UAV solutions for military and homeland security.

Northrop Grumman. Northrop Grumman adopts strategies centered on funding and innovation in counter-drone platforms, positioning itself as a frontrunner in integrated defense networks.

DroneShield. DroneShield prioritizes specialized solutions and expansions, securing funding for AI-powered detection and forming alliances to enhance global deployment of RF-based systems.

Market Trends

- Integration of artificial intelligence and machine learning for enhanced threat prediction and automated responses.

- Adoption of multi-sensor fusion technologies to improve detection accuracy in complex environments.

- Rise in directed energy weapons, such as lasers, for precise and cost-effective neutralization.

- Development of portable and mobile C-UAV systems for rapid deployment in dynamic scenarios.

- Increasing regulatory frameworks and standards for drone management to support market growth.

- Focus on counter-swarm capabilities to address emerging threats from multiple drones.

- Expansion of UAV-based counter systems for aerial interdiction.

Market Segments and their subsegment Covered in the Report

- By Technology

-

- Radar Based

- Radio Frequency (RF) Based

- Electro-Optical (EO) Based

- Infrared (IR) Based

- Acoustic Based

- Laser Based

- Kinetic Based

- RF Jamming Based

- GNSS Jamming Based

- Combined Sensors

- Others

- By Application

- Military & Defense

- Commercial

- Homeland Security

- Critical Infrastructure

- Airports

- Prisons

- Events

- Borders

- Government Buildings

- Power Utilities

- Others

- By End-User

- Military Forces

- Government Agencies

- Law Enforcement

- Commercial Entities

- Energy Sector

- Transportation Hubs

- Event Organizers

- Correctional Facilities

- Border Control

- Critical Infrastructure Operators

- Others

- By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

The Counter UAV Market involves systems and technologies aimed at detecting, tracking, and neutralizing unauthorized drones to ensure security across various sectors.

Key factors include rising drone threats, technological advancements in AI and sensors, increasing defense budgets, and regulatory support for airspace security.

The market was valued at USD 2.08 Billion in 2025 and is projected to reach USD 19.06 Billion by 2035.

The CAGR is expected to be 25.8% during 2026-2035.

North America will contribute notably, holding around 40% of the market share due to advanced infrastructure and high investments.

Major players include Lockheed Martin, Raytheon Technologies, Thales Group, Boeing, Northrop Grumman, and DroneShield.

The report provides comprehensive insights into market size, trends, segments, key players, regional analysis, and forecasts.

Stages include research and development, component manufacturing, system integration, deployment, and maintenance services.

Trends are shifting towards AI-driven autonomous systems, while preferences favor integrated, multi-layered solutions for enhanced reliability and efficiency.

Regulations on spectrum usage and drone operations, along with environmental considerations for energy-efficient systems, influence market dynamics and adoption.