AI Compute Market Size, Share and Trends 2026 to 2035

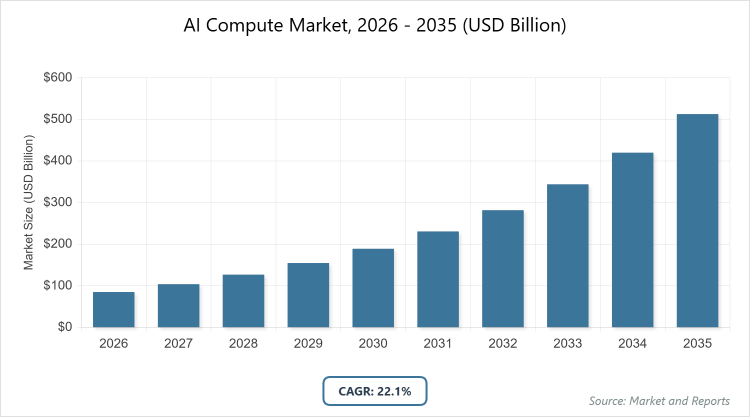

According to MarketnReports, the global AI Compute market size was estimated at USD 85 billion in 2025 and is expected to reach USD 620 billion by 2035, growing at a CAGR of 22.1% from 2026 to 2035. AI Compute Market is driven by explosive growth in large language models, generative AI, and the race for exascale AI training infrastructure.

What are the Key Insights into AI Compute?

- The global AI Compute market was valued at USD 85 billion in 2025 and is projected to reach USD 620 billion by 2035.

- The market is expected to grow at a CAGR of 22.1% during the forecast period from 2026 to 2035.

- The market is driven by rapid scaling of foundation models, generative AI adoption across enterprises, sovereign AI initiatives, and the shift toward inference-heavy workloads.

- In the type segment, GPU dominates with a 68% share due to NVIDIA’s near-monopoly in AI training and the proven performance of H100/H200 series in large-scale clusters.

- In the application segment, training dominates with a 58% share as frontier model development continues to require unprecedented FLOPs and massive GPU clusters.

- In the end-user segment, cloud service providers dominate with a 52% share owing to their role in hosting hyperscale AI clusters and providing AI compute as a service to enterprises.

- North America dominates the regional market with a 58% share, driven by NVIDIA’s headquarters, concentration of hyperscalers (AWS, Azure, Google Cloud), and massive capital investment in AI infrastructure.

What is the Industry Overview of AI Compute?

The AI Compute market encompasses specialized hardware, software, and infrastructure designed to perform the massive parallel computations required for training, fine-tuning, inference, and deployment of artificial intelligence and machine learning models at scale. Market definition includes high-performance GPUs, TPUs, custom AI accelerators, AI-optimized servers, hyperscale clusters, and supporting software stacks that power everything from cloud-based foundation model training to edge inference, addressing the exponential increase in computational demands driven by larger model sizes, more complex architectures, and expanding AI applications across industries while facing challenges in power consumption, cooling, supply constraints, and energy efficiency.

What are the Market Dynamics of AI Compute?

Growth Drivers

The AI Compute market experiences explosive growth from the relentless scaling of foundation models, where parameter counts have grown from billions to trillions, requiring exponentially more compute for training and fine-tuning. Generative AI adoption across enterprises for content creation, code generation, customer service, and drug discovery drives massive demand for both training and inference capacity. Sovereign AI initiatives by governments (India, UAE, Saudi Arabia, France, Japan) push domestic AI compute infrastructure to reduce reliance on foreign clouds. The shift toward inference-heavy workloads (serving trained models to millions of users) creates sustained demand for efficient inference hardware. Strategic investments by hyperscalers, chip vendors, and energy companies in next-generation AI data centers further accelerate ecosystem development.

Restraints

Extreme power consumption of large AI clusters (hundreds of megawatts per site) creates grid connection delays, permitting issues, and high electricity costs, limiting new data center build-out. Global semiconductor supply constraints, particularly for advanced nodes (3nm/2nm) and high-bandwidth memory (HBM), cause allocation battles and extended lead times. Astronomical capital expenditure (billions per cluster) restricts participation to only the largest hyperscalers and tech giants. Cooling requirements for dense GPU racks demand advanced liquid cooling, increasing complexity and cost. Geopolitical tensions and export controls on advanced chips (e.g., U.S. restrictions on China) fragment the global market and slow technology diffusion.

Opportunities

Opportunities emerge in inference-optimized hardware and software that deliver dramatically better performance-per-dollar and performance-per-watt for serving models, shifting the market from training-dominant to inference-dominant. Sovereign AI data center projects in multiple countries create new large-scale procurement opportunities. Growth of AI startups building specialized models creates demand for flexible, multi-tenant AI compute platforms. Energy sector partnerships (nuclear, geothermal, renewables) to co-locate AI data centers with power generation address energy bottlenecks. Edge AI compute for real-time applications in automotive, manufacturing, and smart cities opens massive distributed compute markets.

Challenges

Challenges include achieving meaningful energy efficiency improvements as model sizes and cluster scales continue to grow exponentially. Ensuring reliable supply of scarce components (CoWoS packaging, HBM3E/HBM4 memory) amid intense competition among hyperscalers. Managing thermal design power and cooling at exascale densities without prohibitive infrastructure costs. Addressing talent shortages in AI systems engineering, liquid cooling, and power distribution. Navigating increasingly stringent export controls and national security reviews for advanced AI hardware. Maintaining model performance when using multi-vendor heterogeneous clusters.

AI Compute Market: Report Scope

| Report Attributes | Report Details |

| Report Name | AI Compute Market |

| Market Size 2025 | USD 85 Billion |

| Market Forecast 2035 | USD 620 Billion |

| Growth Rate | CAGR of 22.1% |

| Report Pages | 220 |

| Key Companies Covered | NVIDIA Corporation, Advanced Micro Devices, Inc., Intel Corporation, Google LLC, Amazon Web Services, Microsoft Corporation, Huawei Technologies Co., Ltd., Cerebras Systems, and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of AI Compute?

The AI Compute market is segmented by type, application, end-user, and region.

By Type. GPU is the most dominant subsegment, holding approximately 68% market share, due to NVIDIA’s dominance in AI training with H100/H200 and upcoming Blackwell architecture, offering unmatched performance for large-scale parallel workloads. This dominance drives the market by serving as the de facto standard for frontier model training. ASIC ranks as the second most dominant, with around 15% share, led by Google TPU and emerging custom silicon from hyperscalers, propelling growth through superior efficiency for specific workloads.

By Application. Training emerges as the most dominant subsegment, capturing about 58% share, primarily because frontier model development still requires unprecedented computational scale and remains the most compute-intensive phase. This leads to market growth by driving demand for the largest clusters. Inference follows as the second most dominant, with roughly 32% share and the fastest growth rate, driven by massive serving of trained models to billions of users, driving the market via sustained revenue from cloud inference.

By End-User. Cloud service providers represent the most dominant subsegment at about 52% share, driven by their role in building and operating hyperscale AI clusters and offering AI compute as a service. This dominance accelerates market expansion through massive capex cycles and influence on standards. Enterprises rank second most dominant, holding around 28% share, adopting on-premise and hybrid AI compute for data sovereignty and latency-critical applications.

What are the Recent Developments in AI Compute?

- In January 2026, NVIDIA announced the Blackwell B200 GPU delivering up to 30× faster inference performance than H100 for large language models.

- In December 2025, xAI revealed plans for the Memphis Supercluster with 100,000 H100 GPUs, positioning it as one of the world’s largest AI training clusters.

- In November 2025, Google deployed TPU v5p pods with liquid cooling, achieving 2× performance per watt compared to previous generations.

- In October 2025, Microsoft announced a new generation of Maia AI accelerators optimized for Azure inference workloads.

- In September 2025, AMD launched the Instinct MI325X accelerator with HBM3E memory, targeting both training and inference.

What is the Regional Analysis of AI Compute?

- North America is expected to dominate the global market.

North America holds the largest share at approximately 58%, with the United States as the dominating country, driven by concentration of hyperscalers (AWS, Azure, Google Cloud), leading AI chip vendors (NVIDIA, AMD, Intel), and massive private capital flowing into AI infrastructure. This region’s leadership is underpinned by Silicon Valley’s innovation ecosystem, top-tier research universities, and defense-related AI compute investments. The U.S. hosts the majority of the world’s largest AI training clusters. Canada’s Montreal and Toronto AI hubs contribute meaningful research compute capacity. Government initiatives like the CHIPS Act bolster domestic semiconductor production for AI accelerators. Venture funding and sovereign wealth investments continue to fuel hyperscale expansion.

Europe shows strong growth but remains significantly behind North America, driven by regulatory alignment with trustworthy AI and industrial strength, where France and Germany dominate through government-backed projects (Mistral AI, Aleph Alpha, European High-Performance Computing Joint Undertaking). The region’s expansion benefits from EU sovereign AI initiatives aiming to reduce cloud dependency. The UK’s post-Brexit AI strategy focuses on national compute infrastructure. Nordic countries invest in green AI data centers powered by renewables. However, fragmented funding, slower regulatory approval for large clusters, and limited domestic GPU supply constrain scale compared to North America.

Asia Pacific exhibits the fastest absolute growth, fueled by national AI ambitions and manufacturing scale, with China leading through aggressive state-backed investments in domestic GPU alternatives and massive domestic AI clusters despite U.S. export controls. This area’s potential lies in cost-competitive infrastructure build-out, rapid 5G deployment, and huge domestic data sets. India’s National Mission on Interdisciplinary Cyber-Physical Systems funds AI compute capacity. Japan’s supercomputing heritage transitions to AI-specific clusters. South Korea’s Samsung and SK hynix invest heavily in HBM for AI accelerators. Singapore serves as a regional AI hub with strict data sovereignty rules.

Latin America shows early-stage but accelerating activity, dominated by Brazil’s AI research institutions and growing cloud adoption, though limited by energy infrastructure and capital availability. Mexico benefits from nearshoring and U.S. supply chain integration. Chile invests in green AI data centers leveraging renewable energy. However, limited domestic semiconductor capabilities and lower R&D investment slow progress. Emerging sovereign AI discussions in several countries aim to build regional compute capacity.

The Middle East and Africa represent high-growth emerging markets, with the United Arab Emirates and Saudi Arabia leading through massive sovereign investments in AI infrastructure (G42 in UAE, Vision 2030 in Saudi Arabia). This region’s potential lies in oil-funded capital deployment, strategic partnerships with U.S. and Chinese vendors, and ambition to become AI hubs. South Africa’s growing data center market supports regional compute capacity. However, limited local semiconductor ecosystem and energy availability in many African countries constrain scale. Technology transfer agreements and sovereign AI strategies are accelerating adoption.

What are the Key Market Players in AI Compute?

- NVIDIA Corporation. NVIDIA maintains dominance through its CUDA ecosystem and H100/H200/Blackwell GPU lineup, focusing on full-stack AI factories and partnerships with every major hyperscaler.

- Advanced Micro Devices, Inc. (AMD). AMD aggressively challenges NVIDIA with Instinct MI300 series accelerators, emphasizing open-source ROCm software and better memory bandwidth.

- Intel Corporation. Intel leverages Gaudi accelerators and Xeon processors, focusing on open ecosystem (oneAPI) and cost-competitive inference solutions.

- Google LLC. Google drives innovation with TPU v5p and Trillium chips, optimizing for its own workloads and offering Cloud TPU as a service.

- Amazon Web Services (AWS). AWS develops custom Trainium and Inferentia chips, focusing on cost-efficient training and inference in cloud environments.

- Microsoft Corporation. Microsoft invests in Maia accelerators and partners with OpenAI, building massive AI clusters for Azure.

- Huawei Technologies Co., Ltd. Huawei pushes Ascend AI processors in China and select international markets despite export restrictions.

- Cerebras Systems. Cerebras offers wafer-scale CS-3 engines for massive single-chip training, targeting research and frontier model development.

What are the Market Trends in AI Compute?

- Rapid transition from training-focused to inference-dominant workloads.

- Emergence of custom silicon from hyperscalers and large enterprises.

- Increasing adoption of liquid cooling and advanced power delivery for dense clusters.

- Growth of sovereign AI compute initiatives globally.

- Rise of inference-optimized architectures and quantization techniques.

- Expansion of multi-vendor heterogeneous clusters.

- Focus on energy efficiency and sustainable AI infrastructure.

What Market Segments and Subsegments are Covered in the AI Compute Report?

By Type

- GPU

- CPU

- ASIC

- FPGA

- TPU

- NPU

- Cloud AI Accelerators

- Edge AI Accelerators

- On-Premise AI Servers

- Hyperscale AI Clusters

- AI Training Servers

- AI Inference Servers

- Others

By Application

- Training

- Inference

- Data Preparation

- Model Optimization

- Simulation & Modeling

- Natural Language Processing

- Computer Vision

- Recommendation Systems

- Autonomous Systems

- Generative AI

- Others

By End-User

- Cloud Service Providers

- Enterprises

- Research Institutes

- Government & Defense

- Automotive

- Healthcare & Life Sciences

- Financial Services

- Retail & E-commerce

- Manufacturing

- Media & Entertainment

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

AI Compute refers to specialized hardware, infrastructure, and software optimized for the massive parallel computations required to train, fine-tune, and run artificial intelligence models at scale.

Key factors include foundation model scaling, generative AI adoption, sovereign AI initiatives, inference workload growth, and energy-efficient hardware advancements.

The market is projected to grow from USD 85 billion in 2025 to USD 620 billion by 2035.

The CAGR is expected to be 22.1%.

North America will contribute notably, holding around 58% share due to hyperscaler dominance and chip innovation.

Major players include NVIDIA Corporation, Advanced Micro Devices, Intel Corporation, Google LLC, Amazon Web Services, Microsoft Corporation, Huawei Technologies, and Cerebras Systems.

The report provides comprehensive analysis of market size, trends, segmentation, regional outlook, competitive landscape, and forecasts.

Stages include semiconductor design & fabrication, system integration, data center construction, cluster deployment, model training & inference, and ongoing optimization.

Trends shift toward inference optimization, custom silicon, and sustainable infrastructure, with preferences for performance-per-watt and cost-per-token efficiency.

Export controls on advanced chips, energy consumption regulations, and environmental sustainability mandates for data centers influence supply, design, and location choices.