Flow Battery Market Size, Share and Trends 2026 to 2035

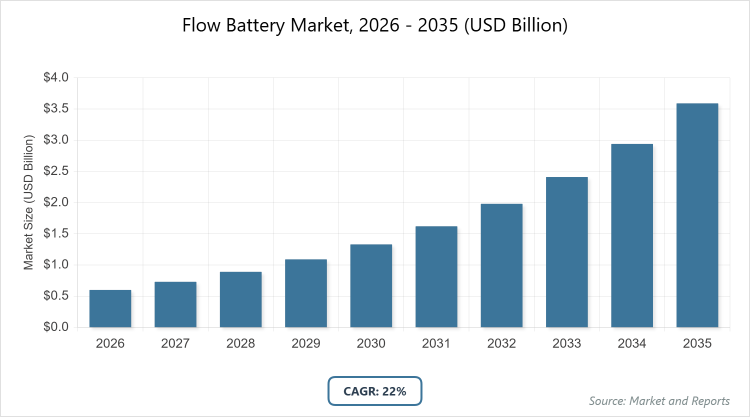

According to MarketnReports, the global Flow Battery Market size was estimated at USD 0.6 Billion in 2025 and is expected to reach USD 4.5 Billion by 2035, growing at a CAGR of 22% from 2026 to 2035. Flow Battery Market is driven by increasing adoption of renewable energy sources requiring efficient long-duration storage solutions.

What is the Industry Overview of Flow Battery Market?

The flow battery market encompasses advanced energy storage systems that utilize electrochemical reactions in liquid electrolytes to store and release energy, offering scalable, long-duration capabilities ideal for grid stability and renewable integration. Market definition refers to rechargeable batteries where energy is stored in chemical solutions contained in external tanks, separated by a membrane, allowing independent scaling of power and energy capacity for applications like utility-scale storage and microgrids.

What are the Key Insights into Flow Battery Market?

- Market size valued at USD 0.6 Billion in 2025 and projected to reach USD 4.5 Billion by 2035.

- Expected to grow at a CAGR of 22% during the forecast period 2026-2035.

- Market is driven by rising demand for renewable energy integration and grid resilience.

- Vanadium redox dominates the battery type segment with 80% share due to its proven long cycle life and ability to operate in full discharge cycles without degradation.

- Utilities dominate the application segment with 50% share as flow batteries provide reliable long-duration storage for large-scale grid applications, enabling efficient peak shaving and frequency regulation.

- Asia Pacific dominates the regional segment with 48% share owing to rapid renewable energy expansion in countries like China and supportive government policies for energy storage.

What are the Market Dynamics in Flow Battery Market?

Growth Drivers

The growth drivers in the flow battery market are propelled by the escalating global shift toward renewable energy sources, such as solar and wind, which necessitate reliable long-duration storage to manage intermittency and ensure grid stability. Technological advancements in electrolyte chemistry and membrane design have enhanced efficiency and reduced costs, making flow batteries more competitive against lithium-ion alternatives for utility-scale applications. Government incentives, including subsidies and mandates for clean energy storage, further accelerate adoption, particularly in regions pursuing net-zero emissions goals.

Restraints

Restraints in the flow battery market include high upfront capital costs associated with materials like vanadium and system installation, which can deter widespread deployment compared to more established battery technologies. Supply chain vulnerabilities for key raw materials, such as vanadium, subject to price volatility and geopolitical risks, pose challenges to scalability. Additionally, lower energy density relative to lithium-ion batteries limits their suitability for space-constrained applications, slowing penetration in certain sectors.

Opportunities

Opportunities in the flow battery market arise from the growing demand for long-duration energy storage (LDES) in emerging applications like data centers and EV charging infrastructure, where safety and scalability are paramount. Innovations in non-vanadium chemistries, such as zinc-bromine and organic-based systems, offer cost reductions and environmental benefits, opening new markets. Expanding microgrid deployments in remote and disaster-prone areas, coupled with favorable policies for grid modernization, present avenues for market expansion.

Challenges

Challenges in the flow battery market stem from technical hurdles like electrolyte degradation over time and the need for improved power density to compete in high-performance scenarios. Regulatory inconsistencies across regions can hinder standardized adoption and investment. Moreover, competition from advancing lithium-ion and solid-state batteries, which offer higher efficiency in short-duration uses, requires flow battery manufacturers to continually innovate to maintain relevance.

Flow Battery Market Report Scope

| Report Attributes | Report Details |

| Report Name | Flow Battery Market |

| Market Size 2025 | USD 0.6 Billion |

| Market Forecast 2035 | USD 4.5 Billion |

| Growth Rate | CAGR of 22% |

| Report Pages | 220 |

| Key Companies Covered | ESS Inc., Invinity Energy Systems, Sumitomo Electric Industries, Redflow Limited, Primus Power, VRB Energy, and Others |

| Segments Covered | By Battery Type, By Application, By End-User, By Material, By Storage, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 - 2024 |

| Forecast Year | 2026 - 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Flow Battery Market?

The Flow Battery Market is segmented by battery type, application, end-user, material, storage, and region. All the segments have been analyzed based on present and future trends and the market is estimated from 2026 to 2035.

Based on Battery Type Segment, Vanadium redox emerges as the most dominant subsegment, holding approximately 80% market share, due to its superior cycle life exceeding 20,000 cycles and ability to fully discharge without damage, which drives market growth by enabling cost-effective, long-term energy storage for grid applications. Zinc-bromine ranks as the second most dominant, with around 12% share, owing to its lower material costs and non-flammable properties, contributing to market expansion through safer deployments in commercial and industrial settings.

Based on Application Segment, Utilities stand out as the most dominant subsegment, capturing about 50% market share, attributed to their need for large-scale, long-duration storage to integrate renewables and stabilize grids, thereby propelling overall market growth via enhanced energy reliability. Renewable integration is the second most dominant, with roughly 20% share, as it addresses intermittency issues in solar and wind projects, fostering market advancement by supporting global decarbonization efforts.

Based on End-User Segment, Utilities dominate as the primary subsegment with around 45% market share, driven by their requirement for scalable storage to manage peak loads and ensure grid resilience, which accelerates market growth through widespread adoption in energy infrastructure. Commercial & industrial follows as the second dominant, holding about 25% share, due to its focus on backup power and cost savings from energy shifting, boosting the market by enabling efficient operations in high-demand sectors.

Based on Material Segment, Vanadium leads as the most dominant subsegment with over 70% market share, thanks to its electrochemical stability and recyclability, which drive market growth by offering durable, low-maintenance solutions for extensive cycling in storage systems. Zinc bromine is the second most dominant, with approximately 15% share, valued for its abundance and lower cost, aiding market progression by providing accessible alternatives for safer, large-scale applications.

Based on Storage Segment, Large-scale dominates with about 75% market share, propelled by its suitability for utility and grid-level deployments requiring extended duration, thus driving market growth through support for massive renewable energy projects. Compact is the second most dominant, with around 20% share, as it caters to space-limited commercial uses, contributing to market expansion by enabling flexible installations in urban environments.

What are the Recent Developments in Flow Battery Market?

- In August 2024, scientists at the Dalian Institute of Chemical Physics developed novel naphthalene-based organic redox-active molecules for aqueous organic flow batteries, enhancing efficiency and sustainability for long-duration storage.

- In April 2024, the U.S. Department of Energy’s Office of Electricity awarded USD 15 million to advance zinc, lead, and flow battery technologies, focusing on long-duration energy storage innovations.

- In May 2023, Pacific Northwest National Laboratory and Invinity introduced a 24-hour vanadium flow battery project with a 525kW power rating, aimed at demonstrating extended discharge capabilities for grid applications.

- In January 2026, ERCOT began settling six-hour ramping products, with Dalian Rongke Power bidding a 300 MWh vanadium system into the first auction to support grid flexibility.

- In August 2025, Dalian Rongke commissioned a 100 MW/400 MWh project in Changzhou using electrolyte leasing, reducing capital costs by 35-40% for large-scale implementations.

What is the Regional Analysis of Flow Battery Market?

Asia Pacific to dominate the global market.

Asia Pacific leads the flow battery market, driven by rapid renewable energy adoption and government-backed initiatives in China, where major projects like Dalian Rongke's large-scale installations dominate, supported by policies for grid modernization and energy security.

North America follows closely, with the U.S. spearheading growth through federal incentives like the Department of Energy awards and deployments in California for wildfire resilience, emphasizing long-duration storage in utilities and data centers.

Europe experiences steady expansion, led by Germany's focus on energy transition via projects like TenneT's black-start trials, bolstered by EU regulations promoting sustainable storage solutions in industrial and renewable sectors.

Latin America shows emerging potential, with Brazil advancing through microgrid applications in remote areas, aided by investments in renewable integration to address energy access challenges.

The Middle East and Africa are nascent but growing, with South Africa leading via off-grid power solutions for mining and telecom, driven by efforts to enhance energy reliability amid infrastructure constraints.

Who are the Key Market Players in Flow Battery Market?

ESS Inc. ESS Inc. focuses on iron-flow battery technology, emphasizing long-duration storage for utilities and renewables through strategic partnerships like the one with Pacific Northwest National Laboratory, while expanding manufacturing capacity to meet growing demand in North America.

Invinity Energy Systems. Invinity Energy Systems prioritizes vanadium flow batteries, pursuing global project deployments and collaborations such as the 24-hour battery initiative, alongside investments in modular designs to enhance scalability and reduce costs for commercial applications.

Sumitomo Electric Industries. Sumitomo Electric Industries leverages its expertise in redox flow systems, implementing large-scale grid projects in Japan and internationally, with strategies centered on R&D for improved electrolyte efficiency and alliances to penetrate emerging markets.

Redflow Limited. Redflow Limited specializes in zinc-bromine batteries, adopting a strategy of targeting off-grid and microgrid sectors through product innovations for safety and durability, while forming distribution partnerships to expand in Australia and beyond.

Primus Power. Primus Power advances zinc-bromine technology, focusing on cost-effective solutions for industrial backup via pilot projects and funding pursuits, aiming to scale production for competitive positioning in the energy storage landscape.

VRB Energy. VRB Energy emphasizes vanadium redox batteries, executing mega-scale installations in China and strategizing through technology licensing and joint ventures to accelerate adoption in Asia Pacific's renewable energy sector.

What are the Market Trends in Flow Battery Market?

- Utility-scale long-duration energy storage deployment for grid stability.

- Integration of flow batteries with renewable energy systems like solar and wind.

- Advancements in electrolyte chemistry and stack design to improve efficiency.

- Rising adoption of modular and scalable energy storage solutions.

- Growing focus on safe and non-flammable battery technologies.

- Expansion into data centers and EV charging infrastructure applications.

- Shift toward non-vanadium chemistries for cost reduction.

What are the Market Segments and their Subsegment Covered in the Report?

- By Battery Type

- Vanadium Redox

- Zinc-Bromine

- All-Iron

- Hydrogen-Bromine

- Polysulfide Bromine

- Organic

- All Vanadium

- Iron-Chromium

- Zinc-Iron

- Membrane-less

- Others

- By Application

- Utilities

- Commercial

- Industrial

- Military

- EV Charging Station

- Off Grid & Micro grid Power

- Renewable Integration

- Peak Shaving

- Backup Power

- Frequency Regulation

- Others

- By End-User

- Utilities

- Industrial

- Commercial

- Residential

- Telecom

- Data Centers

- Renewable Energy Generators

- Military

- EV Infrastructure

- Grid Operators

- Others

- By Material

- Vanadium

- Zinc Bromine

- Organic

- All-Iron

- Hydrogen Bromine

- Others

- By Storage

- Compact

- Large Scale

- Small Scale

- Others

- By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Flow battery market refers to the industry focused on rechargeable energy storage systems using liquid electrolytes for scalable, long-duration power solutions in renewables and grids.

Key factors include rising renewable energy adoption, government incentives for storage, technological advancements in chemistries, and demand for grid resilience.

The market is projected to grow from USD 0.6 Billion in 2025 to USD 4.5 Billion by 2035.

The CAGR is expected to be 22% during 2026-2035.

Asia Pacific will contribute notably, driven by China's large-scale projects and renewable policies.

Major players include ESS Inc., Invinity Energy Systems, Sumitomo Electric Industries, Redflow Limited, Primus Power, and VRB Energy.

The report offers in-depth analysis of size, trends, segments, players, regional outlook, and forecasts.

Stages include raw material sourcing, electrolyte production, system assembly, deployment, and end-of-life recycling.

Trends lean toward safer, non-flammable chemistries, while consumers prefer scalable, cost-effective solutions for long-duration storage.

Factors include incentives for clean energy, emissions regulations, and supply chain sustainability mandates for materials like vanadium.