Edge AI Market Size, Share and Trends 2026 to 2035

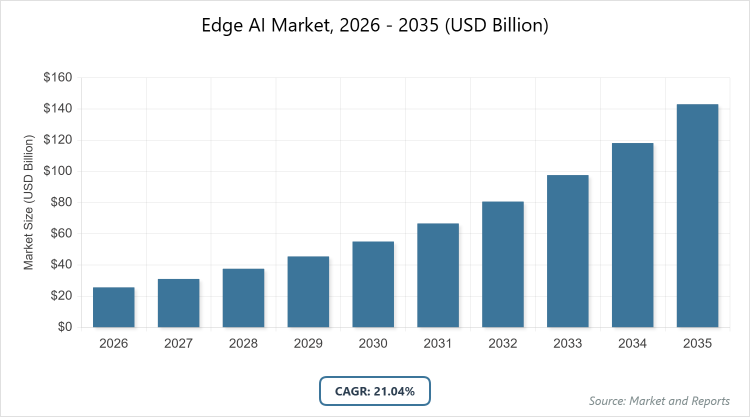

According to MarketnReports, the global Edge AI market size was estimated at USD 25.65 billion in 2025 and is expected to reach USD 143.06 billion by 2035, growing at a CAGR of 21.04% from 2026 to 2035. Edge AI Market is driven by increasing demand for real-time data processing, low-latency applications, and enhanced data privacy in IoT and 5G ecosystems.

What are the Key Insights into Edge AI?

- The global Edge AI market was valued at USD 25.65 billion in 2025 and is projected to reach USD 143.06 billion by 2035.

- The market is expected to grow at a CAGR of 21.04% during the forecast period from 2026 to 2035.

- The market is driven by explosive IoT growth, 5G rollout, the need for low-latency AI in autonomous systems, and increasing focus on data sovereignty and privacy regulations.

- In the type segment, hardware dominates with a 60% share due to the critical role of specialized AI chips and accelerators (NPU, GPU, ASIC) optimized for edge power and performance constraints.

- In the application segment, autonomous vehicles dominate with a 25% share as edge AI enables real-time perception, decision-making, and safety in self-driving systems.

- In the end-user segment, automotive & transportation dominates with a 28% share owing to massive investments in ADAS, autonomous driving, and connected vehicles requiring on-board intelligence.

- North America dominates the regional market with a 40% share, driven by the concentration of leading AI chip vendors (NVIDIA, Intel, Qualcomm), a strong R&D ecosystem, and early adoption in automotive and industrial sectors.

What is the Industry Overview of Edge AI?

The Edge AI market encompasses artificial intelligence technologies and solutions deployed directly on edge devices (sensors, cameras, smartphones, gateways, industrial equipment) rather than centralized cloud servers, enabling real-time inference, local data processing, reduced latency, and improved privacy by minimizing data transmission to remote data centers. Market definition includes hardware (AI chips, accelerators, processors), software (edge ML frameworks, inference engines), and services (development tools, deployment platforms) that support on-device AI workloads across industries requiring immediate decision-making, bandwidth efficiency, and offline capabilities in environments with limited or intermittent connectivity.

What are the Market Dynamics of Edge AI?

Growth Drivers

The Edge AI market experiences robust growth from the massive proliferation of IoT devices generating exponential data volumes that cannot be efficiently sent to the cloud due to bandwidth limitations and latency requirements. The rollout of 5G networks enables ultra-reliable low-latency communication critical for edge AI applications in autonomous vehicles, smart manufacturing, and remote healthcare. Increasing emphasis on data privacy regulations (GDPR, CCPA) and sovereignty pushes organizations to process sensitive data locally rather than transmitting it to centralized servers. Advancements in specialized edge AI hardware (NPUs, efficient GPUs) and optimized inference frameworks reduce power consumption while maintaining high performance, making on-device AI viable for battery-constrained devices. Strategic partnerships between semiconductor companies, cloud providers, and industry verticals accelerate ecosystem development.

Restraints

High development costs for custom edge AI chips and software optimized for specific power, size, and thermal constraints limit adoption among smaller organizations. Limited computational resources on edge devices restrict the complexity of AI models that can be deployed, often requiring model compression techniques that may compromise accuracy. Fragmented hardware ecosystems (different NPUs, GPUs, MCUs) create compatibility challenges and increase integration complexity for developers. Supply chain vulnerabilities for advanced semiconductors (especially during geopolitical tensions) lead to shortages and price volatility. Stringent safety and certification requirements in automotive and healthcare delay time-to-market for edge AI solutions.

Opportunities

Opportunities emerge in the convergence of edge AI with 6G, private 5G networks, and satellite connectivity for truly ubiquitous intelligence in remote and industrial settings. Expansion into smart cities and infrastructure (traffic management, predictive maintenance) offers massive scale potential. Growth of generative AI at the edge enables on-device content creation, personalization, and augmented reality experiences. Partnerships between edge AI chip vendors and vertical solution providers create turnkey solutions for manufacturing, retail, and healthcare. Emerging markets in Asia Pacific and Latin America with rising IoT adoption present significant untapped demand for cost-effective edge AI platforms.

Challenges

Challenges include ensuring model robustness and security against adversarial attacks when processing data in uncontrolled edge environments. Power efficiency remains critical as many edge devices operate on batteries or limited energy sources. Interoperability across heterogeneous edge hardware and software stacks complicates deployment at scale. Talent shortage in edge AI optimization and embedded ML engineering slows innovation. Balancing privacy-preserving techniques (federated learning, differential privacy) with model performance requires ongoing research. Evolving standards for edge AI safety certification in safety-critical applications add uncertainty.

Edge AI Market: Report Scope

| Report Attributes | Report Details |

| Report Name | Edge AI Market |

| Market Size 2025 | USD 25.65 Billion |

| Market Forecast 2035 | USD 143.06 Billion |

| Growth Rate | CAGR of 21.04% |

| Report Pages | 225 |

| Key Companies Covered | Qualcomm Technologies, Inc., NVIDIA Corporation, Intel Corporation, Advanced Micro Devices, Inc., Huawei Technologies Co., Ltd., Samsung Electronics Co., Ltd., Apple Inc., Google LLC (Alphabet Inc.), and Others |

| Segments Covered | By Type, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of Edge AI?

The Edge AI market is segmented by type, application, end-user, and region.

By Type. Hardware is the most dominant subsegment, holding approximately 60% market share, due to the foundational role of specialized AI accelerators (NPUs, GPUs, ASICs) optimized for edge constraints in power, size, and latency. This dominance drives the market by enabling efficient on-device inference across billions of endpoints. Software ranks as the second most dominant, with around 25% share, including inference engines and development frameworks, propelling growth through easier model deployment and optimization.

By Application. Autonomous vehicles emerge as the most dominant subsegment, capturing about 25% share, primarily because edge AI is essential for real-time perception, decision-making, and safety in self-driving systems. This leads market growth by supporting the automotive industry’s massive transition to autonomy. Industrial IoT follows as the second most dominant, with roughly 20% share, enabling predictive maintenance and quality control, driving the market via Industry 4.0 transformation.

By End-User. Automotive & transportation represents the most dominant subsegment at about 28% share, driven by heavy investments in ADAS and autonomous driving requiring on-board intelligence. This dominance accelerates market expansion through large-scale deployments and influence on standards. Manufacturing ranks second most dominant, holding around 18% share, due to smart factory needs for real-time quality inspection, contributing to growth via efficiency gains.

What are the Recent Developments in Edge AI?

- In November 2025, BrainChip Holdings Ltd launched AKD1500 neuromorphic Edge AI accelerator co-processor chip targeting consumer devices in the U.S.

- In October 2025, Synaptics Incorporated introduced Astra SL2600 Series multimodal Edge AI processors, revolutionizing IoT device capabilities.

- In September 2025, ADLINK launched a new range of edge AI platforms designed for multiple end-user industries.

- In August 2025, NVIDIA announced advancements in the Jetson Thor AI processor for robotics and autonomous systems, delivering 8× performance.

- In July 2025, Qualcomm and Amazon collaborated to enhance in-car experiences usingthe Snapdragon Cockpit Platform with AI capabilities.

What is the Regional Analysis of Edge AI?

- North America is expected to dominate the global market.

North America holds the largest share at approximately 40%, with the United States as the dominating country, attributed to the concentration of leading AI chip vendors (NVIDIA, Intel, Qualcomm, AMD), a strong venture ecosystem, and a progressive regulatory environment supporting innovation in edge computing. This region’s leadership is underpinned by massive investments in autonomous vehicles, smart cities, and industrial IoT, world-class research universities (Stanford, MIT), and defense contracts requiring secure edge intelligence. High adoption in healthcare (remote monitoring) and retail (frictionless checkout) further solidifies dominance. Canada contributes through AI research hubs in Toronto and Montreal.

Europe follows with strong performance, driven by GDPR-compliant privacy-preserving edge AI and industrial strength, where Germany dominates through engineering excellence (Bosch, Siemens) and automotive leadership (BMW, Volkswagen). The region’s expansion benefits from EU funding (Horizon Europe, Digital Europe Programme) for trustworthy AI and green edge solutions. France advances in smart cities (Paris), while Nordic countries focus on energy-efficient edge for renewables. Collaborative frameworks and standardization efforts accelerate cross-border deployment.

Asia Pacific exhibits the fastest growth, fueled by manufacturing scale and government support, with China leading through Made in China 2025 initiative and massive IoT deployment. This area’s potential lies in cost-competitive edge hardware production, rapid 5G rollout, and smart city projects in Shanghai and Shenzhen. India’s PLI scheme boosts local semiconductor capabilities. Japan excels in robotics and automotive edge AI. South Korea’s Samsung and LG drive consumer electronics integration. Southeast Asia adopts for smart manufacturing.

Latin America demonstrates moderate progress, dominated by Brazil’s industrial and agtech sectors, supported by foreign investments though limited by infrastructure and economic variability. Mexico benefits from nearshoring and automotive supply chain integration with North America. Government digital transformation programs in Chile promote edge in mining and renewables. However, lower R&D investment slows innovation pace.

The Middle East and Africa remain emerging, with the United Arab Emirates leading through smart city investments (Dubai) and diversification efforts. Saudi Arabia’s Vision 2030 funds edge AI in oil & gas and healthcare. South Africa’s mining sector adopts for predictive maintenance. Technology transfers from global players build capabilities in Egypt. However, limited high-speed connectivity and energy infrastructure constrain widespread deployment.

What are the Key Market Players in Edge AI?

- Qualcomm Technologies, Inc. Qualcomm leads with Snapdragon platforms optimized for edge inference, focusing on automotive and mobile ecosystems through strategic partnerships.

- NVIDIA Corporation. NVIDIA drives growth with Jetson series for robotics and embedded AI, investing in CUDA ecosystem and developer tools for edge deployment.

- Intel Corporation. Intel emphasizes Habana Gaudi and Movidius VPUs, strategizing on open-source frameworks and industrial IoT solutions.

- Advanced Micro Devices, Inc. (AMD). AMD targets embedded markets with Ryzen Embedded and Versal ACAPs, focusing on power-efficient inference.

- Huawei Technologies Co., Ltd. Huawei leverages Ascend processors for edge in smart cities and manufacturing, expanding through global telecom integrations.

- Samsung Electronics Co., Ltd. Samsung integrates edge AI in Exynos and mobile processors, prioritizing consumer devices and automotive applications.

- Apple Inc. Apple focuses on Neural Engine in A-series/M-series chips for on-device intelligence in iPhones and wearables.

- Google LLC (Alphabet Inc.). Google advances Edge TPU and TensorFlow Lite for mobile and IoT edge inference, emphasizing developer ecosystem.

What are the Market Trends in Edge AI?

- Increasing deployment of generative AI models at the edge for on-device content creation.

- Rise of hybrid edge-cloud architectures for workload orchestration.

- Growing adoption of neuromorphic computing for ultra-low-power edge inference.

- Expansion of federated learning to preserve privacy across distributed devices.

- Integration of 5G/6G slicing with edge AI for mission-critical applications.

- Focus on sustainable, energy-efficient edge processors.

- Emergence of open-source edge AI frameworks and marketplaces.

What Market Segments and Subsegments are Covered in the Edge AI Report?

By Type

- Hardware

- Software

- Services

- Edge AI Chips

- Edge AI Accelerators

- Edge AI Processors

- Edge AI Modules

- Edge AI Platforms

- Edge AI Frameworks

- Edge AI Toolkits

- Edge AI Development Kits

- Others

By Application

- Autonomous Vehicles

- Industrial IoT

- Smart Cities

- Healthcare Monitoring

- Retail Analytics

- Surveillance & Security

- Predictive Maintenance

- Remote Monitoring

- Voice & Speech Recognition

- Computer Vision

- Others

By End-User

- Automotive & Transportation

- Manufacturing

- Healthcare & Life Sciences

- Retail & Consumer Goods

- Energy & Utilities

- IT & Telecom

- Agriculture

- Smart Homes & Buildings

- Aerospace & Defense

- Government & Public Sector

- Others

By Region

-

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

- North America

Frequently Asked Questions

Edge AI refers to artificial intelligence processing and inference performed directly on edge devices rather than in centralized cloud servers, enabling real-time decisions with low latency and improved privacy.

Key factors include 5G/6G expansion, IoT proliferation, privacy regulations, autonomous systems demand, and energy-efficient chip advancements.

The market is projected to grow from USD 25.65 billion in 2025 to USD 143.06 billion by 2035.

The CAGR is expected to be 21.04%.

North America will contribute notably, holding around 40% share due to technological leadership and industry adoption.

Major players include Qualcomm Technologies, NVIDIA Corporation, Intel Corporation, Advanced Micro Devices, Huawei Technologies, Samsung Electronics, Apple Inc., and Google LLC.

The report delivers comprehensive analysis of market size, trends, segmentation, regional insights, competitive landscape, and forecasts.

Stages include semiconductor design, chip fabrication, software/framework development, device integration, application deployment, and ongoing optimization.

Trends shift toward generative AI at the edge and privacy-first processing, with preferences for low-power, high-performance solutions.

Data privacy laws (GDPR, CCPA) mandate local processing, while energy efficiency regulations drive sustainable chip design.