AI in Food Industry Market Size, Share and Trends 2026 to 2035

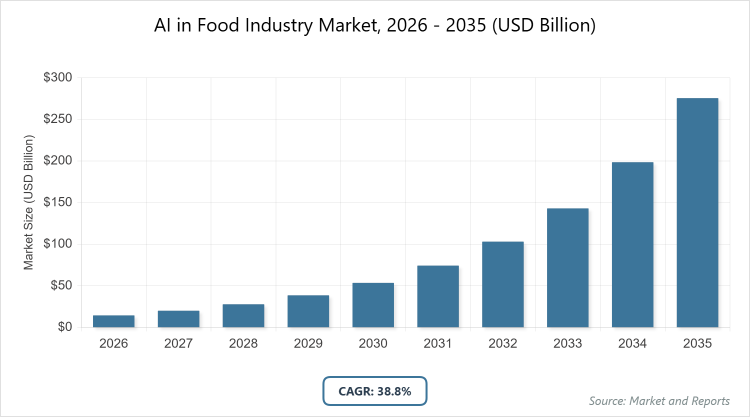

According to MarketnReports, the global AI in Food Industry market size was estimated at USD 14.41 billion in 2025 and is expected to reach USD 382.44 billion by 2035, growing at a CAGR of 38.8% from 2026 to 2035. AI in Food Industry Market is driven by the increasing demand for enhanced operational efficiency, food safety compliance, and personalized consumer experiences.

What are the Key Insights of AI in Food Industry Market?

- The global AI in Food Industry market was valued at USD 14.41 billion in 2025 and is projected to reach USD 382.44 billion by 2035.

- The market is anticipated to grow at a CAGR of 38.8% during the forecast period from 2026 to 2035.

- The market is driven by rising adoption of automation for efficiency, stringent food safety regulations, and the need for supply chain optimization.

- In the Component segment, Machine Learning dominates with a 40% share due to its versatility in data analysis and predictive capabilities, enabling real-time decision-making; Computer Vision is the second dominant with 25% share as it excels in quality inspection and defect detection, reducing waste and ensuring compliance.

- In the Application segment, Quality Control and Safety Compliance dominates with a 35% share because it addresses critical regulatory needs and minimizes risks; Supply Chain Management is the second dominant with 20% share, aiding in inventory optimization and reducing operational costs.

- In the End-User segment, Food Manufacturers dominate with a 45% share owing to large-scale integration for production efficiency; Restaurants are the second dominant with 20% share, leveraging AI for menu personalization and demand forecasting.

- North America holds the dominant regional share of 40% due to advanced technological infrastructure, high investment in AI R&D, and presence of key players fostering innovation.

What is the Industry Overview of AI in Food Industry?

The AI in Food Industry encompasses the integration of artificial intelligence technologies into various aspects of food production, processing, distribution, and consumption to enhance efficiency, safety, and innovation. Market definition refers to the application of AI tools such as machine learning algorithms, computer vision systems, and robotics to optimize operations across the food value chain, from farm to table, addressing challenges like waste reduction, quality assurance, and consumer personalization while promoting sustainability and compliance with global standards.

What are the Market Dynamics of AI in Food Industry?

Growth Drivers

The primary growth drivers in the AI in Food Industry include the escalating demand for operational efficiency amid rising production costs and labor shortages, where AI automates repetitive tasks like sorting and packaging to boost productivity. Additionally, stringent global regulations on food safety propel the adoption of AI for real-time monitoring and predictive analytics, preventing contamination and recalls. The surge in consumer preference for personalized nutrition and sustainable practices further fuels innovation, as AI enables data-driven insights into dietary trends and resource optimization, driving market expansion across segments.

Restraints

Restraints in the AI in Food Industry stem from high initial implementation costs, particularly for small and medium enterprises lacking the capital for advanced hardware and software integration, which hinders widespread adoption. Data privacy concerns and the complexity of handling vast amounts of sensitive consumer and operational data pose significant barriers, as compliance with varying international regulations adds layers of complexity. Moreover, the shortage of skilled professionals proficient in both AI and food science creates integration challenges, slowing down deployment and limiting the market’s potential in emerging regions.

Opportunities

Opportunities abound in the AI in Food Industry with the rise of emerging markets in Asia-Pacific and Latin America, where rapid urbanization and increasing food demand open avenues for AI-driven supply chain enhancements and precision agriculture. Advancements in generative AI and edge computing present prospects for innovative applications like autonomous recipe development and real-time waste management, attracting investments from tech giants. Partnerships between food companies and AI startups can accelerate personalized nutrition solutions, tapping into health-conscious consumer trends and fostering long-term growth through scalable, eco-friendly technologies.

Challenges

Challenges in the AI in Food Industry involve the integration of AI systems with legacy infrastructure in traditional food processing facilities, often requiring extensive overhauls that disrupt operations and increase downtime. Ethical issues surrounding AI decision-making, such as bias in algorithmic predictions affecting food equity, demand robust governance frameworks to maintain trust. Furthermore, the volatility of global supply chains exacerbated by climate change poses difficulties in data accuracy for AI models, necessitating continuous updates and adaptations to ensure reliability and effectiveness in dynamic environments.

AI in Food Industry Market: Report Scope

| Report Attributes | Report Details |

| Report Name | AI in Food Industry Market |

| Market Size 2025 | USD 14.41 Billion |

| Market Forecast 2035 | USD 382.44 Billion |

| Growth Rate | CAGR of 38.8% |

| Report Pages | 214 |

| Key Companies Covered | IBM Corporation, Google LLC, Microsoft Corporation, ABB Ltd., Honeywell International Inc., Oracle Corporation, NVIDIA Corporation, Rockwell Automation Inc., TOMRA Systems ASA, SAP SE, and Others |

| Segments Covered | By Component, By Application, By End-User, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, and The Middle East and Africa (MEA) |

| Base Year | 2025 |

| Historical Year | 2020 – 2024 |

| Forecast Year | 2026 – 2035 |

| Customization Scope | Avail customized purchase options to meet your exact research needs. |

What is the Market Segmentation of AI in Food Industry?

The AI in Food Industry market is segmented by Component, Application, End-User, and Region.

Based on Component Segment, Machine Learning emerges as the most dominant subsegment due to its ability to analyze vast datasets for pattern recognition and predictive modeling, which drives market growth by enabling proactive decision-making in areas like demand forecasting and process optimization; it helps propel the overall market by reducing inefficiencies and enhancing adaptability to consumer trends. Computer Vision is the second most dominant, excelling in visual inspections for quality control, which dominates because of its precision in detecting defects and ensuring compliance, thereby driving the market through minimized waste and improved product standards in high-volume production.

Based on Application Segment, Quality Control and Safety Compliance is the most dominant, as it leverages AI for real-time monitoring and anomaly detection, dominating due to regulatory pressures and the need to prevent costly recalls; this subsegment drives the market by bolstering consumer trust and operational reliability across the food chain. Supply Chain Management ranks second, optimizing logistics and inventory through predictive analytics, which leads because it addresses inefficiencies in global distribution networks, contributing to market growth by lowering costs and enhancing sustainability in resource allocation.

Based on End-User Segment, Food Manufacturers hold the dominant position, utilizing AI for large-scale automation and efficiency gains in processing lines, which dominates owing to the sector’s high volume and complexity requiring advanced tech integration; it drives the market by scaling innovations that reduce labor dependency and boost output. Restaurants are the second dominant, employing AI for menu personalization and operational streamlining, leading because of the need for quick adaptation to consumer preferences, thereby advancing the market through improved customer experiences and revenue optimization in competitive service environments.

What are the Recent Developments in AI in Food Industry?

- In 2025, NotCo partnered with Barry Callebaut to leverage AI for developing sustainable chocolate alternatives amid cocoa shortages, utilizing generative AI to formulate new flavors and textures that maintain quality while reducing dependency on traditional ingredients, marking a significant step in addressing supply chain vulnerabilities.

- PepsiCo expanded its AI applications in 2025 by using generative AI to create innovative snack flavors like Cheetos Crunchy Flamin’ Hot Pickle, analyzing consumer data to predict trends and accelerate product launches, demonstrating how AI shortens development cycles and enhances market responsiveness.

- Mondelez International integrated AI across its operations in late 2025, focusing on supply chain optimization and predictive maintenance, which improved efficiency by reducing downtime and waste, highlighting the shift from pilot projects to enterprise-wide implementation for cost savings and sustainability.

- In early 2026, the AI Institute for Next Generation Food Systems (AIFS) hosted a symposium outlining AI’s role in formulation and consumer insights, leading to collaborative frameworks for interoperable data standards that facilitate industry-wide innovation in personalized nutrition and health-focused products.

- Unilever adopted AI-driven tools in 2025 for flavor creation and personalized nutrition solutions, partnering with tech firms to analyze sensory data and consumer behavior, resulting in faster market entry for plant-based products that align with evolving health and sustainability preferences.

What is the Regional Analysis of AI in Food Industry?

- North America to dominate the global market

North America leads the AI in Food Industry with a 40% share, driven by technological advancements and strong R&D investments, particularly in the United States, where companies like IBM and Google spearhead innovations in quality control and supply chain AI; Canada contributes through agricultural AI applications, fostering efficiency and sustainability.

Europe holds a significant position, emphasizing regulatory compliance and sustainability, with Germany dominating through precision engineering in food processing AI; the UK and France focus on consumer engagement tools, enhancing personalized nutrition amid strict EU food safety standards.

Asia Pacific exhibits rapid growth, fueled by urbanization and tech adoption, with China leading in robotics and computer vision for manufacturing; India advances in predictive analytics for agriculture, addressing food security challenges in densely populated regions.

Latin America is emerging, leveraging AI for supply chain optimization, where Brazil dominates with applications in export-oriented agriculture and food exports; Mexico integrates AI in beverage manufacturing, improving efficiency in global trade networks.

Middle East and Africa shows potential in niche areas like waste reduction, with South Africa leading in AI for food safety in arid climates; the UAE invests in smart farming technologies to overcome resource constraints.

Who are the Key Market Players in AI in Food Industry?

- IBM Corporation: IBM focuses on cloud-based AI solutions like Watson for predictive analytics in supply chain management, partnering with food giants to enhance data-driven decision-making and reduce waste through strategic acquisitions in AI startups.

- Google LLC: Google leverages its DeepMind AI for computer vision in quality control, collaborating with agricultural firms to optimize crop monitoring, while investing in ethical AI frameworks to address data privacy in food personalization.

- Microsoft Corporation: Microsoft employs Azure AI for robotics and automation in food processing, forming alliances with manufacturers for IoT integration, emphasizing scalable strategies to boost operational efficiency across global operations.

- ABB Ltd.: ABB specializes in industrial robotics for food sorting, adopting collaborative strategies with tech integrators to deploy AI-enhanced automation lines, focusing on energy-efficient solutions to meet sustainability goals.

- Honeywell International Inc.: Honeywell uses AI for predictive maintenance in manufacturing, pursuing partnerships with sensor tech firms to improve food safety monitoring, with a strategy centered on integrated smart factory ecosystems.

- Oracle Corporation: Oracle provides AI-driven ERP systems for demand forecasting, engaging in cloud migration strategies for food retailers, aiming to streamline inventory and consumer insights through data analytics platforms.

- NVIDIA Corporation: NVIDIA powers AI hardware for deep learning in recipe development, collaborating with software developers to accelerate GPU-based simulations, targeting high-performance computing for innovative food tech applications.

- Rockwell Automation Inc.: Rockwell focuses on industrial AI for process optimization, implementing digital twin strategies in food plants, partnering with system integrators to enhance real-time monitoring and reduce downtime.

- TOMRA Systems ASA: TOMRA excels in optical sorting AI, adopting sensor fusion strategies to improve accuracy in food grading, expanding through acquisitions to cover broader waste reduction applications.

- SAP SE: SAP integrates AI in supply chain software, pursuing ecosystem strategies with food enterprises for end-to-end visibility, emphasizing analytics for personalized nutrition and regulatory compliance.

What are the Market Trends in AI in Food Industry?

- Increasing adoption of generative AI for flavor and recipe innovation, enabling faster product development cycles.

- Rise in AI-driven personalized nutrition apps, tailoring diets based on consumer health data.

- Enhanced focus on sustainability through AI-optimized waste reduction and resource management.

- Growth in agentic AI for autonomous decision-making in supply chains and manufacturing.

- Integration of multimodal AI models connecting sensory data with consumer preferences for better insights.

What Market Segments and their Subsegments are Covered in the AI in Food Industry Report?

By Component

- Machine Learning

- Deep Learning

- Computer Vision

- Natural Language Processing

- Robotics

- Predictive Analytics

- Big Data

- IoT Integration

- Cloud Computing

- Edge Computing

- Others

By Application

- Quality Control and Safety Compliance

- Supply Chain Management

- Predictive Maintenance

- Demand Forecasting

- Personalized Nutrition

- Food Safety

- Inventory Management

- Recipe Development

- Waste Reduction

- Customer Engagement

- Others

By End-User

- Food Manufacturers

- Beverage Manufacturers

- Restaurants

- Quick Service Restaurants

- Retailers

- Supermarkets

- Farms and Agriculture

- Food Delivery Services

- Hospitality

- Catering

- Others

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- South Africa

- Rest of Middle East & Africa

Chapter 1. Preface

1.1 Report Description and Scope1.2 Research Scope1.3 Research Methodology1.3.1 Market Research Type1.3.2 Market Research MethodologyChapter 2. Executive Summary

2.1 Global AI in Food Industry Market, (2026 - 2035) (USD Billion)2.2 Global AI in Food Industry Market: SnapshotChapter 3. Global AI in Food Industry Market - Industry Analysis

3.1 AI in Food Industry Market: Market Dynamics3.2 Market Drivers3.2.1 AI in the food industry is driven by automation for efficiency, strict food safety regulations, rising labor and production costs, and growing demand for personalized nutrition and sustainable practices.3.3 Market Restraints3.3.1 The market is restrained by high implementation costs, data privacy and regulatory complexities, and a shortage of skilled AI and food-tech professionals.3.4 Market Opportunities3.4.1 Opportunities arise from emerging markets, precision agriculture, generative AI applications, edge computing, and partnerships enabling personalized nutrition and sustainable, AI-driven food systems.3.5 Market Challenges3.5.1 Key challenges include legacy system integration, ethical and bias concerns in AI decisions, climate-driven supply chain volatility, and maintaining accurate, reliable data for AI models.3.6 Porter’s Five Forces Analysis3.7 Market Attractiveness Analysis3.7.1 Market Attractiveness Analysis By Component3.7.2 Market Attractiveness Analysis By Application3.7.3 Market Attractiveness Analysis By End-UserChapter 4. Global AI in Food Industry Market- Competitive Landscape

4.1 Company Market Share Analysis4.1.1 Global AI in Food Industry Market: Company Market Share, 20254.2 Strategic Development4.2.1 Acquisitions & mergers4.2.2 New Product launches4.2.3 Agreements, partnerships, collaborations, and joint ventures4.2.4 Research and development and regional expansion4.3 Price Trend AnalysisChapter 5. Global AI in Food Industry Market - Component Analysis

5.1 Global AI in Food Industry Market Overview: Component5.1.1 Global AI in Food Industry Market share, By Component, 2025 and 20355.2 Machine Learning5.2.1 Global AI in Food Industry Market by Machine Learning, 2026 - 2035 (USD Billion)5.3 Deep Learning5.3.1 Global AI in Food Industry Market by Deep Learning, 2026 - 2035 (USD Billion)5.4 Computer Vision5.4.1 Global AI in Food Industry Market by Computer Vision, 2026 - 2035 (USD Billion)5.5 Natural Language Processing5.5.1 Global AI in Food Industry Market by Natural Language Processing, 2026 - 2035 (USD Billion)5.6 Robotics5.6.1 Global AI in Food Industry Market by Robotics, 2026 - 2035 (USD Billion)5.7 Predictive Analytics5.7.1 Global AI in Food Industry Market by Predictive Analytics, 2026 - 2035 (USD Billion)5.8 Big Data5.8.1 Global AI in Food Industry Market by Big Data, 2026 - 2035 (USD Billion)5.9 IoT Integration5.9.1 Global AI in Food Industry Market by IoT Integration, 2026 - 2035 (USD Billion)5.10 Cloud Computing5.10.1 Global AI in Food Industry Market by Cloud Computing, 2026 - 2035 (USD Billion)5.11 Edge Computing5.11.1 Global AI in Food Industry Market by Edge Computing, 2026 - 2035 (USD Billion)Chapter 6. Global AI in Food Industry Market - Application Analysis

6.1 Global AI in Food Industry Market Overview: Application6.1.1 Global AI in Food Industry Market Share, By Application, 2025 and 20356.2 Quality Control and Safety Compliance6.2.1 Global AI in Food Industry Market by Quality Control and Safety Compliance, 2026 - 2035 (USD Billion)6.3 Supply Chain Management6.3.1 Global AI in Food Industry Market by Supply Chain Management, 2026 - 2035 (USD Billion)6.4 Predictive Maintenance6.4.1 Global AI in Food Industry Market by Predictive Maintenance, 2026 - 2035 (USD Billion)6.5 Demand Forecasting6.5.1 Global AI in Food Industry Market by Demand Forecasting, 2026 - 2035 (USD Billion)6.6 Personalized Nutrition6.6.1 Global AI in Food Industry Market by Personalized Nutrition, 2026 - 2035 (USD Billion)6.7 Food Safety6.7.1 Global AI in Food Industry Market by Food Safety, 2026 - 2035 (USD Billion)6.8 Inventory Management6.8.1 Global AI in Food Industry Market by Inventory Management, 2026 - 2035 (USD Billion)6.9 Recipe Development6.9.1 Global AI in Food Industry Market by Recipe Development, 2026 - 2035 (USD Billion)6.10 Waste Reduction6.10.1 Global AI in Food Industry Market by Waste Reduction, 2026 - 2035 (USD Billion)6.11 Customer Engagement6.11.1 Global AI in Food Industry Market by Customer Engagement, 2026 - 2035 (USD Billion)Chapter 7. Global AI in Food Industry Market - End-User Analysis

7.1 Global AI in Food Industry Market Overview: End-User7.1.1 Global AI in Food Industry Market Share, By End-User, 2025 and 20357.2 Food Manufacturers7.2.1 Global AI in Food Industry Market by Food Manufacturers, 2026 - 2035 (USD Billion)7.3 Beverage Manufacturers7.3.1 Global AI in Food Industry Market by Beverage Manufacturers, 2026 - 2035 (USD Billion)7.4 Restaurants7.4.1 Global AI in Food Industry Market by Restaurants, 2026 - 2035 (USD Billion)7.5 Quick Service Restaurants7.5.1 Global AI in Food Industry Market by Quick Service Restaurants, 2026 - 2035 (USD Billion)7.6 Retailers7.6.1 Global AI in Food Industry Market by Retailers, 2026 - 2035 (USD Billion)7.7 Supermarkets7.7.1 Global AI in Food Industry Market by Supermarkets, 2026 - 2035 (USD Billion)7.8 Farms and Agriculture7.8.1 Global AI in Food Industry Market by Farms and Agriculture, 2026 - 2035 (USD Billion)7.9 Food Delivery Services7.9.1 Global AI in Food Industry Market by Food Delivery Services, 2026 - 2035 (USD Billion)7.10 Hospitality7.10.1 Global AI in Food Industry Market by Hospitality, 2026 - 2035 (USD Billion)7.11 Catering7.11.1 Global AI in Food Industry Market by Catering, 2026 - 2035 (USD Billion)Chapter 8. AI in Food Industry Market - Regional Analysis

8.1 Global AI in Food Industry Market Regional Overview8.2 Global AI in Food Industry Market Share, by Region, 2025 & 2035 (USD Billion)8.3 North America8.3.1 North America AI in Food Industry Market, 2026 - 2035 (USD Billion)8.3.1.1 North America AI in Food Industry Market, by Country, 2026 - 2035 (USD Billion)8.3.2 North America AI in Food Industry Market, by Component, 2026 - 20358.3.2.1 North America AI in Food Industry Market, by Component, 2026 - 2035 (USD Billion)8.3.3 North America AI in Food Industry Market, by Application, 2026 - 20358.3.3.1 North America AI in Food Industry Market, by Application, 2026 - 2035 (USD Billion)8.3.4 North America AI in Food Industry Market, by End-User, 2026 - 20358.3.4.1 North America AI in Food Industry Market, by End-User, 2026 - 2035 (USD Billion)8.4 Europe8.4.1 Europe AI in Food Industry Market, 2026 - 2035 (USD Billion)8.4.1.1 Europe AI in Food Industry Market, by Country, 2026 - 2035 (USD Billion)8.4.2 Europe AI in Food Industry Market, by Component, 2026 - 20358.4.2.1 Europe AI in Food Industry Market, by Component, 2026 - 2035 (USD Billion)8.4.3 Europe AI in Food Industry Market, by Application, 2026 - 20358.4.3.1 Europe AI in Food Industry Market, by Application, 2026 - 2035 (USD Billion)8.4.4 Europe AI in Food Industry Market, by End-User, 2026 - 20358.4.4.1 Europe AI in Food Industry Market, by End-User, 2026 - 2035 (USD Billion)8.5 Asia Pacific8.5.1 Asia Pacific AI in Food Industry Market, 2026 - 2035 (USD Billion)8.5.1.1 Asia Pacific AI in Food Industry Market, by Country, 2026 - 2035 (USD Billion)8.5.2 Asia Pacific AI in Food Industry Market, by Component, 2026 - 20358.5.2.1 Asia Pacific AI in Food Industry Market, by Component, 2026 - 2035 (USD Billion)8.5.3 Asia Pacific AI in Food Industry Market, by Application, 2026 - 20358.5.3.1 Asia Pacific AI in Food Industry Market, by Application, 2026 - 2035 (USD Billion)8.5.4 Asia Pacific AI in Food Industry Market, by End-User, 2026 - 20358.5.4.1 Asia Pacific AI in Food Industry Market, by End-User, 2026 - 2035 (USD Billion)8.6 Latin America8.6.1 Latin America AI in Food Industry Market, 2026 - 2035 (USD Billion)8.6.1.1 Latin America AI in Food Industry Market, by Country, 2026 - 2035 (USD Billion)8.6.2 Latin America AI in Food Industry Market, by Component, 2026 - 20358.6.2.1 Latin America AI in Food Industry Market, by Component, 2026 - 2035 (USD Billion)8.6.3 Latin America AI in Food Industry Market, by Application, 2026 - 20358.6.3.1 Latin America AI in Food Industry Market, by Application, 2026 - 2035 (USD Billion)8.6.4 Latin America AI in Food Industry Market, by End-User, 2026 - 20358.6.4.1 Latin America AI in Food Industry Market, by End-User, 2026 - 2035 (USD Billion)8.7 The Middle-East and Africa8.7.1 The Middle-East and Africa AI in Food Industry Market, 2026 - 2035 (USD Billion)8.7.1.1 The Middle-East and Africa AI in Food Industry Market, by Country, 2026 - 2035 (USD Billion)8.7.2 The Middle-East and Africa AI in Food Industry Market, by Component, 2026 - 20358.7.2.1 The Middle-East and Africa AI in Food Industry Market, by Component, 2026 - 2035 (USD Billion)8.7.3 The Middle-East and Africa AI in Food Industry Market, by Application, 2026 - 20358.7.3.1 The Middle-East and Africa AI in Food Industry Market, by Application, 2026 - 2035 (USD Billion)8.7.4 The Middle-East and Africa AI in Food Industry Market, by End-User, 2026 - 20358.7.4.1 The Middle-East and Africa AI in Food Industry Market, by End-User, 2026 - 2035 (USD Billion)Chapter 9. Company Profiles

9.1 IBM Corporation9.1.1 Overview9.1.2 Financials9.1.3 Product Portfolio9.1.4 Business Strategy9.1.5 Recent Developments9.2 Google LLC9.2.1 Overview9.2.2 Financials9.2.3 Product Portfolio9.2.4 Business Strategy9.2.5 Recent Developments9.3 Microsoft Corporation9.3.1 Overview9.3.2 Financials9.3.3 Product Portfolio9.3.4 Business Strategy9.3.5 Recent Developments9.4 ABB Ltd.9.4.1 Overview9.4.2 Financials9.4.3 Product Portfolio9.4.4 Business Strategy9.4.5 Recent Developments9.5 Honeywell International Inc.9.5.1 Overview9.5.2 Financials9.5.3 Product Portfolio9.5.4 Business Strategy9.5.5 Recent Developments9.6 Oracle Corporation9.6.1 Overview9.6.2 Financials9.6.3 Product Portfolio9.6.4 Business Strategy9.6.5 Recent Developments9.7 NVIDIA Corporation9.7.1 Overview9.7.2 Financials9.7.3 Product Portfolio9.7.4 Business Strategy9.7.5 Recent Developments9.8 Rockwell Automation Inc.9.8.1 Overview9.8.2 Financials9.8.3 Product Portfolio9.8.4 Business Strategy9.8.5 Recent Developments9.9 TOMRA Systems ASA9.9.1 Overview9.9.2 Financials9.9.3 Product Portfolio9.9.4 Business Strategy9.9.5 Recent Developments9.10 SAP SE9.10.1 Overview9.10.2 Financials9.10.3 Product Portfolio9.10.4 Business Strategy9.10.5 Recent Developments

Frequently Asked Questions

AI in Food Industry refers to the application of artificial intelligence technologies to enhance processes in food production, processing, distribution, and consumption, including automation, data analysis, and predictive modeling for improved efficiency and innovation.

Key factors include technological advancements in machine learning and robotics, rising demand for food safety and personalization, regulatory pressures, and investments in sustainable practices, all contributing to accelerated adoption across the value chain.

The market is projected to grow from approximately USD 14.41 billion in 2025 to USD 382.44 billion by 2035.

The CAGR is expected to be 38.8% during the forecast period.

North America will contribute notably, holding around 40% of the market share due to its advanced infrastructure and innovation hubs.

Major players include IBM Corporation, Google LLC, Microsoft Corporation, ABB Ltd., Honeywell International Inc., Oracle Corporation, NVIDIA Corporation, Rockwell Automation Inc., TOMRA Systems ASA, and SAP SE.

The report provides comprehensive analysis, including market size, trends, segmentation, regional insights, key players, and forecasts, offering actionable data for strategic decision-making.

The value chain includes raw material sourcing with AI-optimized agriculture, processing and manufacturing automation, supply chain logistics and distribution, retail and consumer engagement, and end-of-life waste management.

Trends are shifting towards sustainability and personalization, with consumers preferring AI-enabled eco-friendly products and tailored nutrition, driving innovations in waste reduction and data-driven menu planning.

Stringent food safety regulations and environmental concerns like climate change are pushing AI adoption for compliance monitoring and resource efficiency, while data privacy laws influence technology implementation.